As North American supplies of natural gas continue to grow, more industrial, commercial, institutional and residential customers who do not burn natural gas for heating or process use want to participate in the economic savings associated with natural gas versus alternate fuels such as heating oil or propane. Complications in the process of installing pipeline infrastructure are slowing the rollout of direct gas line service. Today we describe natural gas distribution alternatives.

This is Part 2 of a two part series describing demand for natural gas fuel in the Northeast US and Atlantic Canada as a replacement for distillate (or in some cases residual) fuel oil. In Part 1, we discussed the desire of customers to convert from oil to natural gas fuel use and different state expansion initiatives that are underway. For oil-consuming customers located longer distances from existing natural gas transmission and distribution pipelines, there are a number of economic and policy reasons why natural gas pipeline expansion has been a slow and complex process. In this episode we look at solutions that temporarily or permanently replace pipeline infrastructure build out to distribute natural gas in the form of compressed natural gas (CNG) and liquefied natural gas (LNG).

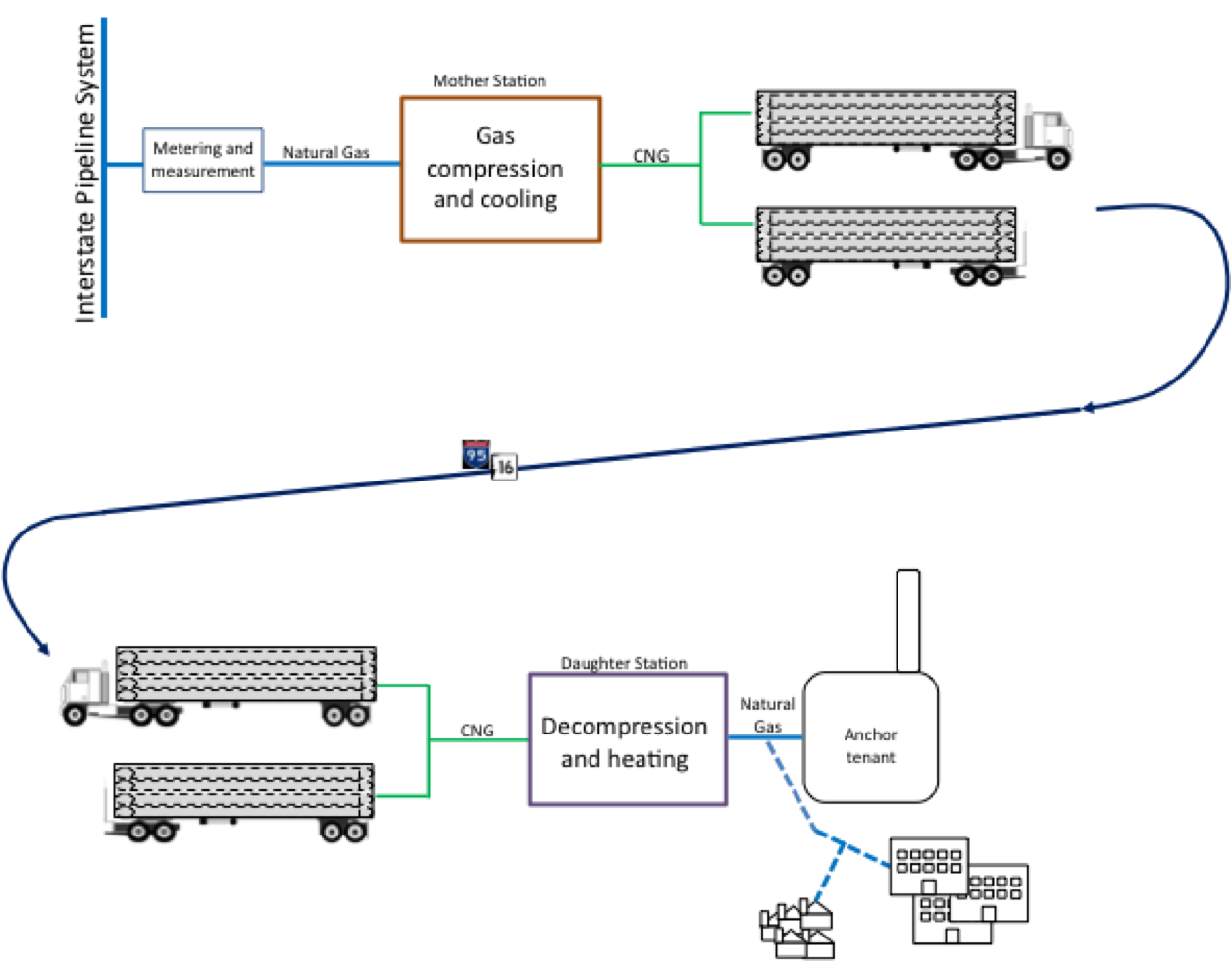

Trucked CNG

Trucked CNG has emerged as a timely and cost-effective solution to reduce high energy costs associated with oil use for some of New England and Atlantic Canada’s large energy consumers such as paper mills, asphalt plants, universities and hospitals. The concept is quite simple.

Known as “the virtual pipeline”, pipeline natural gas is delivered to a centralized compressor station or “mother station”, compressed to a volume that is approximately 1/300th of its original size, and then delivered via truck to a decompression facility or “daughter station” on the large customer’s (anchor tenant) site (see diagram below). In some cases, local distribution companies (LDCs) are considering taking delivery of natural gas via trucked CNG to serve bundles of customers including an anchor tenant in a location far from the interstate pipeline or LDC system, using the daughter station as the source of gas to feed both the anchor as well as a small pipeline distribution system serving commercial and residential customers (the “gas island”).

Source: OsComp Systems/Concentric Energy Advisors

This “virtual pipeline” is emerging as a tool for the LDC to expand their distribution systems to customers that may i) be too far from existing distribution pipelines, ii) require pipeline construction through sensitive or difficult areas such as water crossings or bedrock, or iii) not yet have energy demand that is large enough to economically support pipeline construction. Some LDCs are considering CNG as a tool to open new franchise areas via a gas island. For small customers that still depend on heating oil or propane as their primary energy source that are located far from interstate natural gas pipelines and/or LDC systems, this is indeed welcome news.

Industrial and large commercial or institutional customers can implement the conversion and start saving money in about three to six months, far less time than is required for even the shortest and simplest of natural gas pipeline expansions. Some customers will rely on trucked CNG on a permanent basis, probably maintaining some dual-fuel capability, while others are converting to CNG in anticipation of the arrival of pipeline supply several months or years from now.

In eastern New York, New England, and Atlantic Canada, distributed CNG is being delivered by multiple entities and the competition is heating up. The table below lists the companies who have either developed or are in the process of developing CNG infrastructure for distributed use in the region. Most mother stations are located on or near interstate pipelines or distribution systems and are proximate (100-200 miles) to large anchor customers, primarily industrial process facilities, hospitals, asphalt plants and universities. For the most part, existing LDCs are, so far, only marginally participating in certain of the CNG delivery systems, by providing either interruptible or firm natural gas to the CNG seller. These LDCs are not investing in the CNG infrastructure and are not yet involved in the downstream compression, distribution and customer service supply chain.

Comments

Excellent article, but the US is far behind Asia in the use of CNG or LNG. I spend half my time in Thailand and know Singapore and Malaysia well. My guess is that 60% of the Thai truck fleet is powered with CNG or LPG. Petronas has service stations throughout Thailand. The Bangkok and Singapore taxi fleets is by enlarge powered with CNG. My guess is that it is the same in Malaysia. Buying a car powered with CNG is extremely easy. Several of my neighbors have NG powered cars. We must understand that the coast of NG in Asia in on average is above $15 MMBtu. In the US gas stations are resistant to offer CNG or LPG. My understanding is that an 18 wheeler will save on average $20,000 per year once converted. Since a truck needs an overall every 300K to 400K miles, on average, it would make sense to do the conversion at that time. It took 7 years for the trucking industry to switch to diesel from gasoline; my guess is that we are 1/3 in the US trucking conversion.

Thank you for the article. I'm curious -- what about residential switching to propane from fuel oil in the Northeast? Propane would be a lot easier to transport and store, and there is beginning to be an abundance of it in the region. Have you heard much activity in that fuel-switching market?