Last week (May 3 2013) a very late winter snowstorm crossed the Rocky Mountains into the upper Midwest, dropping over a foot of spring snow from Colorado to Wisconsin. So-called winter Storm Achilles smashed snowfall records across the Upper Midwest. The storm was only the second May snowstorm on record for Kansas City and Des Moines. Today we look at the impact of this year’s late winter weather on energy markets.

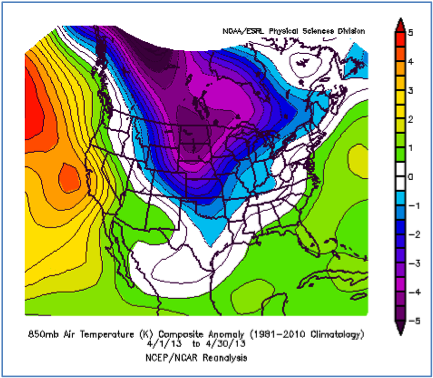

The Achilles storm followed an unusually cold late winter and early spring in 2013. In energy markets, April is usually considered a shoulder month, meaning ‘not much heating demand and not much cooling demand.’ However April 2013 weather was far from dormant. The map below shows average April temperatures compared to normal, (where normal is defined as the mean April temperature from the past 30 years of recorded temperatures). The Central US was much colder (blue and purple) than normal while the Pacific and Atlantic coastal states were warmer than normal (orange and yellow).

Source: NOAA’s Earth Systems Research Lab (Click to Enlarge)

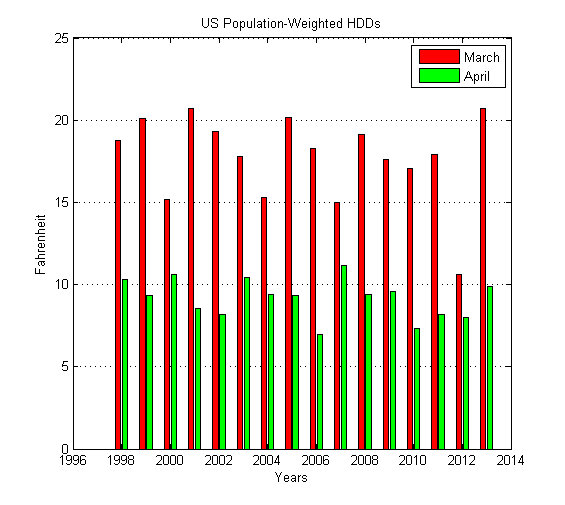

The unusually volatile April weather followed a colder than usual March. The chart below shows March/April average heating degree days (HDDs) for the past fifteen years (see Under the Weather for an explanation of Heating and Cooling Degree Days). The data shows first that March is historically far colder than April. Second, in 2013 we experienced the coldest March in the fifteen-year period. And third, April 2013 was one of the colder Aprils of the past 15 years.

With a record-setting cold March 2013, an unusually cold April 2013 and record-breaking snowfall in May, one has to wonder when this winter might end?

Source: NOAA (Click to Enlarge)

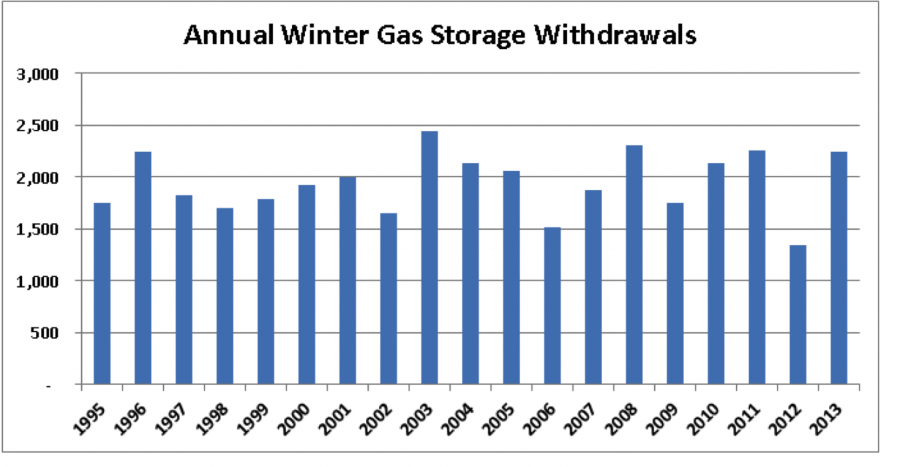

How does unusually cold late winter weather like this impact energy markets? Let’s consider just the natural gas market for the moment. Nationwide local gas distribution companies (LDCs) typically withdraw gas from underground storage during the heating season, nominally defined as November 1st through March 30th (see Put it in Your Cavern). Over the past ten years an average total of 2,010 bcf has been withdrawn from storage during the heating season (see chart below). This winter, in spite of milder weather early on, a cold March and April prompted gas marketers to withdrawal 2,243 bcf from storage. That extra ~250 bcf of gas withdrawn from storage brought an over-supplied gas market back into balance and allowed gas prices to rise above $4.00 / MMBtu by April 2013 – double what they were a year before.

Bcf per Year - Source: EIA (Click to Enlarge)

The chart below shows US natural gas consumption over the past eight years from January to May (source: Bentek). Gas consumption was unusually high during both March and April of 2012 (blue line) and 2013 (green line) but for completely different reasons. This year gas consumption was high because cold weather increased the demand for space heating. Last year record gas consumption resulted from a surge in natural gas fired power generation. That happened after an unusually warm 2011-2012 winter caused the price of natural gas to plummet beneath coal fuel costs. These examples illustrate how abnormal weather - hot or cold – can have a significant impact on energy markets.

Join Backstage Pass to Read Full Article