Canadian demand for diluent is currently forecast to increase by 300 Mb/d between 2013 and 2020. That picture could change dramatically if pipeline projects to transport heavy Canadian bitumen crude to the US Gulf and diluent to Western Canada are delayed or cancelled. In any case, developing plans to transport “raw” bitumen by rail seem set to reduce diluent demand. The possibility of lower diluent demand threatens the most promising market today for increasing US natural gasoline and lease condensate production. Today we complete a two part series on Canadian condensate demand.

In the first part of this series (see Fifty Shades of Eh?) we looked at production forecasts for Canadian heavy bitumen crude that is projected to increase from 1.7 MMb/d in 2011 to 2.9 MMb/d in 2017. The primary market for this heavy sour crude is the US Gulf Coast and the transport mechanism of choice to get there is pipeline. As much as 55 percent of that tar sands crude will be blended with diluent in 2017 in order to reduce its viscosity so that it can flow in pipelines. [The rest of the production is upgraded into lighter synthetic crudes.] Heavy crude blending will create demand for approximately 480 Mb/d of diluent in 2017 assuming a 70:30 ratio of bitumen to diluent. We discussed the various alternative diluents that can be used and where they would come from. Canada will produce about 140 Mb/d domestically and the rest will need to be imported. Canadian producers generally prefer natural gasoline - a natural gas liquid (NGL) because lower volumes are needed for blending versus lease condensates. Only 140 Mb/d of US natural gasoline are expected to be available for export to Canada in 2017. The balance of diluent demand after Canadian production and US natural gasoline exports will be met by lease condensate. There is plenty of lease condensate available from rising US shale production – especially in the Eagle Ford. In this episode we look at the heavy crude demand for diluent out to 2020 and how condensate supplies will get to Western Canada to meet the need.

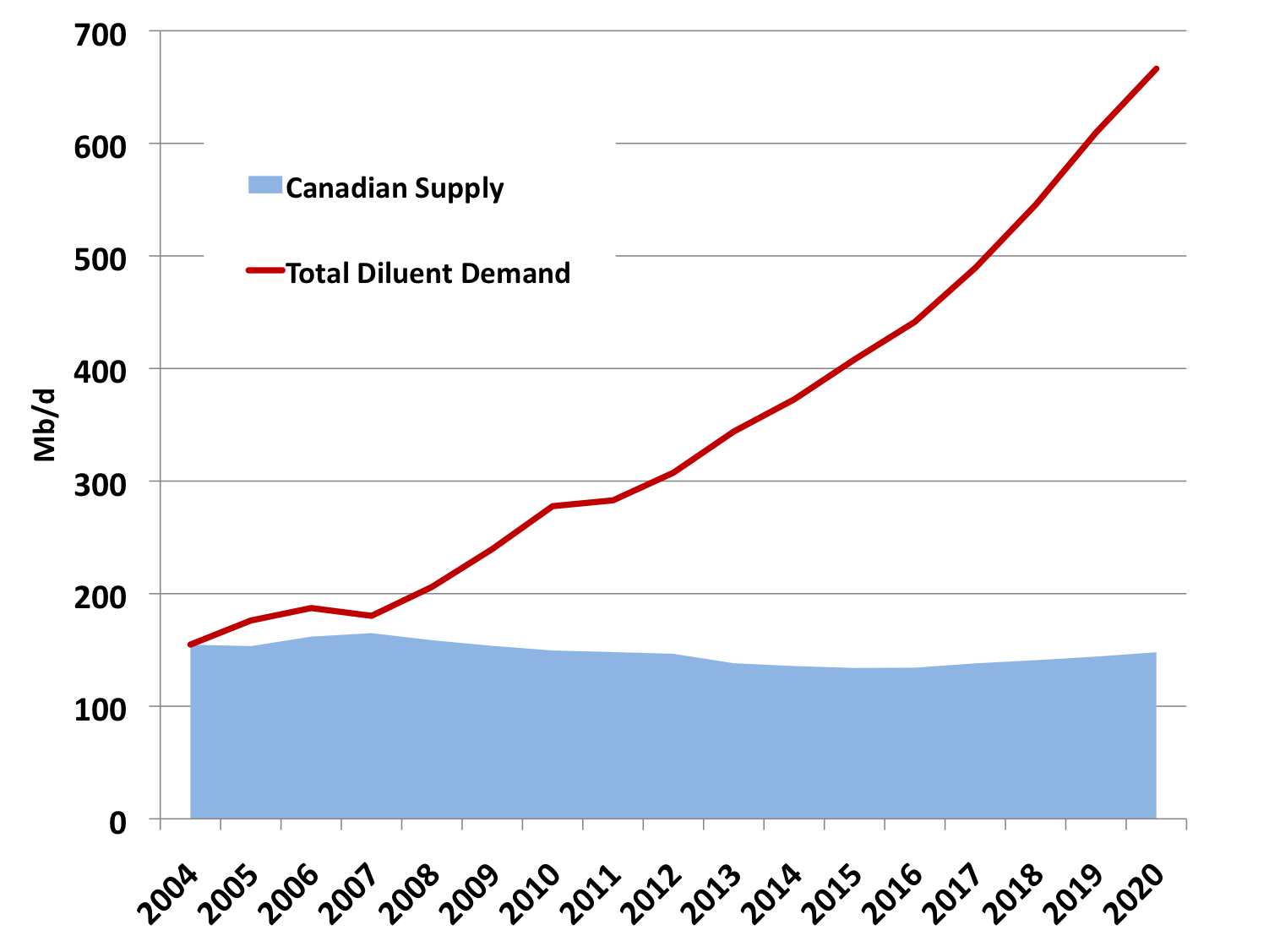

The chart below shows forecast Canadian demand for diluent out to 2020 based on a Canadian Energy Research Institute (CERI) NGL report published at the end of 2012. The data indicates 2013 demand for diluent will be 340 Mb/d rising to 670 Mb/d in 2020. The chart also shows the forecast for Canadian supply in 2013 will be 138 Mb/d rising to 148 Mb/d in 2020. The demand for Canadian diluent imports will therefore increase from about 200 Mb/d in 2013 to more than 500 Mb/d in 2020. The CERI forecast is conservative compared to some estimates that add as much as 200 Mb/d to diluent requirements.

Source: CERI and RBN Energy (Click image to enlarge)

US production of lease condensate is increasing rapidly and appears to be creating all kinds of challenges for Gulf Coast refiners that are not equipped to consume such a light feedstock. Since US lease condensate exports are banned except to Canada, supplies are basically flooding the market looking for a home. Given the Canadian demand for diluent the challenge is finding a way to deliver adequate supplies of natural gasoline and lease condensate to Western Canada.

In our recent series on Gulf Coast crude terminals we covered two transport routes for diluent to Western Canada. The first of these was shipping condensate to Canada via Plains All American (PAA) infrastructure in St. James, LA (see Plains Trains and Diluent Deals). Those shipments move condensate on the Capline pipeline (PAA owns the largest percentage of Capline) to Patoka near Chicago, IL from where it is shipped on the Enbridge Southern Lights pipeline to Edmonton, AB and then on the PAA Rainbow II pipeline to the Canadian oil sands fields at Nipsi, AB. PAA has separately invested in pipeline infrastructure in the South Texas Eagle Ford basin that now delivers significant volumes of condensate to its marine terminal at Corpus Christi, TX where it is loaded on barges and shipped St. James.

The second diluent route to Canada that we identified is the Explorer pipeline and the Kinder Morgan (KM) Cochin reversal project (see It’s a Kinder Magic). Like PAA, Kinder Morgan has developed a lease condensate gathering system in the Eagle Ford that feeds a 300 Mb/d pipeline to their Galena Park terminal on the Houston Ship Channel. From there customers can ship lease condensate on the Explorer pipeline to Hammond, IL south of Chicago. Explorer held an open season in March and April 2012 for a “diluent extension” from Peotone, IL to Manhattan, IL to be in service 1Q 2014 that will link with the Enbridge Southern Lights pipeline. In the meantime there are indirect pipeline routes that allow for Explorer product to transfer to Southern Lights in Chicago. KM is also awaiting final approval from the Canadian National Energy Board for a project to link Explorer to their existing Cochin pipeline that runs from Western Canada to the US Midwest. KM will build a new terminal that links Explorer to the Cochin pipeline at Kankakee, IL. KM will then reverse and expand part of Cochin to carry diluent westward to Fort Saskatchewan, Alberta. If approved, the project will come online in July 2014. In addition to moving lease condensate from the Eagle Ford to Western Canada, the Explorer pipeline is connected to Mont Belvieu 20 miles east of Houston – the center of the NGL universe (see Can Mt. Belvieu Handle the NGL Supply Surge for more on Mt. Belvieu). That link means that US natural gasoline exports can also flow to Canada on the same route.

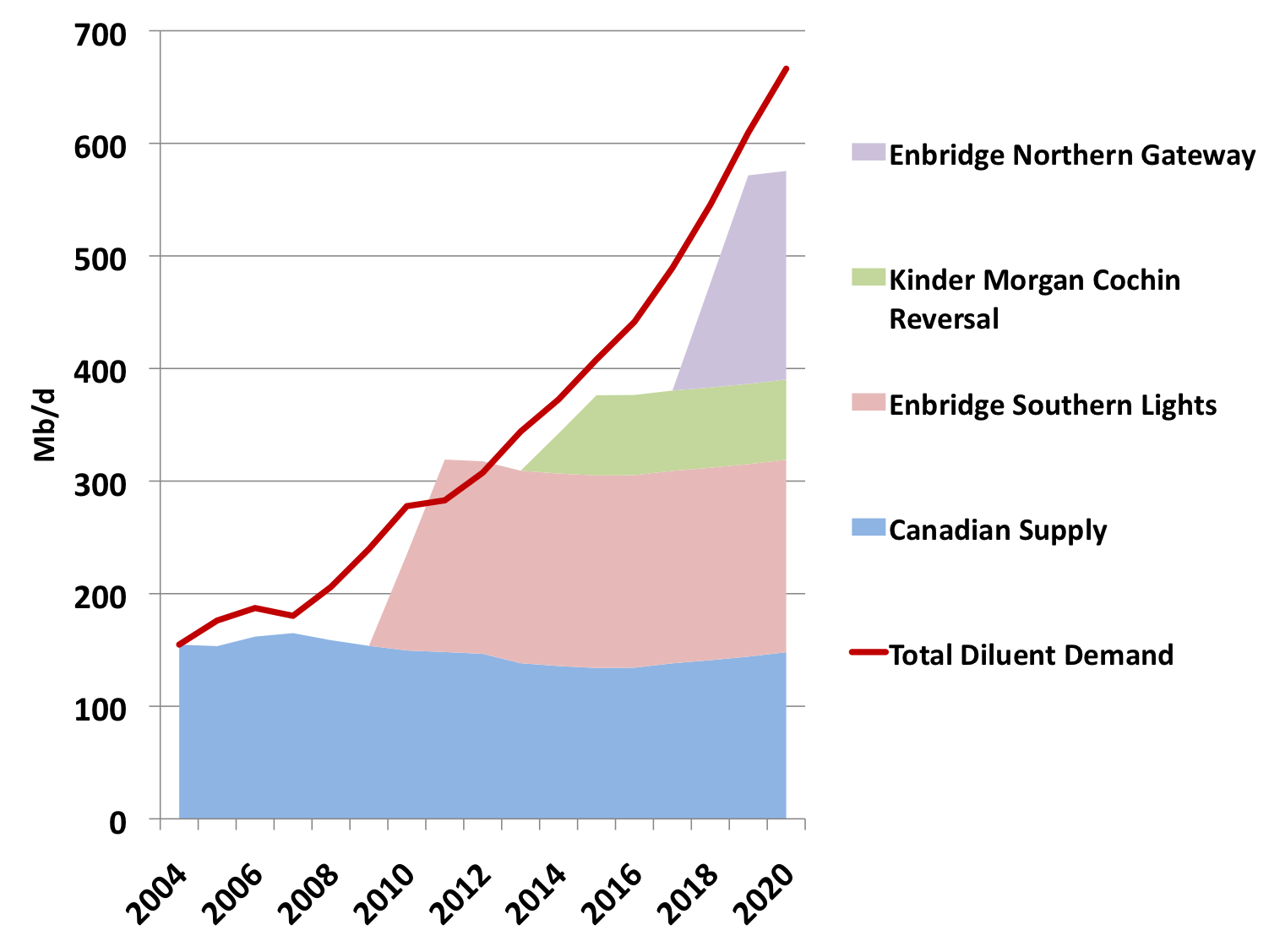

The Southern Lights pipeline capacity to carry diluent is 180 Mb/d – much of which is already being used by shippers on the Capline and Explorer to deliver diluent. The Cochin reversal will add another 95 Mb/d of capacity.

Aside from the Enbridge Southern Lights and Kinder Morgan Cochin reversal one more pipeline project is on the drawing board that will supply diluent imports into Western Canada. That is the Enbridge Northern Gateway pipeline (see West Coast Pipe Dreams – Canadian Double Jeopardy) that is planned to run from Edmonton, AB to a new deep-water port at Kitimat, BC on the Canadian West Coast. Northern Gateway is designed to include two parallel pipelines. The first (525 Mb/d) will carry diluent blended bitumen to the coast for export and the second will carry 190 Mb/d of imported diluent back to Edmonton.

The chart below has the same forecast of diluent demand that we saw above as well as the Canadian supply. We also added in the quantities that can be delivered via the pipeline routes just discussed. During this year (2013) supplies are restricted to the Southern Lights pipeline that will be adequate to meet demand until next year. The Kinder Morgan Cochin reversal will kick in during 2014 but still leave a gap between pipeline supply and transportation capacity. After 2017 adequate supplies will rely on Northern Gateway being built and again it looks like demand will outstrip pipeline capacity.

Source: CERA and RBN Energy (Click image to enlarge)

Any gap between available pipeline capacity and diluent demand during the period after next year could of course be met by alternatives to pipeline transportation. The obvious choice in that case would be rail tank car. A certain amount of rail tank car transportation of natural gasoline and condensate is already happening. The data is not clear about how much diluent is being moved this way because railroad statistics do not distinguish between crude and condensate or natural gasoline. The US Energy Information Administration do not keep track of railroad movements into Canada by product either. Given the recent dramatic increase in the movement of crude by rail then we can only imagine that Canadian demand for condensate will justify increased rail shipments of diluent to Canada once pipeline capacity is full. The increased production of NGL’s expected in coming years in the Marcellus gas shale in the Northeast US would seem an obvious source for rail shipments of natural gasoline for example. Early reports of Utica production in Eastern Ohio also indicate high levels of lease condensate production.

These alternative transport methods may have to take more of the shipping burden than expected if the Northern Gateway pipeline is delayed. So far Northern Gateway has attracted significant environmental protest and opposition in British Columbia. If the pipeline is not built then an additional 200 Mb/d of diluent supply will be needed to meet demand.

One mitigating factor that could improve the diluent supply situation is the increase of shipments of Western Canadian bitumen to market by rail using special tank cars with heated coils. The important difference between this delivery method and pipelines is that the bitumen requires far less diluent when transported this way. Two bitumen by rail alternatives have emerged. The first is “railbit” that is an 85:15 bitumen to diluent mixture that requires insulated railcars and the second is raw bitumen that has to be transported in special rail tank cars with heated coils and has no diluent. These alternatives to the traditional 70:30 bitumen to diluent dilbit ratio potentially alter the economics of rail shipment versus pipeline. First the quantities of diluent are reduced by 50 percent or more and second the quantities of “real” crude increase accordingly. That is less diluent to ship and pay for and more bitumen to sell. These methods are already a reality. PBF refining is planning to deliver 40 Mb/d of raw bitumen crude to its Delaware City, DE refinery by heated coil rail tank car. Terminals are being constructed on the Gulf Coast in Mobile, Alabama, and Natchez, Mississippi, to handle railbit deliveries (we will cover these in more detail in an upcoming blog in our crude by rail series).

So far these alternatives have not moved significant quantities – perhaps 50 Mb/d by the end of 2012. Canadian producers that have pipeline capacity to ship heavy crude from Edmonton continue to do so and are unlikely to give up their capacity any time soon. However, the pipelines are congested so that new production is attracted to transport alternatives like rail. There are some good indications that Canadian producers are interested to pursue the rail car approach. The recently released US State Department Keystone XL Supplemental Environmental Impact Study includes a market impact section that reviews the possibility of Canadian tar sands moving by rail if Keystone is not approved. The report cites new orders for 28,000 insulated rail tank cars as evidence of producer interest and also estimates that the savings in diluent cost compare favorably to the difference between pipeline and rail cost.

Talking about the fate of Keystone brings us to one last factor that impacts Canadian diluent demand and that is the level of Canadian tar sands production. Our forecasts in this blog have assumed that production will find a market. If the pipeline capacity to move dilbit to market does not materialize that will obviously impact diluent demand. Also if the price of crude oil falls below $60/Bbl for an extended period of time then the production and transport economics of tar sands crude do not look good. That will at least slow down production in the short term and curtail expansion plans. We talked about this possibility last year in “What Price Crude Recovery” and it is certainly true that Canadian heavy crude production is the most vulnerable to cutbacks given its high cost.

In this two part series we have established that Canadian demand for diluent continues to increase at a rapid rate based on current production forecasts for heavy crude. Diluent supply already relies on imports from the US and those volumes will increase. Significant quantities of US natural gasoline are already being exported to Canada. Additional diluent requirements are being met by shipments of lease condensate. US production of lease condensate will more than meet expanding Canadian diluent requirements. The greater challenge is finding the pipeline capacity to deliver the diluent volumes and that will get tricky unless the Enbridge Northern Gateway pipeline is built by 2017. However, after the 2012 “year of the rail tank car” we now expect that rail will fill any transportation gap. What is more surprising is that increased movements of raw bitumen by rail in coming years could reduce the demand for diluent and solve the transport dilemma that way. There is also the ever-present threat to heavy crude production that lower crude prices could curtail planned production increases. We conclude that there will be no shortage of diluent for Canadian bitumen producers and that forecast demand may end up being optimistic if the Keystone XL and Northern Gateway pipelines do not get built. Lease condensate holders will once again be left searching for a source of demand.