It’s been a devastating few weeks for the natural gas market. Sure, Shale Era abundance was supposed to keep gas prices from skyrocketing — and it generally has. But seriously? Henry Hub gas sinking below $2/MMBtu — and staying there, in the depths of the winter heating season? Prices have stabilized a little as a few E&Ps announced cutbacks in capex and gas-focused drilling, but gas-storage levels are abnormally high, coal-plant retirements have trimmed opportunities for coal-to-gas switching, and any significant gains in LNG exports aren’t going to happen until this time next year. With all that, you’ve gotta ask — as we do in today’s RBN blog — how low could natural gas prices go?

Join us at our historic 20th School of Energy!

School of Energy: Foundations is a two day, in person conference designed to help energy professionals better understand the forces shaping crude oil, natural gas, NGLs, refined products, and petrochemicals.

Attendees will learn from RBN experts, work with Excel based analytical models, participate in Q&As, and network with industry peers.

Build the foundation to better navigate volatile energy markets.

In observance of Good Friday, we are giving our analysts a break and replaying a recently published blog on natural gas markets. If you didn’t read it then, this is your opportunity to see what you missed!

It came as no surprise to anyone paying attention that natural gas prices would be soft as a down pillow in 2023. We said in our annual prognostications blog in January 2023 — 15 months ago — that the hiatus in adding new LNG export capacity would trigger an oversupplied market, and most everyone else in the gas world agreed. The market bearishness only intensified in the second half of last year when an El Niño weather pattern settled in for the first time in four years, correctly portending unseasonably mild winter weather in the northern tier of the Lower 48. Meanwhile, reasonably strong global crude oil prices have continued to incentivize U.S. producers — particularly those in the low-cost Permian — to keep their foot on the gas (so to speak), thereby producing massive volumes of associated gas and pushing Lower 48 natural gas production to a record 106 Bcf/d in December 2023.

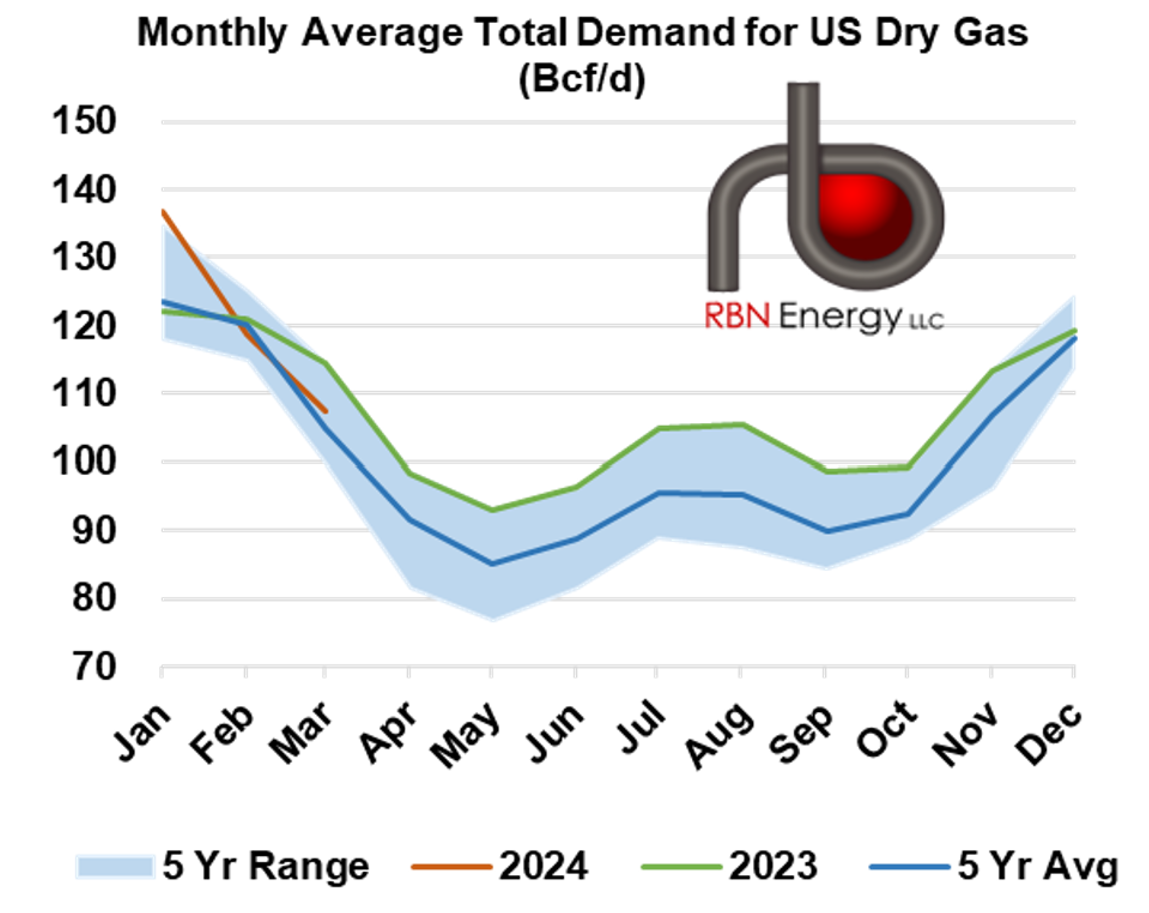

Figure 1. Net U.S. Natural Gas Demand by Month, Including LNG and Pipeline Exports. Sources: EIA, RBN analysis