Way back in 2018-19, U.S. NGL production was rising fast, new ethane-only steam crackers were coming online along the Gulf Coast, and new fractionation capacity wasn’t being added quickly enough — the capacity shortfall sent the NGL market into near-panic. Fast forward to now: NGL production is still rising but domestic demand is flat, resulting in an NGL-exports surge and a race to develop new export capacity. And fractionation capacity in Mont Belvieu and elsewhere? The market learned its lesson five years ago and, to avert another capacity crunch, midstream companies have been adding new fractionators at an almost frenetic pace. In today’s RBN blog, we discuss the ongoing fractionation-capacity buildout — and the need to quickly expand NGL export terminals.

Having sufficient infrastructure in place is, of course, a critical need in each and every U.S. hydrocarbon market. There’s no way around it — you need the processing plants, the pipelines, the storage, and (especially in the Shale Era) the export docks to deal with the massive volumes of crude oil, natural gas and NGLs being produced. And don’t forget to build in a cushion, not just to deal with the daily and weekly ups and downs in supply and demand, but also to anticipate production growth.

Visualize the infrastructure behind U.S. NGL movement.

The U.S. NGLs Map provides a comprehensive view of the transport, processing, and export networks moving NGLs across the U.S.

NGLs, a favorite topic for many of us at RBN, are a case in point. As we said in last fall’s Drill Down Report on NGL networks, U.S. production of y-grade (mixed NGLs) has more than tripled over the past 15 years, and now tops 7 MMb/d — a much faster growth rate than crude oil or natural gas. There are many reasons for the steady rise in NGL output, including the fact that crude-focused wells in the Permian — by far the leading and fastest-growing production area — produce vast quantities of liquids-rich associated gas and that there is strong demand for NGL “purity products” like ethane, propane and butanes at Gulf Coast petrochemical plants and in overseas markets. Burgeoning NGL production has required an extended, far-reaching buildout of new infrastructure.

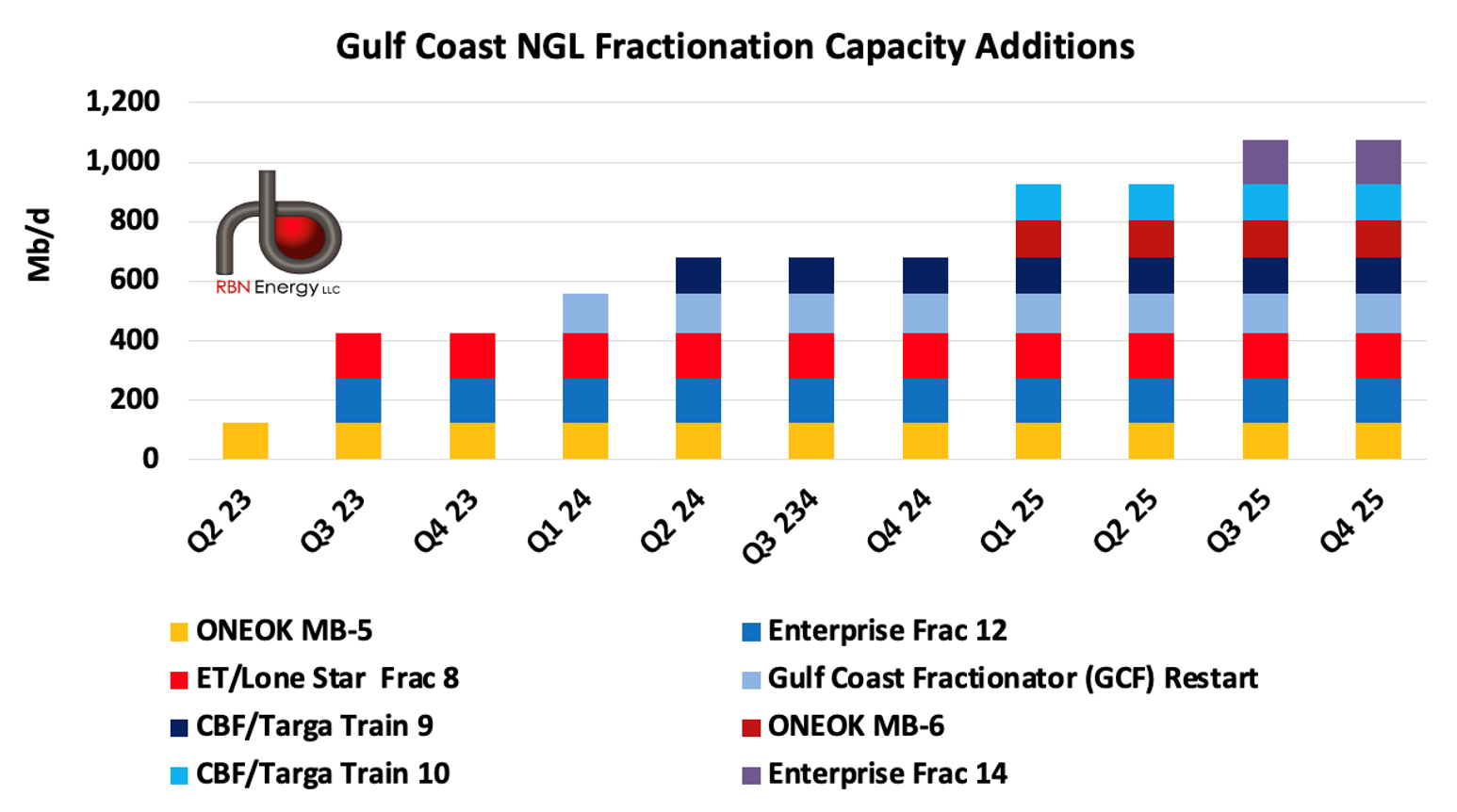

It should come as little surprise that all the new fractionators under construction today are located in Mont Belvieu. In our seven-part Magical Mystery Tour blog series a few years back, we explained that the NGL storage and fractionation hub in Mont Belvieu — about 30 miles east of Houston in Chambers County, TX — has been the epicenter of the North American NGL market for decades, largely because of the giant salt dome formation under the city’s Barbers Hill that allowed for the buildout of more than 250 MMbbl (yes, you read that right!) of underground NGL storage capacity. As shown in Figure 1 below, 443 Mb/d of new fractionators came online at Mont Belvieu in 2023, another 685 Mb/d will begin commercial operation there over the next 18 months or so, and 100 Mb/d of fractionation capacity that has been offline will be returning to service this spring. That will increase Mont Belvieu’s total capacity to more than 4.4 MMb/d by the second half of 2025 — a 35% gain since January 2023 and a doubling of fractionation capacity there since 2018.

Figure 1. Mont Belvieu Fractionation Capacity Additions, 2023-25. Source: RBN

About the song

“Kick Out the Jams” was written by the MC5 and appears as the second song on the MC5’s debut album of the same name. Released as a single in January 1969, the song went to #82 on the Billboard Hot 100 Singles chart. The fact that the song was censored but album copies were available with the “bad words” on them helped to propel sales in the same way that LPs with parental-warning labels helped to increase sales of heavy metal in the 1980s. Personnel on the record were: Rob Tyner (lead vocals), Wayne Kramer (guitar, backing vocals), Fred “Sonic” Smith (guitar, backing vocals), Michael Davis (bass, backing vocals), and Dennis Thompson (drums).

The album, Kick Out the Jams, was recorded live at Detroit’s Grande Ballroom over two nights in October 1968: Devil’s Night and Halloween. Produced by Elektra Records’ Jac Holzman and Bruce Botnick, the album was released in January 1969. It went to #30 on the Billboard 200 Albums chart. After the furor over the offending words on the title song, Elektra edited them out of some of the LPs, which infuriated the band and its manager, John Sinclair. Hudson’s, the Detroit department store chain, refused to carry the album, deeming it obscene. The band responded with a full-page ad in a Detroit newspaper featuring a picture of singer Rob Tyner with the words, “F Hudson’s,” with the Elektra logo on it. Hudson’s then refused to carry any Elektra product and the label dropped the MC5. The band promptly signed a new deal with Atlantic Records. The album has gone on to legendary status and is considered a seminal album for the punk rock movement. One single was released from the LP.

The MC5 was an American rock band formed in Detroit in 1963 with Rob Tyner, Wayne Kramer, Fred “Sonic” Smith, Michael Davis, and Dennis Thompson its core early members. Managed by counterculture guru and founder of the White Panther Party, John Sinclair, the band was considered radical anti-war political activists, in addition to being one of the greatest rock bands out of Detroit. For a taste of how fierce the band was live, check out their live performance at Tarter Field in Detroit, which is available on YouTube. Russ Gibb, who owned the Grande Ballroom in Detroit, loved the band and utilized them as the house band for the venue, helping them to build a large following. Most people who saw them at The Grande considered them to be the best band from Detroit, period. They released one live album, two studio albums, and eight singles before breaking up the first time after a show at The Grande Ballroom on New Year’s Eve in 1972. Smith then played in Ascension and Sonic’s Rendezvous Band before retiring and raising a family with punk giant Patti Smith. Kramer reformed the MC5 with a revolving cast of characters before being incarcerated for drug charges from 1975-78. After becoming sober, he released some excellent solo albums in the 1990s, did some MC5 reunion shows, and founded Jail Guitar Doors, a non-profit that provides prison inmates with musical instruments and counseling as a means of rehabilitation. Tyner performed as a solo artist and became a producer, manager, and promoter in Detroit, and Davis played with the Detroit band Destroy All Monsters. Thompson played in The New Order and New Race.

Rob Tyner died in 1991, Fred “Sonic” Smith died in 1994, Michael Davis died in 2012, and Wayne Kramer died earlier this month — our condolences to his family and friends. Dennis Thompson is the sole survivor from the original band. Amazingly, MC5 is still not in the Rock and Roll Hall of Fame.