With Brent premiums hovering close to $10/Bbl versus West Texas Intermediate (WTI) crude in the past month, the netbacks for Bakken producers shipping crude by rail to the East or West Coast are higher than they are for pipeline movements to Cushing or the Gulf Coast. Netbacks represent the crude price at the destination less transportation costs back to the wellhead. Today we show how the market destinations with the highest netbacks have reversed since July.

During 2012 when the Brent crude premium to WTI averaged $12/Bbl Bakken producers and midstream companies built out twenty rail loading terminals in North Dakota to bypass the crude congestion in the Midwest that was discounting their netback prices. Using rail they could get Bakken crude to coastal markets where prices traded closer to Brent. As a result the crude by rail business in North Dakota went from nowhere in 2011 to shipping 75 percent of the State’s crude to market by April 2013. Producers deserted the pipelines for railroads as North Dakota takeaway capacity changed from a famine of pipeline to a feast of rail (see The Year of the Tank Car). As long as the spreads between coastal markets and inland crude prices was wide enough to cover higher rail transport costs, the railroads provided the best netback.

In late February of this year the Brent premium to WTI started to narrow – putting pressure on crude rail transport netbacks. We discussed the consequences for crude by rail transport when the Brent premium over WTI was down to $9/Bbl in June (see Last Train to Bakkenville) and looked at Bakken producer netbacks when the premium had fallen to $4/Bbl in July (see Netback, Netback, Netback to Where You Started From). The Brent premium kept on falling – to reach close to parity later in July (see Reunited) – causing rail shippers to shift incremental volumes back to pipelines. This month (October 2013) the Brent premium to WTI has widened out again to more than $10/Bbl as US Gulf refiners are oversupplied at the Gulf Coast (see Goodbye Stranger).

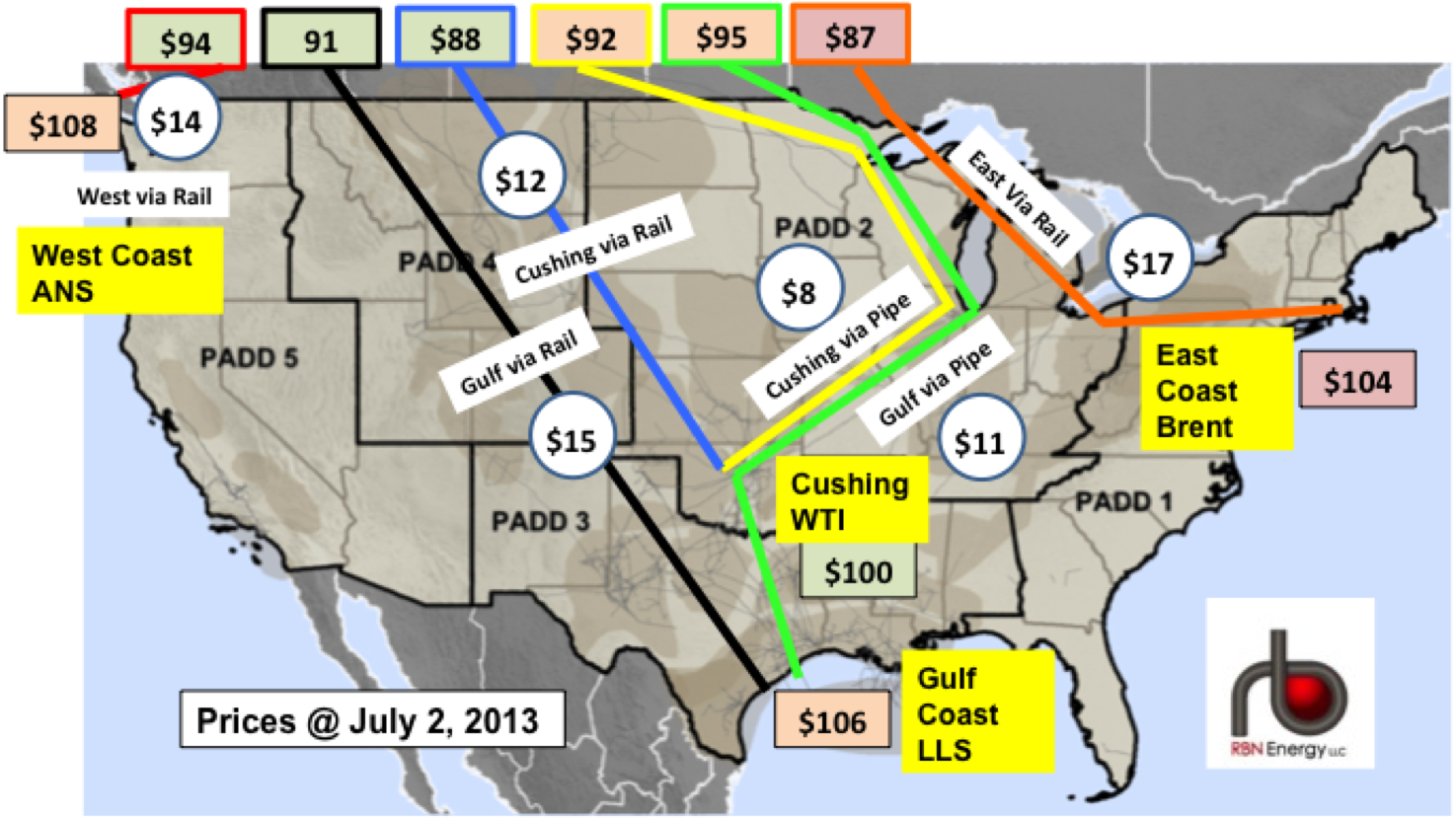

Today we compare Bakken netbacks in July – when the Brent premium to WTI was $4/Bbl – to the equivalent values this month – now Brent has widened back out to a more than $10/Bbl premium ($10.93 yesterday – October 28, 2013). The netback calculation estimates where a producer can get the best return on crude based on transport costs and destination prices (see Brent WTI and the Impact on Bakken Netbacks for a complete explanation). The following two map representations illustrate the impact of changing crude differentials on these Bakken producer netbacks between July and October 2013.

Source: RBN Energy

The first map (above) shows the netbacks on July 2, 2013 – when the WTI discount to Brent was $4/Bbl. The various routes and modes of transport from North Dakota to the West Coast, East Coast, Gulf Coast and Cushing, OK are shown on the map. We will compare these netbacks with the situation on October 22, 2013 (see map below). There is a summary table of the results lower down to make comparing them easier on your eyes. The transport costs indicated in circles on the maps are based on a number of industry presentations as well as published pipeline tariffs, terminal rates and estimates of rail car leases. The cost estimates include all transportation from the wellhead to the refining region and are by their nature representative rather than actual. [Note we have updated these costs using more accurate estimates since we last showed the July netbacks (see Netback, Netback to Where You Started From) and we used the latest transport costs in both July and October calculations here for a “level playing field” comparison. Rail lease rates have fallen since July but by less than $1/Bbl in most cases. The yellow text boxes indicate the market region and the adjacent box with a $/Bbl number is the prevailing benchmark crude price. The benchmark for the East Coast is Brent crude, for the West Coast, Alaska North Slope (ANS), for Cushing, OK it is WTI, and for the Gulf Coast, Light Louisiana Sweet (LLS).

About the song

“On the Road Again” was written by Willie Nelson and appears as the first song on side one, record one of Willie Nelson and Family’s Honeysuckle Rose soundtrack album. Nelson had his first starring role in the movie Honeysuckle Rose and, while on a flight, the film’s producer, Jerry Schatzberg, asked Nelson to come up with a theme song for the movie. Nelson wrote the lyrics for “On the Road Again” on an air-sickness bag before they landed. The song was recorded on Brian Ahern’s Enactron Truck Mobile Studio in Hollywood in the fall of 1979. “On the Road Again” was released as a single in August 1980 and went to #1 on the Billboard Hot Country Songs chart, #7 on the Billboard Adult Contemporary chart, and #20 on the Billboard Hot 100 Singles chart. It won Nelson a Grammy Award for Best Country Song. Personnel on the record were: Willie Nelson (lead vocal, guitar), Jody Payne (guitar), Bobbie Nelson (piano), Chris Ethridge (bass), Paul English (drums), and Mickey Raphael (harmonica).

Honeysuckle Rose, the soundtrack album by Willie Nelson and Family, is a double album featuring songs from the film performed by a number of artists, including Emmylou Harris, Johnny Gimble, and Jeannie Seely. Recorded in the fall of 1979 and produced by Willie Nelson, the album was released in July 1980. It went to #1 on the Billboard Top Country Albums chart and #11 on the Billboard 200 Album chart. Three singles were released from the LP.

Willie Nelson is an American country music singer, songwriter, guitarist and actor. One of the founding figures of the “outlaw country” movement in the seventies, Nelson is one of the most popular and recognized figures in country music. He has released 102 studio albums, 14 live albums, 51 compilation albums, two soundtrack albums, and 132 singles. He has appeared in 57 motion pictures and television shows. He is a member of the Country Music Hall of Fame, Rock and Roll Hall of Fame, and the National Agricultural Hall of Fame. He is the recipient of Kennedy Center Honors and the Gershwin Prize from the Library of Congress. Nelson continues to record and tour and is currently on tour in the U.S.