It seems like everybody and his uncle are planning new methanol production capacity in the U.S. The economics certainly are compelling. Low natural gas prices are attracting methanol projects like a magnet, especially to the Gulf Coast; domestic and foreign demand for methanol is rising; and methanol prices are as high as they’ve been in five years. But companies are always looking for an angle, a competitive edge, a chance to make their project the most cost-efficient—and profitable—of all. Today, in “Cheap Trick: ‘I Want You to Want Me(thanol)’”--we consider Valero Energy’s methanol initiative and its cheap trick: a plan to add 1.6 million to 1.8 million tons per annum (MMtpa) of methanol capacity for an investment of only about $700 million. That’s around half what it would normally cost.

Valero’s ace-in-the-hole? Its planned methanol plant at the company’s St. Charles refinery in Norco, Louisiana, will be fed with syngas - something every methanol plant needs - by the same process that provides hydrogen to its hydrocracker – saving the company from developing the feedstock from scratch.

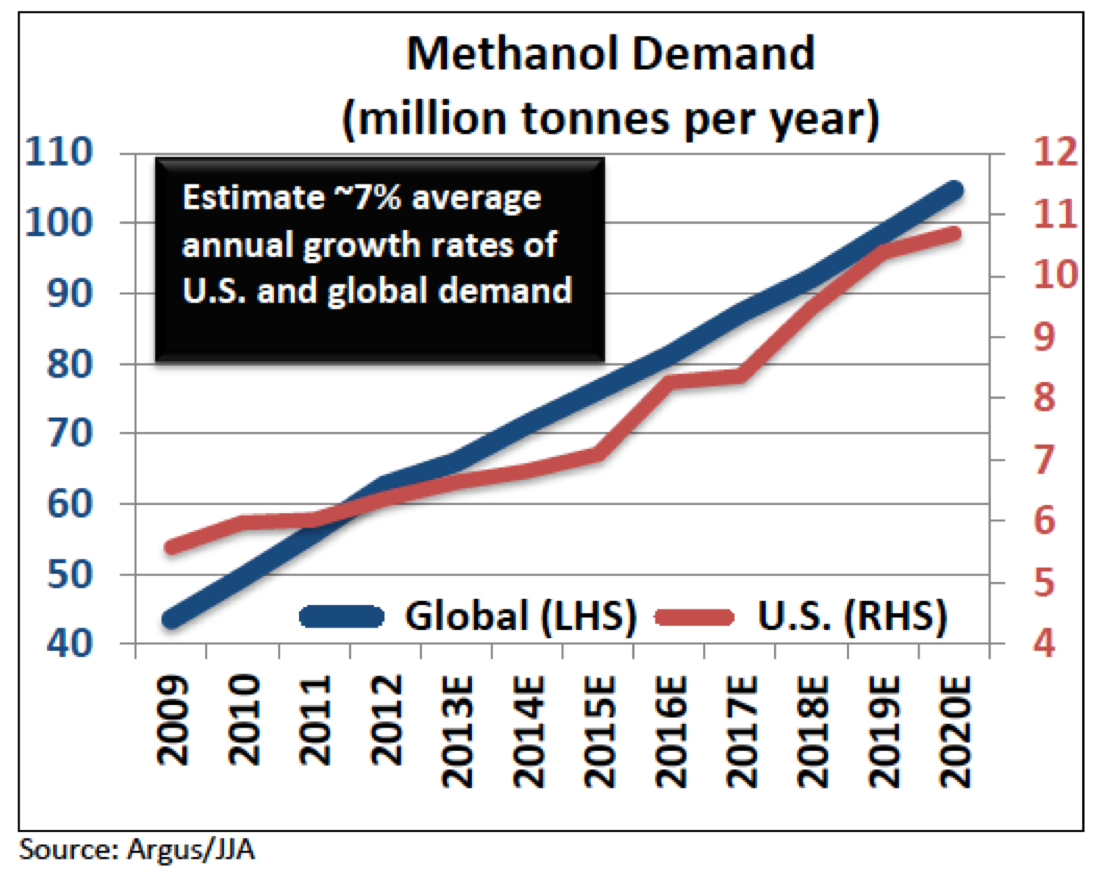

Methanol is a very basic chemical feedstock, used to make formaldehyde, acetic acid and petrochemical intermediates that, in turn, are used to make plastics, synthetic fibers, paints, resins and solvents, among many other things. . Demand has been rising and it’s expected to continue to, both here and abroad (see Figure 1). The U.S. in the past 20 years has yo-yoed from being the world’s largest methanol producer to a big net importer, and—with all the new methanol capacity now being planned (see Ignition Timing Countdown: 1.4 Bcf/d Increase in Natural Gas Demand from Methanol?) We’re now on the verge of becoming “methanol independent,” and maybe even an exporter to boot. The numbers tell the story. U.S. methanol capacity in the mid-1990s totaled about 10 MMtpa, but by 2005, with natural gas prices on the rise, more than nine-tenths of that capacity had been taken offline (much of it scrapped), a victim mostly of higher, volatile natural gas prices. Now, with once-unthinkable volumes of shale gas available at low and more stable prices, U.S. methanol production is making a big comeback. If all the new methanol capacity being planned or talked about is actually built (and no, it almost certainly won’t be), we could see 15 MMtpa or more of new capacity within five years. Methanol prices remain firm: Methanex’s non-discounted reference price for October stands at $549/mt, up from $439/mt a year ago and the highest since the price spiked higher than $800/mt in late 2007 and early 2008. Methanex’s Asian posted contract price stands at $490/mt, up $55/mt from a year ago and, again, the highest it’s been since 2008.

Figure 1: Source Valero Investor Presentation

So, what’s Valero’s angle regarding methanol production at St. Charles? To really simplify things, methanol production takes three steps. First, a steam-methane reformer (SMR) converts natural gas into a synthesis gas (syngas) consisting of carbon monoxide, carbon dioxide, water and hydrogen. Next, hydrogen is stripped from the syngas, and third, methanol is produced through a catalytic synthesis of the syngas. Valero is already using hydrogen in their refinery that is produced from an existing SMR under a long-term contract with Praxair. To feed the Methanol plant, Valero will tap supplies of syngas from the same SMR they get hydrogen from and save the cost of building their own plant to make feedstocks.

About the song

"I Want You to Want Me" was written by Rick Nielsen and appeared originally as the fourth song on side one of Cheap Trick's second album, In Color. Released as the first single from the album in September 1977, it failed to chart in the U.S. However, when the song was released as a single in Japan, it went to #1 there, and paved the way for CBS to release the live album Cheap Trick at Budokan in 1979 in the states. When the live version of the song from that album was released as a single in April 1979, it went to #7 on the Billboard Hot 100 Singles chart and has been certified Gold by the Recording Industry Association of America (RIAA). Personnel on the record were: Robin Zander (lead vocals, rhythm guitar), Rick Nielsen (lead guitar, backing vocals), Tom Petersson (bass, backing vocals), and Bun E. Carlos (drums).

Cheap Trick at Budokan was recorded live in Japan in April 1978; the album was produced by Cheap Trick. Released in the U.S. in February 1979, the LP went to #4 on the Billboard Top 200 Albums chart. It has been certified 3X Platinum by the RIAA. Two singles were released from the album.

Cheap Trick are an American rock band formed in Rockford, IL, in 1973. Eight members have passed through the band since its inception, with Robin Zander and Rick Nielsen being in the fold from the start. The band has released 19 studio albums, six live albums, 17 compilation albums, four EPs, and 64 singles. Cheap Trick has sold more than 20 million records worldwide and was inducted into the Rock and Roll Hall of Fame in 2016. The band continues to record and tour, with a North American tour scheduled to begin in late April.

Comments

I don't see why Valero should spread into Methanol for MethanoI just because Gas Producers are looking for opportunities to move their gas into markets linked to oil, and Oil/Gas ratio is low.

Refiners' goal is to build demand for their oil products and supply feedstock at the lowest cost... so I think it's a big mistake for a refiner to step into methanol unless the primarly business objective is too convert cheap methanol feedstock into Gasoline.

Simon