E&P investors have historically been a skittish lot, and for good reason. In the second half of the 2010s, the S&P E&P Index had as many sudden ups and downs as Coney Island’s famous Cyclone roller coaster, culminating in a near crash in early 2020 as equity prices bottomed out at one-tenth their peak. A fairly smooth annual return of nearly 7% over the 2021-to-Q2 2024 period has wooed money back to a sector that now prioritizes shareholder returns. But wariness remains, especially as natural gas prices cratered to three-decade summer lows. In today’s RBN blog, we analyze the balance sheets and budgets of the U.S. gas-focused producers we track to determine if there are causes for concern.

Join us at our historic 20th School of Energy!

School of Energy: Foundations is a two day, in person conference designed to help energy professionals better understand the forces shaping crude oil, natural gas, NGLs, refined products, and petrochemicals.

Attendees will learn from RBN experts, work with Excel based analytical models, participate in Q&As, and network with industry peers.

Build the foundation to better navigate volatile energy markets.

As we reported recently in Part 1 of this series, pre-tax operating profits for the 39 E&Ps we monitor rebounded slightly: up 1.8% in Q2 2024 to $12.25/boe ($16.6 billion) from $12.04/boe in Q1 2024. As a whole, the group outperformed the turbulent 2015-19 period but fell short of results in the post-COVID years. The primary reason was that low natural gas realizations nearly offset the impact of higher liquids (crude oil and NGLs) realizations for the entire group, as the production weighting of the 39-E&P group was 36% oil, 17% NGLs and 47% natural gas. The Oil-Weighted producers, with output that is 77% liquids, earned $20.11/boe ($9.6 billion) in Q2 2024, slightly higher than the $20.04/boe ($9.2 billion) they earned in Q1 2024. Diversified E&Ps, which produce 35% natural gas, earned $18.21/boe ($7.9 billion) in Q2 2024, slightly lower than the previous quarter of $18.59/boe and $1.50/boe lower than the Oil-Weighted group.

Engineering Company Wood Selected for DeLa Express Gas Pipeline

However, the Gas-Weighted producers, with a portfolio weighting of just 16% liquids, had a brutal quarter. Pre-tax operating profits for the 11 gas-focused E&Ps we cover have been descending into the red in 2024, reporting an aggregate $850 million in losses as revenues per boe (barrel of oil equivalent) dipped during Q2 2024 to the lowest level since the pandemic price crash in 2020. With no short-term price relief in sight, results raised concerns over the financial stability of a peer group that averaged debt-to-capital ratios of more than 40% in the 2015-20 period while reporting net losses in four of those six years. With that in mind, we decided to analyze the Gas-Weighted group’s balance sheet, capital spending trends and cash allocation to determine if current low prices do, in fact, threaten their financial stability.

Leverage

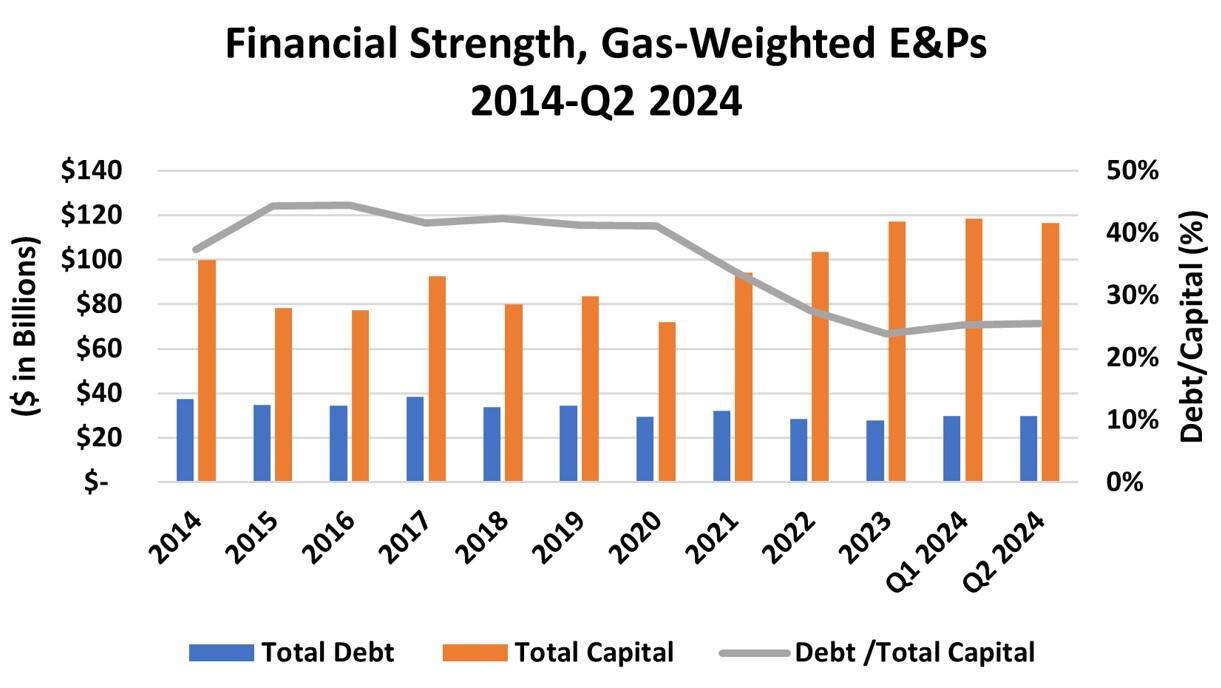

Spoiler alert: Our analysis belies those concerns, revealing a peer group whose members have dramatically stabilized their balance sheets by taking advantage of record profits from elevated gas prices in 2021-22. Revenues per boe for gas-focused E&Ps doubled from $12.48/boe in 2020 to $24.02/boe in 2021, then rose another 62% to $38.85/boe in 2022. As shown in Figure 1 below, Gas-Weighted producers took advantage by sharply lowering the average debt-to-capital ratio (gray line) from 41% in 2020 to 24% in 2023, the lowest among our three peer groups. Debt per boe of proved reserves also plunged to $1.21 after averaging more than $2/boe over most of the last 10 years. Lowest in the group were Range Resources ($0.59/boe) and Antero Resources ($0.51/boe). The primary outlier was Haynesville producer Comstock Resources, which had a debt-to-boe of $3.20 and a debt-to-capital ratio of 47%.

Figure 1. Financial Strength, Gas-Weighted E&Ps, 2014-Q2 2024.

Source: Oil & Gas Financial Analytics, LLC

About the song

“Bad Moon Rising” was the lead single from Creedence Clearwater Revival’s third album, Green River. Written and produced by John Fogerty, the song was recorded at Wally Heider’s Studio in San Francisco in March 1969. The single reached #2 on the Billboard Hot 100 singles; the Green River LP went to #1 on the Billboard 200 album chart.

John Fogerty has said he wrote “Bad Moon Rising” after watching “The Devil and Daniel Webster,” and was inspired by a scene in the movie involving a hurricane. The last line of the chorus — “There’s a bad moon on the rise” — has often been misheard as "There’s a bathroom on the right," and Fogerty has been known to sing that line sometimes in concert. The song has been used in numerous films and television shows.

Creedence Clearwater Revival, also referred to as CCR, included John Fogerty (lead and backing vocals, lead guitar and piano), Tom Fogerty (rhythm guitar), Stu Cook (bass) and Doug Clifford (drums). The band was formed in the San Francisco Bay area in 1967 and released seven studio albums from 1968 to 1972 — they disbanded in October of that year. John Fogerty went on to have a successful solo career and still tours today. Tom Fogerty (John’s older brother) released several solo albums before passing away in 1990. Stu Cook and Doug Clifford still tour today as Creedence Clearwater Revisited, playing a repertoire of CCR songs. Creedence Clearwater Revival was inducted into the Rock and Roll Hall of Fame in 1993.