Emission regulations require that companies planning new olefin crackers in EPA designated nonattainment areas like Houston must buy emission credits prior to construction. The market for credits in Houston for one criteria pollutant – volatile organic compounds (VOCs) skyrocketed from $4.5K/ton in 2011 to $300K/ton this month. The scarcity of emission credits and their rising price threaten to constrain or delay new petrochemical plant builds and will continue to hamper plant development and expansions in the Gulf Coast region. Today we describe the challenge new projects face.

|

Statistics and prices in this posting have been provided by Element Markets LLC, a leading environmental credit marketing company. For more information see www.elementmarkets.com |

Yesterday we explained the complex emissions rules governing new plant construction in regions designated as nonattainment areas by the Environmental Protection Agency (see All I need is the Air That You Cleaned and to Pay You). If you are not familiar with these regulations, you might want to read that posting before you jump into this one. To recap we described Clean Air Act (CAA) rules relating to new sources of emissions such as those created when building new chemical processing plants (olefin crackers). We explained the mechanism that allows a plant operator in one of the ozone nonattainment areas to permit a new plant by acquiring emission reduction credits (ERCs) from retired facilities or processes to offset new emissions from their project. The Texas Commission for Environmental Quality (TCEQ) administers the ERC scheme in the Lone Star State. Companies register plant retirements or process abandonments with TCEQ to receive ERC credits that can be used by them or sold to others in a bilateral market. The number of offsetting ERCs required for building new plants in nonattainment areas increases with the severity of that area’s nonattainment. ERCs must also come from the same area and be for the same criteria pollutant as the new plant emissions.

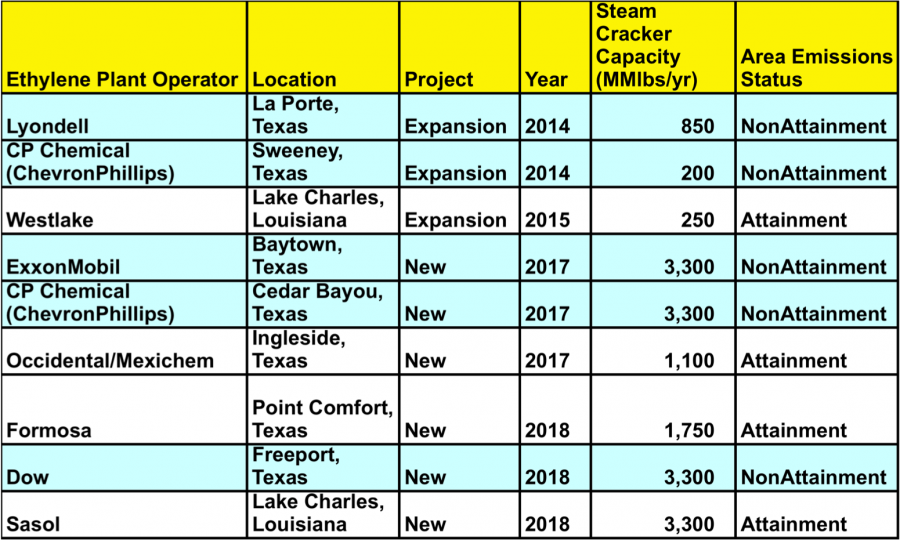

The worst nonattainment area in Texas is the Houston/Galveston/Brazoria region – known as HGB. Despite its poor air quality the HGB area is experiencing significant growth in the number and size of announced projects in the petrochemical sector. The table below lists 9 currently announced projects to expand ethylene crackers or build new plants in the US. The five projects highlighted in blue are located in the HGB nonattainment area. The other 4 are in attainment areas and do not need to be concerned with emission offsets. [Note that to keep things simple we didn’t include two plants in nonattainment areas that are not in HGB – a Dow plant in Plaquemine Parish, La and the proposed Shell plant in Pennsylvania]. Each of the five highlighted projects will likely have the potential to emit over 25-100 tons per year of Volatile Organic Compounds (VOC) and nitrogen oxide (NOx). That means they will have to secure ERCs in HGB – at a time when these credits have become scarce – especially those for VOCs.

[Note: Two ethylene plants not included in this list are also in nonattainment areas

outside the Houston/Galveston/Brazoria region – the Dow expansion at Plaquemine

Parish, La and the new Shell plant in Pennsylvania.]

Source: Element Markets LLC (Click to Enlarge)

This scarcity in the HGB region came about in 2011 after a period when ERCs for VOC’s were relatively easy to come by in 2009. That was after the financial meltdown had depressed heavy industry leading to many plant retirements and no new construction to use the credits. Once the economy started to recover in 2011 and energy costs began to fall as shale production of natural gas boomed, companies began to start planning ethylene plant expansions on the Gulf Coast as well as other industrial process facilities such as fractionators and liquefied natural gas (LNG) plants. Companies like CP Chemical and others found that there were no credits on the TCEQ books to buy. So they started doing deals with companies operating marginally economic facilities to shut down those plants to ‘make’ credits. The way that works is that company “A” needs to offset a new plant emission so they identify company “B” that has an old plant or process with emissions that match those company “A” needs to offset. Company A then pays company B to shut down their plant or process and transfer the resulting ERC credits to use for their offset.

This process can be tricky because when a plant closes down or cuts back its emission reduction must be registered with the TCEQ in order to receive the credits. Once registered, the credits can be applied as an offset at any time during the subsequent 5 years before they expire. So if you pay a company for presold credits in this way then you need to monitor when their plant closes and when the credits are registered with TCEQ to avoid the credits expiring before you need to use them. But if the “presold” credits you buy in this fashion have not been registered there is no guarantee of their volume – so there are risks attached to the strategy. Nevertheless the scramble for credits in HGB (actual and presold) increased the price per ton of ERCs for VOCs from $4,500 to $125,000 between January and December of 2011.

And as new projects were announced the price of VOC ERCs in HGB continued to skyrocket. The chart below shows data from Element Markets tracking the price of VOC credits (red line, right axis) since 2009 as well as the volume of VOC ERCs that have been traded (blue bars, left axis). As you can see the volume of trades has been very small in the past two years and the price has increased exponentially. Element Markets auctioned off the last available registered VOC ERCs on May 23rd of this year (2013) for $270,000/ton as part of a package with NOx ERCs at $151,000/ton. Those ERCs belonged to the City of Houston that pocketed over $5MM from the deal.

Join Backstage Pass to Read Full Article