The U.S. natural gas market is starting its 2015-16 winter season with a whopping 3,929 Bcf in storage, equal to the record maximum level set Nov. 2, 2012. Meanwhile gas production is also well above last year. Given these conditions, the market will need record demand to absorb incremental production and work off the surplus in storage. But weather forecasts so far are pointing toward a delayed start to winter heating demand. The price of natural gas has sagged under the pressure with the prompt CME/NYMEX Henry Hub futures contract treading at a price less than half this time last year. And, now, a number of operational factors and constraints are set to kick in for the winter that could further disrupt an oversupplied market. In today’s blog, we look at the storage and transportation dynamics that could factor into how the market balances this winter.

Last time, in Hazy Shade of Winter Part 1, we showed how the market balanced supply and demand this year to date has left storage inventories near record highs. This was in large part because of a storage overhang from last winter, which left 600 Bcf more in storage by the start of injection season April 1, 2015. Additionally, dry gas production averaged 73.5 Bcf/d this summer, about 3.0 Bcf/d higher than last year. While demand responded this summer (mostly higher volumes into gas fired generation), averaging 79.6 Bcf/d, 3.4 Bcf/d higher than last year, it was not enough to erase the storage overhang from the previous winter, and storage inventories ended injection season as of Oct. 31 equal to the record high. As noted above, the Energy Information Administration (EIA) reported inventories as of Oct. 30 were at 3,929 Bcf, which is 371 Bcf higher than last year and 224 Bcf higher than the 5-year average for that week. That’s a lot, and leaves the market oversupplied and in a tough spot for balancing this winter. Now, the gas market is making its seasonal “flip” from summer injection season to winter withdrawal season, which presents its own challenges for the market. So, next, we examine the seasonal flip from the perspective of storage and pipeline operations.

The Flippin’ Seasonal “Flip”

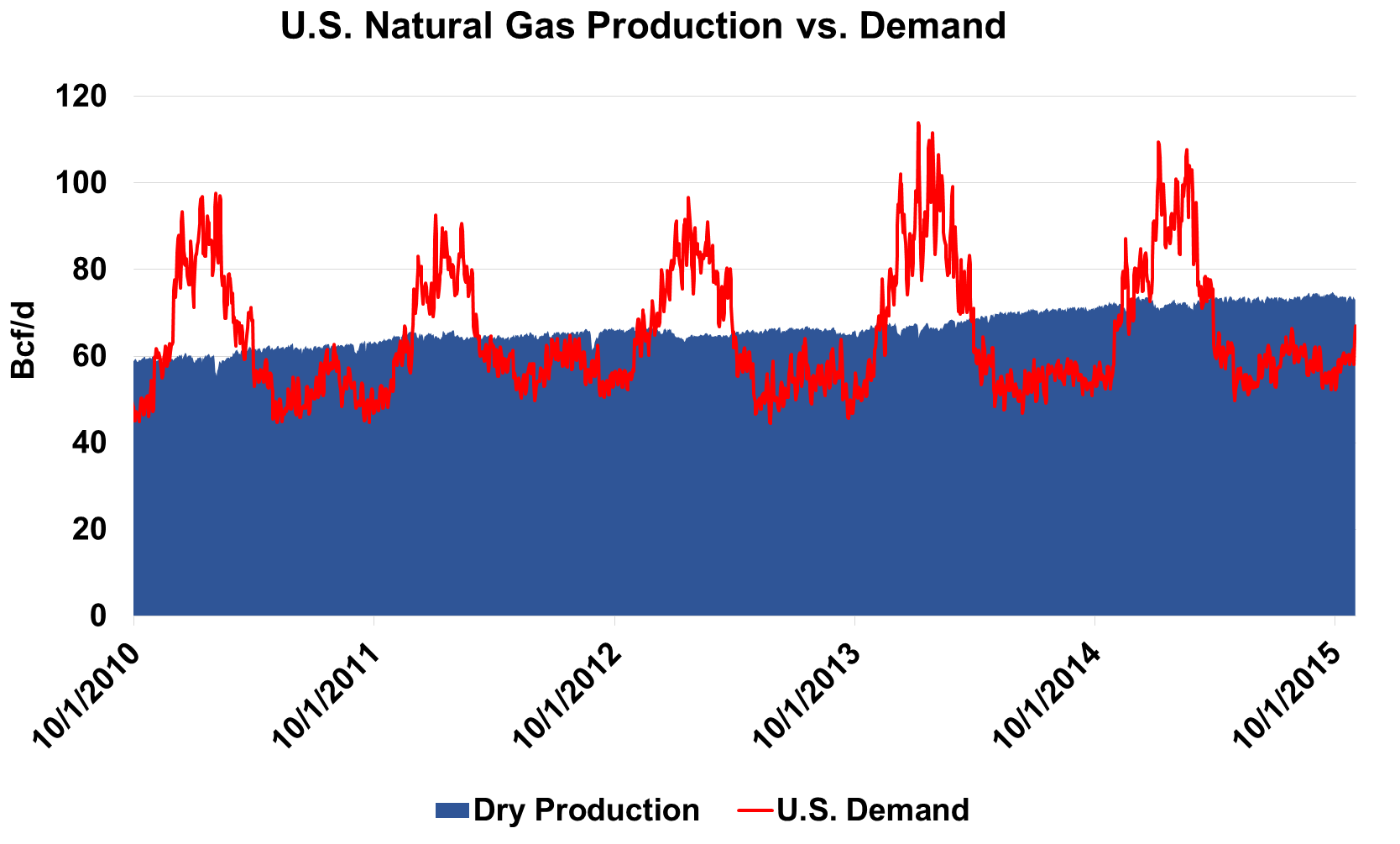

The flip from summer to winter season in the gas market is essential when demand begins to exceed available supply from production and imports and gas that was injected into storage during the lower-demand summer months is withdrawn to help meet demand. Of course, the primary driver behind the “seasonal flip” of the gas market is that cold weather drives gas demand well above available supply. In the big seasonal demand markets (Northeast, Midwest), gas demand for electricity generation, the primary demand source in the summer, is almost always lower than demand from home and commercial heating in the winter. Additionally the coldest weather strikes some of the most heavily populated regions, bolstering winter demand. Thus, as shown in Figure #1, weather can cause huge swings in gas demand (red line) from lows below 50 Bcf/d in the summer to highs close to 120 Bcf/d in winter. By comparison, gas production (blue area) is not weather-sensitive and steadily marches on, with the exception of a few temporary disruptions due to extreme cold in the winter (see Cold as Ice) or hurricanes the summer.

Figure 1; Source: PointLogic Energy

About the song

“A Hazy Shade of Winter” by Simon & Garfunkel, was released in October 1966, initially as a stand-alone single, but subsequently included on the duo's fourth studio album, Bookends (1968). The song peaked at number 13 on the Billboard Hot 100. In 1987, The Bangles recorded a cover version of the song for the Less Than Zero soundtrack; that version peaked at number two on the Billboard Hot 100.