Boosting America’s hydrocarbon output was a major plank in the 2024 Republican platform, and Donald Trump’s recent victory has stimulated a lot of optimism about the U.S. upstream sector. The nomination of Liberty Energy CEO Chris Wright as Energy Secretary confirmed that “drill, baby, drill” will be a mantra in the new administration. However, over the past few years, U.S. producers have dramatically shifted their focus from growth at any cost to strict financial discipline focused on maximizing free cash flows and shareholder returns. In today’s RBN blog, we analyze the Q3 2024 results of the major U.S. E&Ps we follow and look for early clues about how their senior executives might react to the renewed federal enthusiasm to rapidly accelerate drilling.

The NATGAS Appalachia weekly report provides the data and insights to monitor the northeast natural gas market’s twists and turns and identify the risks and opportunities along the way, including tracking supply-demand trends, outbound capacity and their impact on takeaway pipeline utilization, and regional prices.

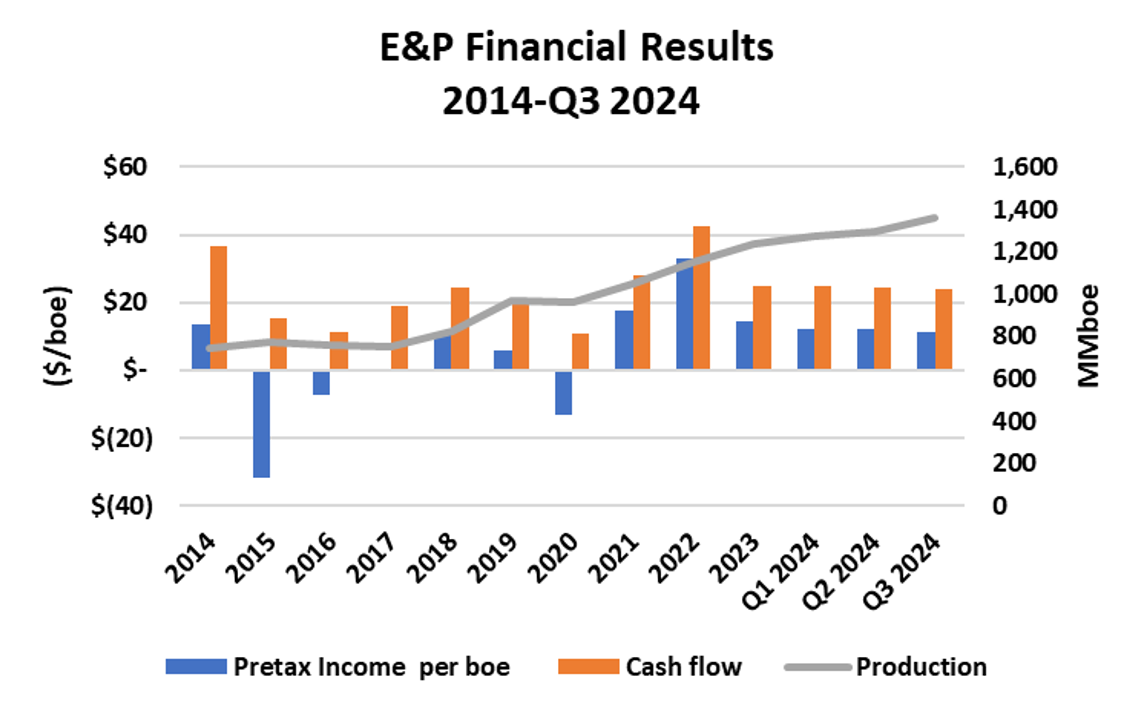

We begin with a reminder that producers were financially brought to their knees in early 2020 after a steep commodity price decline in late 2019 that bottomed out after the onset of the pandemic. Investors fled the oil and gas industry in droves and equity prices fell 95% from their 2014 highs. Survival necessitated the shift in strategy from growth to fiscal discipline, which was implemented by E&P executives heavily incentivized by bonus criteria that tied compensation to rates of return rather than reserve and production growth. Thanks to a surge in post-pandemic commodity prices, cash flows soared and investors flocked back to an industry that suddenly offered total returns nearing or exceeding 10%. Although prices have retreated from 2022 highs, the industry is still generating cash flows of more than $20 per barrel of oil equivalent (boe) produced. As shown by the orange bars and left axis in Figure 1 below, this level is still significantly higher than the results in 2015-20.

Figure 1. E&P Financial Results and Production, 2014-Q3 2024.

Source: Oil & Gas Financial Analytics, LLC

However, Q3 2024 results show that weakening oil prices are eroding profits (blue bars and left axis) and cash flows. The average WTI crude oil price slid nearly 7% in Q3 2024 to $75.26/bbl and exited the quarter at just above $70/bbl. The dip was partially offset by a bump in natural gas prices from summer lows, but the average realized price for the 39 E&Ps we follow fell 5% to $35.82/boe, the lowest since Q2 2023. That translated into a 5% reduction in cash flow at $23.97/boe. Pre-tax operating income fell 17%, heavily impacted by a $1.1 billion impairment charge by APA Corp. The declining results were mirrored by a 4% decline in the S&P E&P index, as investor sentiment has been closely tied to oil prices.

About the song

“Who’ll Stop the Rain” was written by John Fogerty and appears as the third song on side two of Creedence Clearwater Revival’s fifth studio album, Cosmo’s Factory. This song is another example of the swamp rock/Americana music that made them such a popular singles band. Released in January 1970, it went to #2 on the Billboard Hot 100 Singles chart and has been certified Platinum by the Recording Industry Association of America (RIAA). Backed with “Travelin’ Band,” it was one of three double-sided singles from Cosmo’s Factory to reach the Top Five on Billboard's Hot 100 Singles chart. Personnel on the record were: John Fogerty (lead vocals, lead guitar, piano), Tom Fogerty (rhythm guitar, backing vocals), Stu Cook (bass, backing vocals), and Doug Clifford (drums).

Cosmo’s Factory was recorded in 1969-70 at Wally Heider in San Francisco with John Fogerty producing. Released in July 1970, it went to #1 on the Billboard 200 Albums chart and has been certified 4X Platinum by the RIAA. It would be the last album with Tom Fogerty in the band. Three double-sided singles were released from the LP.

Creedence Clearwater Revival (aka CCR or Creedence) was an American rock band formed in 1959 in El Cerrito, CA, by John and Tom Fogerty, Stu Cook and Doug Clifford. They played under the names The Blue Velvets and The Golliwogs before changing their name to Creedence Clearwater Revival in 1967 after signing a record deal with Fantasy Records in San Francisco. As CCR, they released seven studio albums, five live albums, 41 compilation albums and 29 singles and have sold more than 50 million records worldwide. The band broke up in 1972, with John Fogerty pursuing a solo career and the others involved in various projects. Tom Fogerty released several solo albums before passing away at his home in Scottsdale, AZ, following surgery complications in September 1990. The band was inducted into the Rock and Roll Hall of Fame in 1992, where John Fogerty refused to play with the surviving members. Fogerty continues to record and perform and will be doing a series of shows at the Encore Theater at Wynn Las Vegas in January 2025.