It’s well understood today that the U.S. natural gas market turned from potential domestic shortages to major LNG exports thanks to the Shale Revolution. What is not so well remembered is that the dramatic shift in the U.S. gas market wasn’t widely understood at the time and took several years to be accepted by the energy industry. In today’s RBN blog, we turn our attention to the beginnings of the Shale Revolution and how it allowed the U.S. to evolve into the world’s largest LNG exporter.

Analyst Insights are unique perspectives provided by RBN analysts about energy markets developments. The Insights may cover a wide range of information, such as industry trends, fundamentals, competitive landscape, or other market rumblings. These Insights are designed to be bite-size but punchy analysis so that readers can stay abreast of the most important market changes.

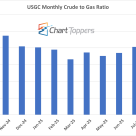

The monthly NYMEX crude-to-gas ratio for September 2025 stands at 21.4, where crude was $63.81/bbl and gas was $2.98/MMbtu, a slight decline from August’s 22.1.

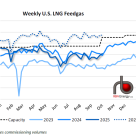

U.S. LNG feedgas demand averaged 15.4 Bcf/d last week (see blue-dotted line in figure below), up 0.1 Bcf/d from the previous week despite lower intake at Cove Point.

This week when nominations come to mind your thoughts naturally go to the political candidates in general, and the Tampa convention in particular. But don't forget about that other kind of nomination - the most important step in the scheduling of NGLs and other hydrocarbon transportation. Today we will continue our blog series on the Art of NGL Distribution by examining exactly how the nomination step takes place. We’ll continue the scenario covered last week in Movin’ Down the Line – Conway Propane to Janesville, WI on MAPL. That’s a nomination from Kansas, so we thought a politically themed title would be appropriate.

Understanding the natural gas market is not for the faint hearted. Natural gas production recently returned to record levels last seen before prices fell through the floor. How could that happen in the face of record storage levels? It’s all par for the course - in a world where the threat of a major Hurricane no longer impacts the price of natural gas (NYMEX Natural gas closed down 4 cents at $2.614 yesterday). Today we will look at buoyant natural gas production levels.

It looks like a combination of shale crude oil production and inventory drawdowns have been backing out crude oil imports over the past two months. Gulf Coast refineries are leading the way to crank up utilization, increase diesel exports and pull crude oil inventories down from the stratosphere. A lot of this activity seems to be bypassing Cushing. Meanwhile the Gulf Coast is at the center of two big events this week – a tropical storm and a huge refinery fire. Today we continue our analysis of crude inventories.

Every Wednesday energy markets eagerly anticipate the EIA Weekly Petroleum Supply Report release. Its contents frequently sway the market. Last Wednesday the biggest surprise was a 500 Mb/d reduction in crude imports. Today we start a two part analysis of EIA crude inventory data.

It’s still August, but there already is crispness in the Wisconsin mornings. And to a propaner, that’s a signal that the heating season is on its way. It is time to get those supplies lined out, and to make sure that customers are ready for the winter. But Wisconsin is a long way from the centers of propane supply. How does the propane get there? How do the Distribution experts make sure the right volumes are in the right place at the right time? In today’s blog we’ll continue our exploration of the Art of NGL Distribution by digging into the mechanics of moving supply on the Enterprise Mid-America Pipeline (“MAPL”) system from the Conway, KS hub to the Wisconsin market. Along the way we’ll learn how propane is scheduled on a pipeline system, how a NGL pipeline tariff works, and why the word “allocation” sends shivers down the spine of an NGL shipper.

Plenty of new natural gas shale reserves have been discovered in Western Canada. In British Columbia (BC) there are four basins (Horn River, Montney, Liard and Cordova) with estimated reserves in place exceeding 1,200 Tcf. Drilling in these basins is constrained by low natural gas prices, limited infrastructure and lack of market demand. Before any of these shale plays can be developed fully, producers have to find new markets for their gas that can justify the investment.

We’ve talked here frequently about the two ends of the Natural Gas Liquids market. On one end we have the commercial aspects of the business – things like pricing, differentials, processing economics and feedstock selection calculations. At the other end, there is the operational infrastructure – processing plants, pipelines, fractionators and downstream demand, including olefin plants. You may have wondered – what ties the commercial and operational worlds together? In the NGL world, the answer is Distribution – often the unsung hero of the NGL marketplace. Where the rubber meets the road. Where deal-making is translated into reality. Today we start a series of blogs to examine why NGL distribution is so important to the market, how it works, how Distribution generates value and why it is much an art as it is a science.

The Gnats Patootie

NGLs are complicated. First of all, there are five different products included under this umbrella: ethane, propane, normal butane, isobutane and natural gasoline. Each has different physical characteristics and different markets. With the exception of natural gasoline, all of the NGLs require high pressure and very low temperatures to move in a liquid state. All are highly flammable, heavier than air and require special handling all across the value chain – things like processing, fractionation, high pressure pipelines, insulated trucks rail cars, and salt dome storage. The total cost of all of this frequently can add up quickly, running over $0.20/gallon or $8/barrel, and occasionally much higher. It seems mind boggling, and for an amateur it can be.

The good news is there are many talented people behind the scenes working to ensure this is done well and efficiently. They live and breathe in a world filled with jargon terms like pump tickets, tenders, tariffs, fuel adjustments, product losses, pipeline allocations, product specs, late fees, component balancing, Product Transfer Orders (PTO’s), Bill of Ladings (BOLs), Freight on Board (FOB), demurrage, pumpovers, batch orders, stenched, unstenched, and the list goes on. It is a world that does not stop at 5pm. Product is moving 24 hours a day, 7 days a week. Most of the time things go right. But sometime things go wrong – mechanical failures, process upsets, product handling errors, and worse. All of these issues must be handled in a timely, methodical and professional basis. At the end of the day, all the paperwork (or databases, these days) must reconcile down to a gnats patootie. That’s a much tighter specification than six sigma.

The folks that inhabit this world are the Distribution experts – who can make or break the economics for NGL transactions. The job is Distribution. And the process is mysterious, critical, and truly an art—an art in which the big midstream players make big investments.

Is it just scheduling product from place to place? No, it’s a long way from that. The process involves understanding and actively engaging in every part of the NGL’s life from production to end use (like y-grade and propane in the Long and Winding Road Part I & Part II) and squeezing out every bit of value possible; down to a small fraction of a cent. It requires understanding the operations of production forecasting, gathering, gas processing and pipelines operations, high pressure tank cars, trucks, waterborne ships and barges, loading docks, fractionation, storage – salt caverns and above ground bullets, PTO’s (product transfer orders), computer technology, and cash flow.

The Art and Magic of NGL Distribution

But the Distribution expert must know more than the physical hardware. Infrastructure knowledge must be combined with a solid understanding of contract terms/flexibility, market intuition, and negotiating skills. It is truly an art to pull all of this together in a distribution plan that can be effectively and profitably executed. But that is still not enough. This knowledge must be combined with the talent and skill to develop great, dependable and valuable relationships with other people in the Distribution fraternity. It is these relationships that make the “magic” of this process happen. Some of the best in the industry have been doing this their whole career and are truly masters.

Companies who are serious about making money on NGL’s invest in the best and brightest to do Distribution for them. The large companies have Distribution experts for each product and each piece of the road. Others have experts handling larger pieces or the entire journey.

So what do most of these Distribution experts do? Just think, every time an NGL molecule changes location or changes hands a long chain of activities takes place. Each movement must be subject to a contract between the parties. Each transaction must be measured, reconciled and ultimately financially settled. Frequently (but not always) the triggering event for the physical movement of product is scheduling. That activity makes up a big part of the Distribution function, and it is a perfect place to start our journey.

Scheduling NGLs: Introducing Scenario #1

In “The Long and Winding Road”…we followed the journey of a molecule of propane from producing well to end-use market, which was a relatively typical journey. In the background of that story there were a minimum of 7 scheduling points, requiring at least 14 schedulers, tons of technology, phone calls, emails, spreadsheets, and lots of very high (human) energy. If that journey hadn’t been so smooth, those numbers (and Advil consumption) would be on the rise. Rarely does it go that smooth. Let’s look at some other typical winding road scenarios and do a deeper dive into exactly what NGL scheduling is all about.

“A Midwest NGL Company” (“AMNGLCo”) is a large midstream company that owns NGL assets and owns or controls production all over the US and Canada. Propane expertise has been the foundation for their success and a staple product for decades. They own it, buy it, sell it, transport it, store it, speculate on it, and build assets around it. Similar to other large midstream companies, distribution and scheduling is centralized in their home office, in this case located in Gotham City, Oklahoma. Those experts work via phone and e-mail with the “field” operations (considered all the people who physically make and move NGL’s) out and around the continent. This is an example of a company that understands the complexity and importance of Distribution and has the process down pat.

Here is just one (of many) scenarios that AMNGLCo could face every day.

“Keep (us) Dry!!!”

In August 2011 there were 900 rigs drilling for natural gas in the U.S. As of last week 405 gas rigs had disappeared and only 495 were left. As we all know, when gas prices fell, so did the natural gas rig count as producers moved capital budget dollars and rig crews to crude oil. That shift resulted in an astronomical increase in the crude oil rig count - from 1,050 this time last year to 1,432 today (Chart #1). But somehow the decline in the natural gas rig count has not translated into a decline in natural gas production. Very Strange. With shale gas wellhead production decline rates up to 80% in the first year, how is it that gas production has remained flat? Ghostly. When Halloween comes this year the 2012 natural gas production trend line will fall below the 2011 trend. What will that mean? Today, the 13th of August, we’ll look into the numbers to see how these spooky trends are likely to play out over the next few months.

A couple of weeks back in “A Market of Contradictions: Ethanol Mandates, Motor Gasoline and the Blend Wall” we looked at how US refiners are on the hook to blend more and more ethanol into a diminishing pool of gasoline (the blend wall) under Renewable Fuel Standard (RFS) legislation. Ethanol producers are losing 35 cnts/gal after the hottest July ever fried the corn harvest. Sinking ethanol production may not cover refiner’s needs. In response, refiners are turning to an arcane workaround called Renewable Identification Numbers (RINS). Today we'll peel back the red tape to see what is really going on.

The ratio between crude oil and natural gas (NYMEX) futures yesterday was 31.8. That is crude prices in $/Bbl were 31.8 X natural gas prices in $/MMbtu. In the 10 years from August 1997 to August 2007 the ratio averaged 7.5 X – that was the old world. Since August 2007 the ratio has averaged 19.4 X – with a dramatic rise during the last year to dizzying heights over 50 X. A major shift to high liquid hydrocarbon production has ensued. Now the futures market indicates the ratio will halve from 31 X to 15 X by 2020. Today we review the prospects for a return to a more normal crude to gas ratio.

September NYMEX natural gas closed up a nickel yesterday at $2.96/MMbtu. The January 2013 contract closed at $3.537 – a winter summer spread of $0.57/MMbtu, but the average seasonal spread in the futures market has fallen from $0.62/MMbtu just two years ago to $0.39/MMbtu this week. There was a time not that long ago when the winter-summer spread was measured in dollars. Now it seems to be fading into oblivion. Today we search for signs of seasonality in the forward curves.

Eagle Ford crude production is close to 600 Mb/d as of July 2012. Most forecasts show that number increasing to about 1,200 Mb/d over the next five years. Takeaway projects being developed today to go online by 2013 have capacity for 1,650 Mb/d. The midstream companies building these projects are either wildly optimistic or they know something about Eagle Ford production that we don’t. Today we look at plans for condensate takeaway from the Eagle Ford.

On Friday purity ethane in Mont Belvieu came in at 36.4 cnts/gal on OPIS, up 1.5 cnts while Conway ethane in E/P mix was up 1.25 cnts to 15.75 cnts/gal. Given that at this time last month Conway was trading at a dismal 2.25 ctns/gal while Mont Belvieu was wallowing under 30 cnts/gal, these numbers sound pretty good (See Chart #1 below). But let’s not lose sight of the fact that these prices are still dirt cheap. This time last year ethane prices were 2.5X to 3X higher. Is this simply a replay of the natural gas-oversupply-price-collapse story as some are saying? Or is it more complicated than that? As you’ve probably guessed, it is definitely more complicated than that. Because this the simplest of the NGL molecules turns out to be surprisingly complex in the marketplace. Today we’ll break down that complexity by looking at the details of the ethane markets.

Yesterday we learned that Gulf Coast diesel cracks (margins over crude) averaged $12.88/Bbl since August 2010 (read it here if you missed it). The result has been a Gulf Coast diesel-refining boom. Diesel production to feed this boom comes from refining conventional domestic and imported crude supplies that currently feed Gulf Coast refineries. Today we discover how new supplies of unconventional shale crude will force Gulf Coast refineries that process these light sweet crudes to kick their diesel crack habit.

[Note: This blog is based in part on projections from a new study on the implications of crude oil production growth and the crude quality dimensions of the increasing production from Turner, Mason and Company. More information on that study can be found in the block at the bottom of this blog.]

Gulf Coast diesel cracks (margins over crude) have averaged $8/Bbl more than gasoline for the past two years. As a result, Gulf Coast refiners have been producing more diesel than gasoline for the first time since records began. US demand for diesel has remained flat but exports have boomed. Diesel has been a shining light for US Gulf refiners at a time when their colleagues on the East Coast and in Europe are heading for the exits. Today we examine the diesel boom and where it is headed.