Since 2011, U.S. natural gas liquids (NGL) production has more than tripled, while domestic demand has grown only modestly. Consequently, the only way NGL markets could balance was a dramatic increase in exports. Today, over 70% of U.S. propane production is exported, with the majority going to overseas markets, while other NGLs see varying export levels: 40% for butanes, 25% for natural gasoline, and 18% for ethane. Although U.S. NGL production growth is slowing, we still project an increase of 1.5 MMb/d over the next decade and a half, with 85% of that growth coming from the Permian Basin. As U.S. ethane and LPG production continues to rise, nearly all the export growth is expected to head to the Asia/Pacific region, with a significant portion going to one country: China. But is this outlook for U.S. NGLs realistic? And do we have adequate infrastructure — ranging from gathering systems to processing plants and fractionators, and from export terminals to the right kind of ships — to handle all of these volumes? In one of his hit tunes, Toby Keith clearly identified the problem for us: “Where You Gonna Go? And What Ya Gonna Do When You Get There?” These are key NGL market themes that we'll be exploring at our upcoming NACON conference on October 24 at the Royal Sonesta Hotel in Houston and that we’ll introduce in today’s RBN blog.

Let’s start with our view that NGL production will continue to grow, but at a rate slower than in the past few years. That’s not much of a surprise, considering the rapid increase of NGL production from gas processing, up from about 2.2 MMb/d in 2011 to 6.7 MMb/d in 2024. During that 13-year period, production of propane, butanes and natural gasoline (C3+) increased from 1.3 MMb/d to 4 MMb/d (about 3X), while recovered ethane production tripled from 0.9 MMb/d to 2.7 MMb/d.

Most NGL production in the U.S. is dominated by shale-driven, “supply-push” economics. Volumes are essentially a byproduct of crude oil and natural gas production, with NGL supply growth dependent on the growth trajectory of “wet” (high-Btu) natural gas, much of it associated gas from crude wells. Accordingly, we project NGL supply primarily as a function of crude and natural gas production growth, with our “Mid” forecast scenario based on $70/bbl WTI Cushing crude and $4/MMBtu Henry Hub gas. At these prices, and with today’s production economics and producer capital deployment strategies, oil and gas production growth is slowing and will eventually flatten, then shift into a declining trajectory.

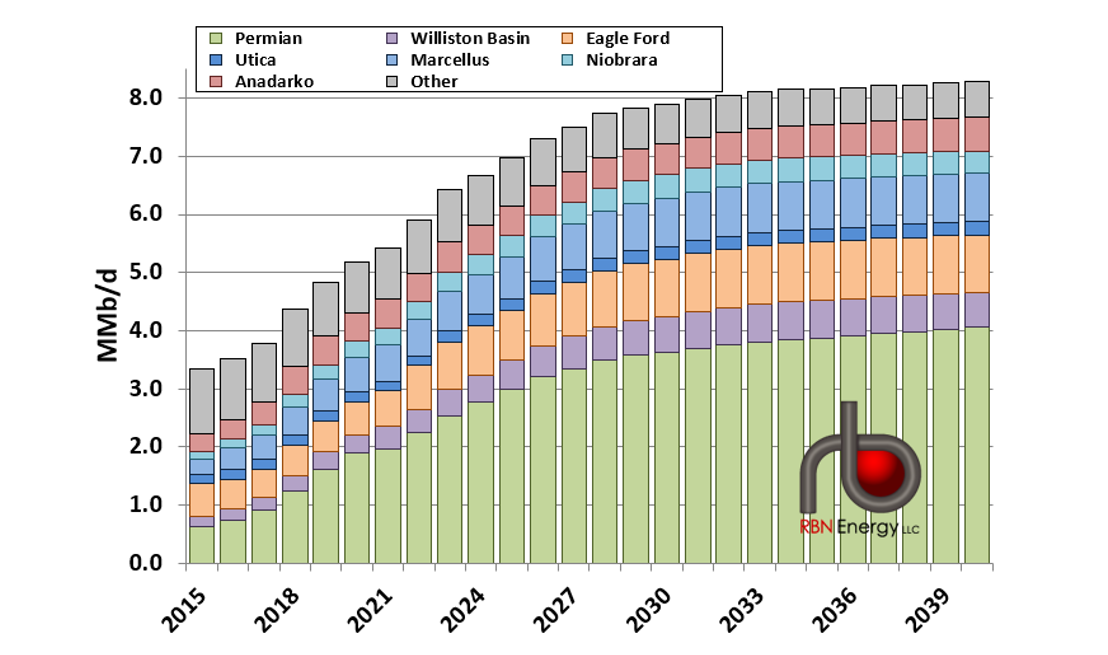

But even with that slower-growth outlook, as shown in Figure 1 below, NGL production is still expected to increase from 6.7 MMb/d in 2024 to 8.2 MMb/d in 2040 (CAGR 1.3%), up 1.5 MMb/d, with — as noted above — 85% of the incremental volume coming from the Permian (green bar segments). Note that the increase is front-end loaded, with most of the growth in the 2025-30 timeframe. Even though we project crude oil production to peak in the early 2030s, increasing gas-to-oil ratios (GORs) and higher NGL content (gallons per Mcf, or GPM) keep NGL production growing through the 2040 horizon.

Figure 1. NGL Production Forecast by Basin. Source: RBN