Western Canada’s natural gas market never really seems to catch a break. Prices this winter have remained well below those across much of the rest of North America thanks to an all-too-common combination of insufficient pipeline export capacity from the region, bloated gas storage and robust supply growth. Even with forward price prospects for much of the rest of the continent looking buoyant, with more gas expected to head to expanding Gulf Coast LNG terminals and a storage-refill season that will be stronger than last year, price upside for Western Canada looks to be minimal at best and will be partly dependent on the rate of gas intake to LNG Canada, as we explain in today’s RBN blog.

We all love those movies about the wrongly convicted individual sent to prison, only to be released (or escaping!) later thanks to a combination of legal work, tenacity and plain stubbornness in overcoming the unjust imprisonment. Western Canada’s gas producers were probably hoping that this most recent winter heating season might provide a similar storyline for its primary price marker, AECO, and its regional cousin, Station 2, which have been imprisoned inside Western Canada’s all-too-often pipeline-constrained and oversupplied regional market, with prices that have frequently disconnected from pricing action elsewhere in North America.

Join us at our historic 20th School of Energy!

School of Energy: Foundations is a two day, in person conference designed to help energy professionals better understand the forces shaping crude oil, natural gas, NGLs, refined products, and petrochemicals.

Attendees will learn from RBN experts, work with Excel based analytical models, participate in Q&As, and network with industry peers.

Build the foundation to better navigate volatile energy markets.

Hopes were high at the start of the heating season in November that the right combination of colder weather (and the strong demand to go with it), a healthy drawdown of bloated regional gas storage, some self-imposed production constraints, modest growth in pipeline egress capacity from the region and, importantly, a gradual ramping up of gas supply into LNG Canada, would do the trick and unlock the door to the outside world with a better connection to higher gas prices across the continent. That was a long list, and everything had to go just right to pull off that escape.

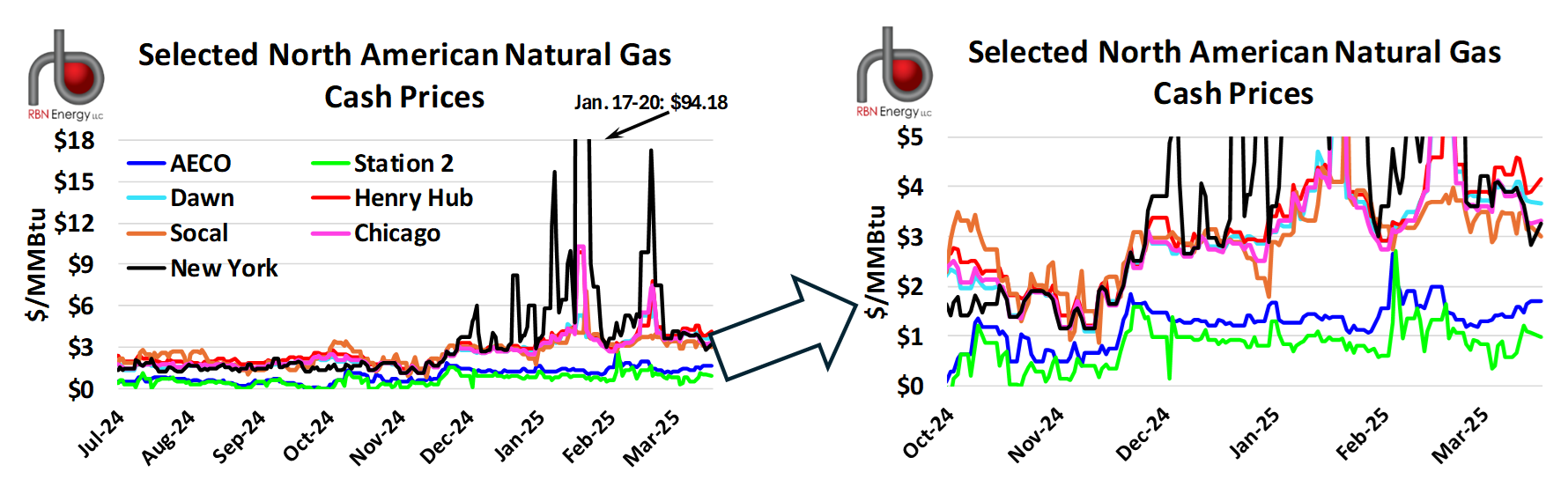

Well, it didn’t quite pan out as hoped. AECO (blue line in Figure 1 charts below) and Station 2 (green line) cash prices this past winter have been locked away in the market’s dungeon the entire heating season. Gas cash prices in many other regional markets (compare to red, orange, pink and black lines) were already trending upward at the start of the heating season and then soared on the arrival of colder-than-average weather and storms across parts of Canada and the U.S. in mid-January, which was followed by another round of colder-than-average temperatures for most of North America for most of February and a second price surge. No matter where you looked, cash prices elsewhere reacted as space heating demand cranked up, and immense storage withdrawals followed to keep regional markets adequately supplied. Even Canada’s other major cash price marker of Dawn (light-blue line) in southern Ontario —closest to Canada’s major population centers in the east and large U.S. centers in the Midwest and Northeast — ramped up to much higher levels this winter and has held there since.

Figure 1. Selected North American Natural Gas Cash Prices. Source: Bloomberg

About the song

“Folsom Prison Blues” was written by Johnny Cash and first appeared as the fifth song on side two of his debut solo album, Johnny Cash with His Hot and Blue Guitar! The song is based on an earlier tune, “Crescent City Blues,” written by Gordon Jenkins. It was first released as a single by Cash on Sun Records in December 1955 and went to #4 on the Billboard Hot Country Songs and #5 on the Billboard Best Sellers in Stores Singles charts. It also appeared later as the first song on side one of Cash’s first live album, Johnny Cash at Folsom Prison. Released as a single from the album in April 1968, it went to #1 on the Billboard Hot Country and #32 on the Billboard Hot 100 Singles charts. Interestingly, Folsom wasn’t Cash’s first prison concert. In 1958, he played at San Quintin State Prison in California, where a young Merle Haggard was present as an inmate. Personnel on the 1955 record were: Johnny Cash (vocals, acoustic rhythm guitar), Luther Perkins (electric lead guitar) and Marshall Grant (acoustic bass). Personnel on the 1968 record were: Johnny Cash (vocal, acoustic guitar), Luther Perkins, Carl Perkins (electric guitar), Marshall Grant (bass) and W.S. Holland (drums).

Johnny Cash with His Hot and Blue Guitar! was recorded between September 1954 and August 1957 at Sun Studios in Memphis with Sam Phillips producing. It was Cash’s debut album and contained four of his previous hit singles issued by Sun Records.

Johnny Cash at Folsom Prison was recorded live at Folsom Prison in Folsom, CA, in January 1968 and was Cash’s first live album. Produced by Bob Johnston, it was released in May 1968 and went to #1 on the Billboard Top Country and #13 on the Billboard 200 Albums charts. It has been certified 3x Platinum by the Recording Industry Association of America. One single was released from the LP.

Johnny Cash was an American country music singer and songwriter. Known as the “Man in Black” due to his stage apparel, his five-decade career in popular music incorporated elements of country, rockabilly, folk, blues, rock and roll, and gospel in his musical palette. He released 68 studio albums, 16 live albums, four soundtrack albums, 105 compilation albums, and 170 singles. He has sold more than 90 million records worldwide. He is a member of the Rock and Roll Hall of Fame, Country Music Hall of Fame, and Gospel Music Hall of Fame. Johnny Cash died in Nashville in September 2003 at the age of 71.