Growing Canadian production of oil sands bitumen requires diluent to blend it to pipeline flow specifications. The resulting demand for diluent exceeds local Canadian supply from plant condensate production (aka, natural gasoline) – leading to imports from the US of more than 150 Mb/d in 2013 – a figure expected to grow to 460 Mb/d by 2018. That expectation for future import growth is based on the assumption that Canadian condensate supplies would remain relatively flat at about 140 Mb/d. But could the developing Duvernay gas shale play in Western Alberta turn those estimates on their head? Today we investigate the consequences for US condensate demand.

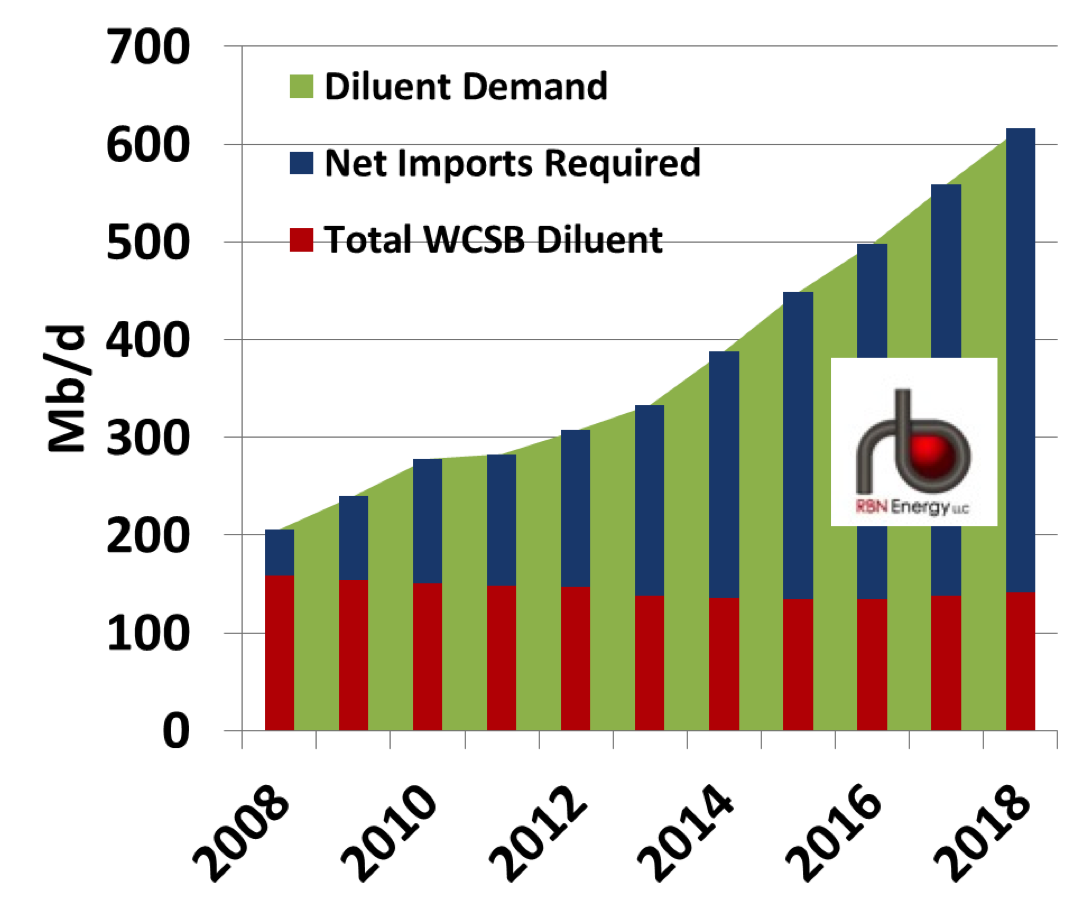

Canadian demand for light hydrocarbon material used as a diluent to reduce the viscosity of oil sands bitumen - allowing the resulting “dilbit” blend to flow in pipelines - is expected to increase significantly over the next 4 years as bitumen production takes off. The green shaded area in Figure 1 below represents Canadian demand based on the typical requirement to blend raw bitumen with 30 percent diluent – doubling from just over 300 Mb/d in 2013 to more than 600 Mb/d in 2018. The only constraint on these demand levels would be the large scale development of crude by rail transport that reduces diluent demand to less than 20 percent – but the extent of this development is still unclear (see Railbit Train to Natchez). We don’t have big time railbit volumes baked into the forecast below. When we last looked at sources of supply for diluent back in December 2013 (see Utica Condensate Routes to Canada) the conventional wisdom was that local Canadian production – shown in red in Figure 1 – would peak at about 140 Mb/d and then stay flat over the next four years. The result would be a rising need for Western Canadian bitumen producers to import diluent supplies from overseas (the blue bars in Figure 1) – rather neatly coinciding with a growing surplus of such materials in the US.

Figure 1

Source: RBN Energy

Diluent supplies are typically sourced from one of the three main branches of the condensate family, namely lease or field condensate produced at the wellhead when liquids rich natural gas is brought to the surface, plant condensate (aka natural gasoline or pentanes plus) produced by natural gas processing plants and naphtha produced from petroleum refining. [Canadian producers also use light synthetic crude oil (SCO) produced by upgrading bitumen as a diluent.] As we explained in Like a Box of Chocolates – The Condensate Dilemma, supplies of all of these condensate range materials in the US are increasing faster than demand can keep up – providing a ready surplus to supply Canadian needs.

About the song

The song “Da Doo Ron Ron” has been recorded by many artists but the original was a hit in 1963 for the Crystals - produced by Phil Spector

Comments

Does the first chart of projected condensate demand include recycled condy from the various diluent recovery units at the upgraders and rail loading centers? Would be interesting to get an estimate on what % is recycled. Seems like if proportionately more crude bit. is shipped by rail, WCSB demand for condensate might not be as high as expected.

In reply to Condensate Demand by Carl Evans

Hi Carl,

Agreed. I did say in the blog that the chart in Figure 1 does not include any "railbit" estimate and the same goes for recycling diluent. These will also reduce the ultimate demand for diluent imports - especially if more rail is used to ship crude and if diluent recovery units become common. One caveat to the "recycle" concept is that if Canadian supplies become abundant due to Duvernay or other shale plays taking off - the result would presumably reduce the price of condensate in Edmonton. If Edmonton condensate is cheaper than the Gulf Coast, the incentive to recycle by (for instance) backhauling diluent from the Gulf, would disappear.

Sandy

In reply to Hi Carl, by Sandy Fielden

If Kaybob Duvernay condensate were to back out incremental Gulf Coast supply, wouldn't that lead to an oversupply situation (decreased prices) down there as well? It appears as though condensate is the economic driver for Canadian drillers. Even at lower gas prices they kept expanding that area. Would US producers ever be at risk of production growth decline if they couldn't find a home for their condensate, or would they just accept a discount on their by-products to be able to move it?

Sandy,

Seems to me that emergence of the Kaybob Duvernay play as a replacement for US condensate is yet another negative factor in the rapidly developing Gulf Coast storage glut you described today.