Last week (see Sailing Stormy Waters) we reviewed limited market options for Western Canadian heavy bitumen crude producers. The US Gulf Coast is the only viable market with significant refinery capacity to process these crudes. At the moment there is limited transport infrastructure in place to get them there. As a result prices are being heavily discounted in the over supplied Midwest market. The Canadian benchmark Western Canadian Select (WCS) price traded this January at a discount of more than $38/Bbl to the US benchmark West Texas Intermediate (WTI). Today we examine how much prices are likely to improve once the pipelines are built.

Canadian producers yearn for Gulf Coast crude oil values. Prices in that market are higher because they are not affected by US internal transportation constraints. The closest equivalent to WCS at the Gulf Coast is the Mexican crude Maya that has similar density and sulfur qualities. Over the last 15 months, Maya has sold on average for $30/Bbl more than WCS. The implication for Canadian producers is that if they could deliver their crudes to the US Gulf they would fetch far higher prices – less the cost of transport. At the moment aside from very constrained pipeline space those transport options are limited to rail tank cars – and some Canadian producers are using that alternative (see Crude Loves Rock’n’Rail – Heat It! Bitumen Economic Part 1). Moving bitumen crudes by rail however requires special infrastructure and can cost $30/Bbl – about as much as the Gulf Coast price premium – making the economics marginal unless special cost breaks have been negotiated.

So given that conditions are pretty miserable right now for Canadian producers, we wondered how different they might be once the infrastructure constraints are lifted? In other words – in a future scenario where there is adequate pipeline capacity from Western Canada to the US Gulf Coast allowing producers to ship heavy crude to market without interruption. Granted this might seem like fantasy to long suffering producers, but the idea of seamless pipeline transportation must surely have been envisioned when they originally planned expansions of heavy crude production. The point of this detour into (somewhat dangerous) crystal ball territory is therefore to try and figure out what the pricing situation might be on that happy day when pipelines are finally in place. After all - if prices for Western Canadian heavy crudes don’t improve once pipeline capacity becomes available – what was the point in expanding production in the first place?

Once pipelines are up and running, WCS will compete at the Gulf Coast with similar quality crudes such as Maya. The future price of Maya is therefore the natural starting point for understanding how much Canadian producers could expect to get for WCS without pipeline constraints.

Maya is a waterborne crude, sold under term contract by the Mexican state oil company, PEMEX. If you want to buy Maya you have to enter into a term contract agreement with PEMEX’s international marketing company “PMI” to take delivery of Maya in a crude tanker (that you would normally charter). The price you pay for Maya depends on the destination of the crude and is determined by a formula set by PMI. You can see the current price formulas on the PMI website here (in Spanish). There are 3 different formulas for each of the Mexican crude grades (Maya, Isthmus and Olmeca) and the formulas vary for delivery to the US Gulf Coast, Europe and Asia. The formula for Maya to the US Gulf is as follows:

Where: WTS = West Texas Sour, #6 Fuel Oil 3% = US Gulf Coast high sulfur fuel oil price, LLS = Light Louisiana Sweet, Brent DTD = the Brent North Sea Dated Cargo price, and K = the PEMEX formula adjustment.

The formula has two major components – the market price component and the PEMEX “K” constant or adjustment. The market price component uses three widely traded crudes – LLS, WTS and Brent and the price of fuel oil at the Gulf Coast. The first part of the formula (0.4 * (WTS + #6 Fuel Oil 3%) says that 80 percent of the market price component will be set by a 50/50 mix of WTS – the high sulfur sister crude to WTI - and high sulfur fuel oil. That means Maya’s high sulfur content mostly determines its price. A 50/50 mix of LLS and Brent crude sets the other 20 percent of the market price component.

The second component of the Maya US Gulf formula is the adjustment factor constant - often referred to as the “fudge” factor. This is a $/Bbl number determined every month in advance by PEMEX that is added to the formula market price component to arrive at the final price. This month (April 2013) the adjustment factor constant is - $4.90 meaning that you subtract $4.90/Bbl from the market price formula to arrive at the Maya price. Adjustment factors are published every month on the PMI website (here). The monthly changing constant factor allows PEMEX to adjust the final price that customers pay. PEMEX uses the adjustment factor in part to stay competitive with other crude suppliers. Although the constant is set ahead of time it should be seen in the context of a long term crude sales contract. If it turns out that the April constant was unfavorable to customers then PEMEX can adjust future constants to compensate refiners retrospectively. The adjustment factor is a very powerful tool, as we shall see.

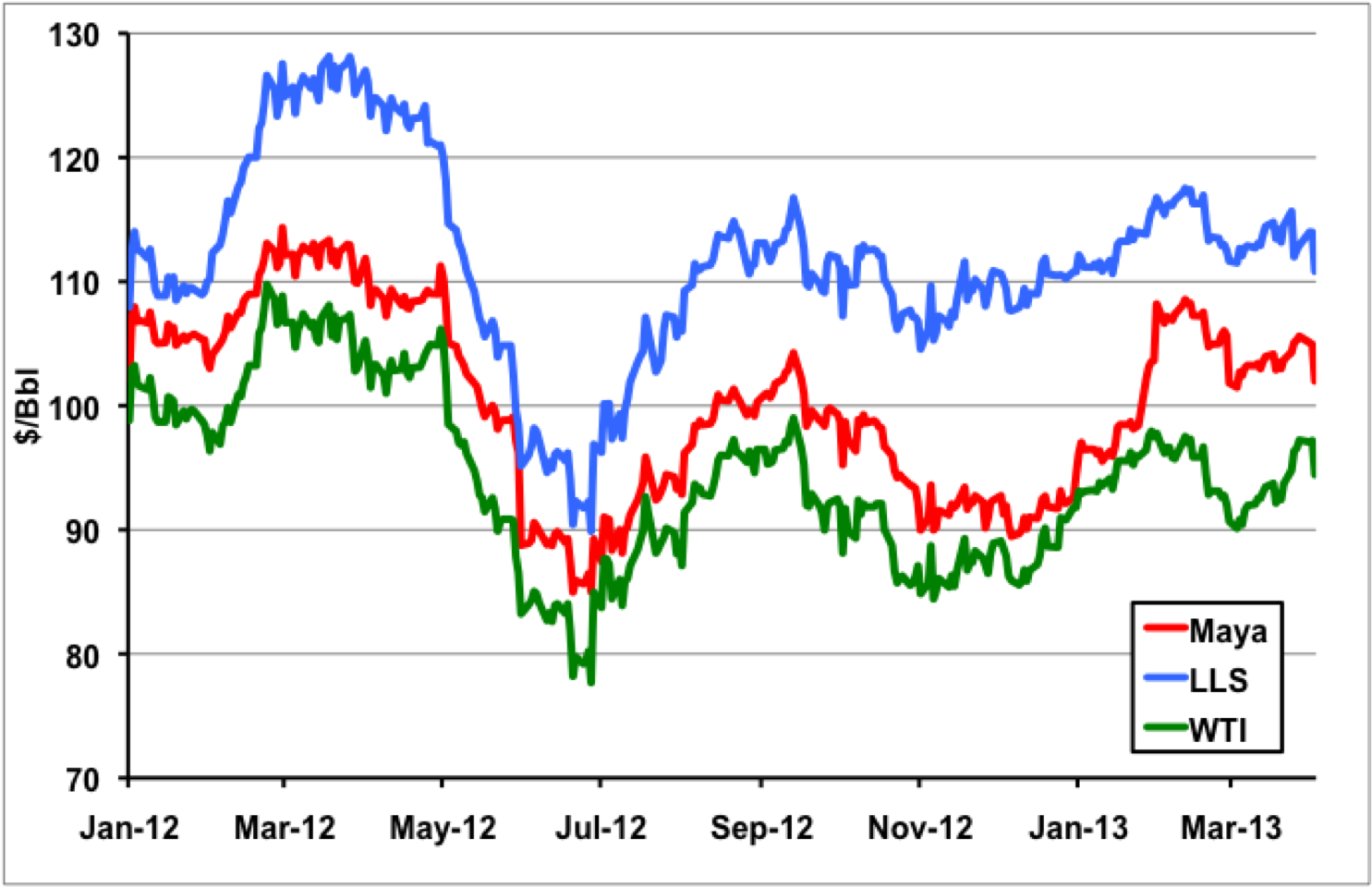

The chart below shows the calculated Maya formula price (red line) along with LLS (blue) and WTI (green) since the beginning of 2012. We put WTI in the chart even though it is not in the Maya formula because it is the US inland Cushing, OK benchmark currently used to price WCS. Both LLS and Maya are Gulf Coast crude prices. Because of the heavy weighting in the formula towards the high sulfur crude component, the price of Maya is lower than LLS by an average of $11.50/Bbl. Higher crude prices at the Gulf Coast compared to the Midwest mean that Maya traded at an average premium to WTI of $6/Bbl.

Source: CME data from Morningstar

Now comes the tricky part of our analysis – trying to predict what will happen to Maya prices once the pipeline constraints to move crude to the Gulf Coast are resolved. The reason the analysis is tricky is because the Maya formula contains prices for Midwest crude (WTS) as well as Gulf Coast crude (LLS), Gulf Coast products (fuel oil) and international crude (Brent). All of these moving parts have different influences and drivers – so it is like herding cats to figure out where they will head in the future. However, we can draw some basic conclusions from our previous analysis back in December of where price relationships might go after new pipelines to the Gulf Coast come online (see After The Flood).

It was our contention back then that “after the flood” WTI prices would move closer to LLS. We described a scenario where LLS would trade at a $6.50/Bbl premium to WTI Cushing based on the pipeline transport cost between Cushing and St. James, LA. The LLS premium to WTI has averaged a much higher $17.50/Bbl since January 2012. We expect the price of WTS at Midland to move closer to LLS in parallel with WTI since the two crudes have historically tracked within $3/Bbl of each other. Fuel oil prices at the Gulf Coast since January 2012 have traded at an average premium to WTS of $10/Bbl. Since international markets have generally more heavily influenced refined product prices, we expect fuel oil to stay level while WTS prices move closer to LLS.

So leaving aside the role of Brent crude in our prediction for the moment, we have the three domestic components in the Maya formula re-arranging themselves so that the WTS/Fuel oil combination (80 percent of the pricing component) is pulled closer to LLS when the WTS/LLS spread narrows. That means higher relative prices for Maya at the Gulf Coast in our future scenario.

The impact of future Brent prices on the Maya formula is considerably more complicated to predict. Our scenario back in December was that the flood of new light sweet crude coming into the Gulf Coast market in the next two years would push out light sweet imports. With no imported light sweet crude at the Gulf Coast the price of the international light sweet benchmark Brent would “detach” from the US market and follow its own direction. If that turns out to be the case then the Brent component of the Maya formula will arguably become obsolete. If Brent prices stray too far from other US Gulf Coast crudes then buyers will either insist PEMEX remove the Brent component or expect PEMEX to “neutralize” any adverse impact that Brent has on the formula using the monthly constant adjustment factor (we told you it was a powerful tool).

To sum up, based on the current Maya formula we expect that the spread between Maya and LLS will narrow from its recent average of $11.50/Bbl. Recognizing that we are deep into back of the envelope territory, we therefore expect Maya prices to be higher once the Gulf Coast pipeline logjam is resolved. At that time we can expect Canadian WCS crude to trade on the Gulf Coast at a quality discount to Maya of perhaps $2/Bbl because (as we explained in episode 1), WCS has “dumbbell” qualities that reduce its middle distillate yield compared to Maya. Bottom line – Canadian producers can finally expect to get higher prices for their crude – less transportation costs of course.

And those transportation costs will be greatly improved by then because pipeline capacity will be in place. Our estimate in Episode 1 was that pipeline transport from Hardisty, Alberta to the Gulf Coast would be around $14/Bbl. That means with all other factors being equal, Canadian producers should expect to realize crude prices of Maya minus $2/Bbl at the Gulf Coast and Maya minus $16/Bbl at Hardisty. Those will compare favorably with the past 15 month average discount to Maya of $30/Bbl at Hardisty. For example on April 3, 2013 LLS was $110.80/Bbl and Maya $102/Bbl. WCS at Hardisty was $80.5/Bbl. In our future scenario, Maya would be closer to LLS – say $105/Bbl and WCS would be Maya - $16 or $89/Bbl.

What could go wrong with this rosy picture? Here are three factors to bear in mind: