Supplies from the three main branches of the US condensate family are increasing faster than demand can keep up. Field condensate production from shale basins is nearing 1 MMb/d - headed to 1.6 MMb/d by 2018. Plant condensate – aka natural gasoline - will increase from just over 0.3 MMb/d in 2013 to more than 0.5 MMb/d in 2018. Because field condensates cannot be exported to overseas markets, more of this material will be refined traditionally or using a splitter – pushing out existing refinery demand for natural gasoline and creating an excess of naphtha range material. Petrochemical demand for natural gasoline has dried up in the face of cheap ethane feedstocks. Canadian demand for natural gasoline as diluent will soak up some but not the entire natural gasoline surplus. With US gasoline demand declining, the only outlet for excess naphtha and natural gasoline will be more exports (beyond Canada). Today we look at changing condensate demand patterns.

This is Part 2 of a two part series looking at the gap between surging condensate supplies and market demand. In Part 1 we provided definitions of the 3 branches of the condensate/pentane family and then detailed growing US condensate production. In this episode we tackle the demand side of the equation. Much of the material in this blog is adapted from a presentation Rusty made to the 3rd Annual Platts NGL Conference in Houston at the end of September (2013).

If you are new to condensates then you can refer to a number of previous RBN Energy posts on the topic in conjunction with this one. At the end of last year we provided some early definitions and looked at regulatory issues around condensates in our “Fifty Shades of Condensate” series including “Which One Did You Mean?”, “What Should be Done With Condensates?” and “Where is All This Condensate Going?” Earlier this year Al Troner of APPEC consulting contributed a couple of blogs on the market for condensates outside the US including some comprehensive definitions (see Through The Looking Glass). And there have been others on specific topics that (as usual) we will provide links to as we go along.

Demand for Field Condensate

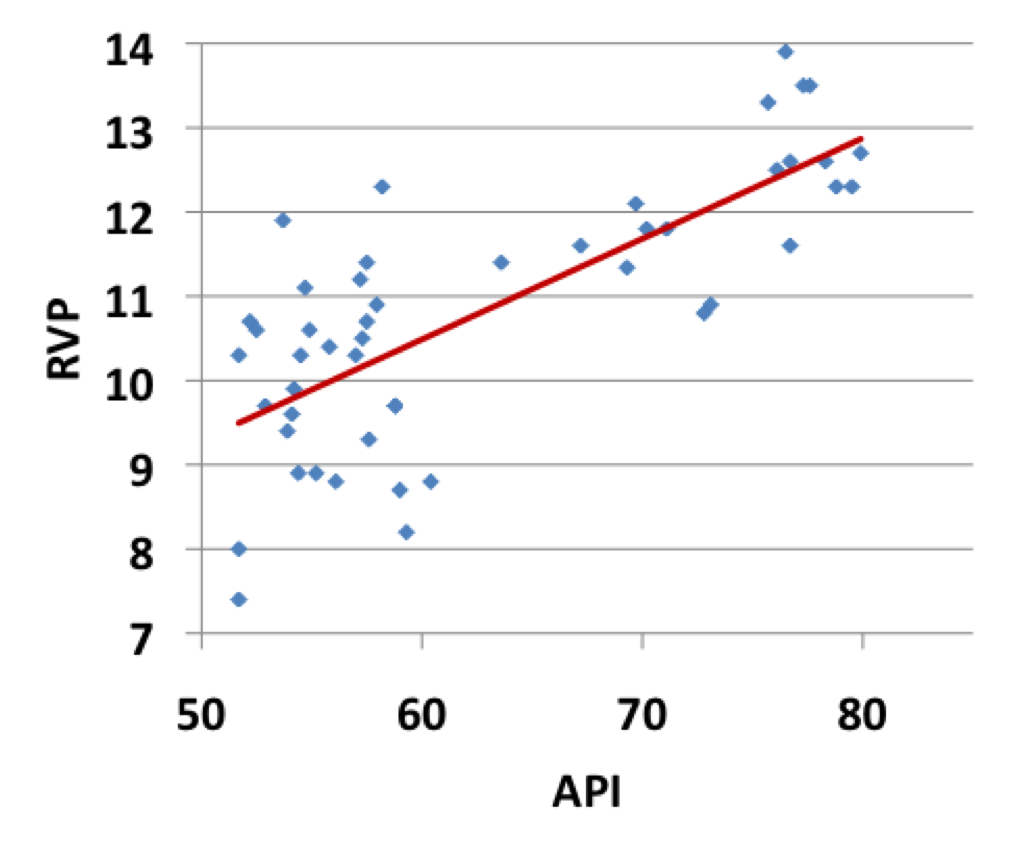

Field condensate is a buyer’s market in the US at the moment – especially in the condensate rich Eagle Ford basin – where up to 45 percent of crude is actually condensate. Producers suffer unwanted discounts from refiners that have a low opinion of their product, which is currently flooding the Gulf Coast market (see Don’t Let Your Crude Oils Grow Up to be Condensates). The Energy Information Administration (EIA) classifies condensate as crude, meaning that under Department of Commerce rules it cannot be exported overseas, where it might find a more welcoming home – for example in Asia (see Through the Looking Glass). Unlike the EIA, refiners do not consider condensate to be crude and they especially don’t like the box of chocolates problem – not knowing what they are getting. Refiners like standard, predicable crude grades that have qualities that do not vary much from batch to batch. Crudes like West Texas Intermediate (WTI) and Light Louisiana Sweet (LLS) fit the bill. Eagle Ford condensates are the opposite end of that spectrum. Every condensate seems to be different and the quality varies over time. The chart below is a scattershot of condensate assays, looking at only two qualities, API gravity (basically a measure of viscosity) and reid vapor pressure (RVP - a measure of volatility see Regulatory Gas Pressure Party). Some Eagle Ford condensates get a lot lighter than this – well above 100 API and look more like y-grade (mixed) NGLs than they do condensates. It is the wild west of U.S. hydrocarbons markets.

And not only is there a lot of variability from one condensate to the next, the other big problem with condensates is that they contain too many light hydrocarbon components that refiners do not need. These light components can overwhelm refineries configured to process heavier and more stable crudes – reducing effective refinery throughput capacity. At the moment this characteristic is constraining how much condensate Gulf Coast refineries can process – even though the price is routinely discounted by $20/Bbl against LLS.

Source: Turner Mason/RBN ENergy

Outside of conventional refineries there are few alternative homes for field condensates. It can and does get used as a diluent for Canadian heavy bitumen crude (see Heat It!). However, because of its unstable specification Canadian producers generally prefer to use natural gasoline that is produced to a standard quality. Shipments of condensate are making their way to Western Canada as diluent – via Houston (see It’s a Kinder Magic) or the Louisiana LOOP terminal (on the Capline pipeline). But the Canadian pipelines (today the Enbridge Southern Lights system, soon to be joined by the Kinder Morgan Cochin reversal) carrying diluent into the producing region in Alberta impose quality equalization standards that discount material that does not meet specification – meaning that some blending or pre-processing is required before field condensate is acceptable for diluent use.

Comments

Nice article thank you - I'am already looking forward to the follow-ups. Regarding condensate pricing, especially Eagle Ford's in relationship to LLS (i.e. the Eagle Ford discount to LLS), what is your view on the marker methodology suggested by Platts? In http://www.platts.com/IM.Platts.Content/MethodologyReferences/MethodologySpecs/eaglefordmarker.pdf, Platts suggests to calculate an Eagle Ford crude/condensate marker price by comparing the spot market value of the resulting refinery output slate with the spot marker value of an output slate based on LLS. This will then result in a differential to LLS which may be indicative for actual market diffs.

Do you think this is a useful approach or is condensate quality and therefore yield too variable?

Regards

Dan

In reply to Eagle Ford Pricing by Daniel Probst

Hi Dan,

The Platts Eagle Ford marker methodology is trying to capture a price assessment for Eagle Ford crude and it creates a yield of refined products based on a standardised yield with an API gravity of 47 degrees. That 47 API constraint is more like a light sweet crude - comparable to Light Louisiana Sweet than a field condensate - that would have an API above 50 and as high as 70.

In general valuing a crude based on a product yield is valid because it represents the refining gross product worth (GPW) of the crude. However, other factors impact crude prices - like supply and demand. Right now, very light Eagle Ford is oversupplied and has weak demand from refiners - causing discounts greater than might be reflected in the GPW.

Sandy

Hi Sandy,

Great write-up! You show a significant increase in the amount of natural gasoline exports in the forecast period. Is any of this material waterborne exports; if so, where do you believe it will be headed? Do you believe there could there be any demand in Europe and other regions for natural gasoline (if imported supply is cheap enough) for blending into refinery gasoline blending pool? Since NGLs in other regions are also not priced as low as in the US, could US-based natural gasoline compete for petchem feedstocks in other regions?

Thanks for your insights!

Guillermo

In reply to Hi Sandy, by Guillermo Saade

Guillermo

Take a look at prior blogs on condensate markets such as "Where is All This Condensate Going" for some analysis of non-Canadian exports as well as Through the Looking Glass Part 1 and Part 2 for analysis of European and Asian markets

Sandy

Guillermo,

I'm a bit of a neophyte to a lot of this and I have a stupid question: Although it probably has never even come close to being economical in the past (And I don't know if it's feasible now), is there any leeway in existing capacity to Alkylate C5s for diesel blend-stock? It seems plausible, and I know via google that Chevron filed patents on a process to do that in 2012. Especially if this stuff stays trapped in the U.S. I don't know what the alkylation values for that would be or how it would compare to the alkylation values of C4/C3 (I make that comparison with the naive assumption that the same equipment could be used for C5)

Just a thought. I'm enjoying this series of articles. It's really helping me.

Jesse