The U.S. Gulf Coast is poised to experience another big wave of new LNG export capacity, and this time it will be joined by new capacity coming online in both Mexico and Canada. The more than 13 Bcf/d of incremental natural gas demand from North American LNG projects starting up over the next five years will have significant effects on U.S. and Canadian gas producers, gas flows and (quite likely) gas prices, which have been deeply depressed for more than a year now. In today’s RBN blog, we provide updates on the 10 LNG export projects in very advanced stages of development in the U.S., Mexico and Canada, detail the expected ramp-up in LNG-related gas demand and discuss the potential impact of rising LNG exports on gas prices.

Visualize the infrastructure behind U.S. NGL movement.

The U.S. NGLs Map provides a comprehensive view of the transport, processing, and export networks moving NGLs across the U.S.

The Biden administration’s late-January announcement of a temporary pause in approving new LNG export licenses to non-Free Trade Agreement (non-FTA) countries — or extending existing licenses, barring special circumstances — grabbed headlines and raised energy-industry hackles. But while the pause has cast a shadow over several LNG export proposals nearing final investment decisions (FIDs), it has had little or no impact on the long list of projects with those Department of Energy (DOE) export licenses already in hand. In fact, as we said in How Do You Like Me Now?, the pause may well have a positive effect on a few U.S. and Mexican projects that already have non-FTA licenses — as well as Canadian projects that don’t need them — but had not yet received a final go-ahead from their developers.

(Two quick sidebars: First, a long list of major LNG-importing countries and regions fit into the non-FTA category, including the U.K., the European Union (EU), Japan, China, India, Brazil and Argentina. Second, a federal court judge in Louisiana on July 1 ordered that the pause be “stayed in its entirety, effective immediately,” but it’s unclear what the practical effects of that ruling will be.]

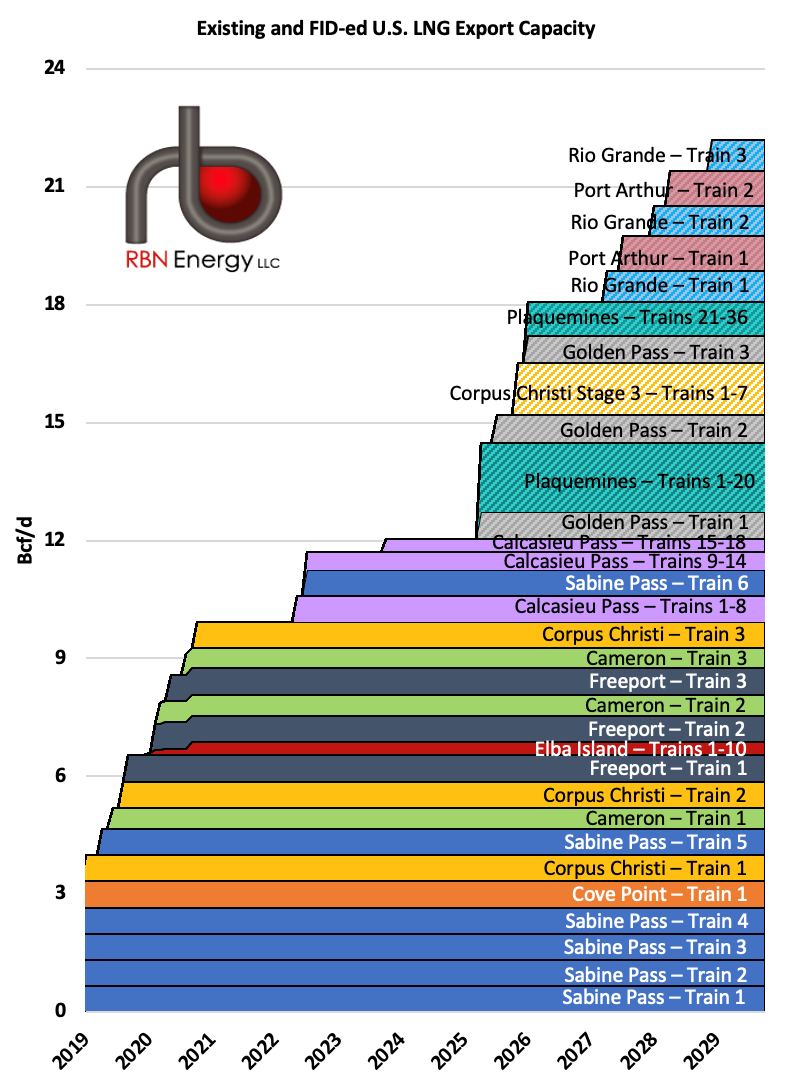

In any case, there is a long list of North American LNG projects — large, medium and small — that have reached FID and are either under construction or about to enter that phase. We’ll start with the U.S., which already has 12 Bcf/d of LNG export capacity in operation and is expected to add another 6.4 Bcf/d by early 2026 and an additional 3.9 Bcf/d in 2027-29 (see Figure 1 below). That would put U.S. LNG export capacity at more than 22 Bcf/d by the end of this decade.

Figure 1. Existing and FID-ed U.S. LNG Export Capacity. Source: RBN’s LNG Voyager

About the song

“Big Wave” was written by Jeff Ament and appears as the eighth song on Pearl Jam’s eighth studio album, Pearl Jam. The song exemplifies the band’s return to their roots on the album, with a more forceful rock and roll edge to their sound. Personnel on the record were: Eddie Vedder (lead vocals, guitar), Jeff Ament (bass), Stone Gossard, Mike McCready (guitars), and Matt Cameron (drums, percussion, backing vocals).

The album Pearl Jam was recorded between November 2004 and February 2006 at Studio X in Seattle. Produced by Adam Kasper and Pearl Jam, it was released in May 2006. The album went to #2 on the Billboard 200 Albums chart and has been certified Gold by the Recording Industry Association of America. It was the band’s first studio album in almost four years and represented a more collaborative effort on the songwriting for the LP. Pearl Jam supported the album with a world tour in 2006. Three singles were released from the album.

Pearl Jam is an American rock band formed in Seattle 1990 from the ashes of Mother Love Bone. Mother Love Bone broke up after the heroin overdose of their lead singer, Andrew Wood, days before their debut album, Apple, was scheduled for release in March 1990. Band members Stone Gossard and Jeff Ament recruited singer Eddie Vedder and put together Pearl Jam, initially billing themselves as Mookie Blaylock. They changed their name to Pearl Jam after signing with Epic Records in 1991. The band was one of the standard-bearers of the Seattle grunge movement. They have released 12 studio albums, 23 live albums, three compilation albums, one EP and 42 singles. Pearl Jam was inducted into the Rock and Roll Hall of Fame in 2017. Vedder, Gossard, Ament and McCready went through four drummers before settling on Matt Cameron, who has sat at the drum throne with the band since 1998. Pearl Jam continue to record and started a world tour in late June 2024.