With the UN’s Climate Change Conference (COP 26) in Glasgow just over a month away, it’s natural to reflect on the progress achieved since the Paris Agreement (signed at COP 21), which is approaching its sixth anniversary. In the past half decade, the world has taken tremendous strides toward decarbonization – not only in rhetoric, but in real and substantial investment. Green hydrogen and carbon capture are among the notable solutions many are pursuing to that end. But perhaps no green business has been in the spotlight as much recently as renewable diesel. Low-carbon fuel standards have spurred a lucrative renewable diesel market that refiners are lining up to access, with units being built and planned across North America. The nationwide buildout is being underwritten by the states that have enacted policies to induce low-carbon solutions, and while the Golden State is paramount among them, Californians are not alone. The largess being generated by those policies is so substantial that it will have an impact on and may incubate other low-carbon technologies that can be paired with renewable diesel to create even lower-carbon fuel sources and capture more of the credits that are ultimately driving the economics of the energy transition. In today’s RBN blog, we identify key manufacturing centers for low-carbon fuel supply growth, the at-times lengthy route the fuels may take to LCFS markets, and the economic incentive structure that justifies all those costs.

The significant level of investment targeting the renewable diesel (RD) market has prompted us to blog prolifically on the subject recently, most notably in our Come Clean blog series developed with our good friends at Baker & O’Brien which focuses on the laws and regulations aimed at reducing carbon-dioxide and other greenhouse gas (GHG) emissions from the transportation sector in the U.S. and Canada. We published Part 7 of the series on sustainable aviation fuel (SAF) in August and Part 8, about hydrogen as a transportation fuel, is in the works. To keep this blog a manageable length, we’ll be referring back to concepts from that series.

We start with a quick review of the policies motivating the buildout. In Part 1, we provided an overview of various policies that have been adopted and are being discussed to reduce GHG emissions from transportation fuel use. We noted several approaches being taken, including fuel economy standards, renewable blending requirements, zero-emission vehicle mandates, and low carbon fuel standards (LCFS). In Part 2, we focused on California’s LCFS, which was first implemented in January 2011 and subsequently enhanced. Now, California is the center of the LCFS universe, with Oregon and British Columbia also out front.

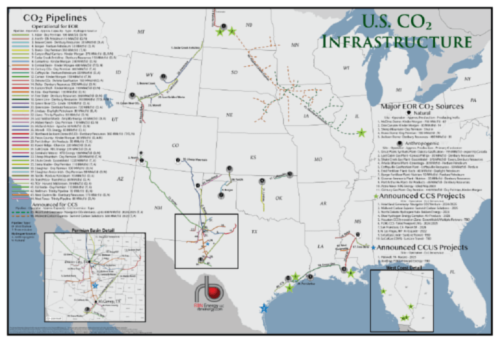

RBN Energy’s US CO₂ Infrastructure map brings together legacy Enhanced Oil Recovery (EOR) assets, as well as announced large-scale Carbon Capture and Sequestration (CCS) and Carbon Capture, Utilization and Sequestration (CCUS) projects, all in our signature concise, accurate, and intelligible style.

About the song

"Californication" was written by Anthony Kiedis, Flea (Michael Balzary), Chad Smith, and John Frusciante (Red Hot Chili Peppers), and it appears as the sixth song on Red Hot Chili Peppers' seventh studio album of the same name. Released as a single in May 2000, the song went to #1 on the Billboard Alternative Airplay and Mainstream Rock charts, and #69 on the Billboard Hot 100 Singles chart. It has been certified 5x Platinum by the Recording Industry Association of America. The song talks about the dark side of Hollywood and the exploitation of culture through the music and movie industry. Personnel on the record were: Anthony Kiedis (lead vocals), Flea (bass), John Frusciante (guitar, organ, backing vocals), and Chad Smith (drums).

The album, Californication, was recorded between December 1998 and March 1999 at Cello Studios in Los Angeles, with Rick Rubin producing. Released in June 1999, it went to #3 on the Billboard Top 200 Albums chart; and it has been certified 7x Platinum by the RIAA. Six singles were released from the LP.

Red Hot Chili Peppers are an American rock band formed in 1993 by fellow Fairfax High School members Anthony Kiedis and Flea in Los Angeles. They have sold over 90 million records worldwide. The band has released 11 studio albums, two live albums, five EPs, and 61 singles. They have won four American Music Awards, three Brit Awards, six Grammy Awards, and eight MTV Video Music Awards. They are members of the Rock and Roll Hall of Fame and have a star on the Hollywood Walk of Fame. Fourteen members have passed through the group since its formation. Keidis, Flea, Smith, and Frusciante continue to record and tour as the Red Hot Chili Peppers. Rick Rubin is currently producing a new album with the band, with a world tour being planned that will begin in June 2022.