Last Thursday (May 16, 2013) the Ohio Department of Natural Resources offered a rare glimpse into 2012 production in the Utica shale. In a long awaited report, the State said that 87 wells drilled by 11 companies produced about 1750 b/d of oil and 35 MMcf/d of gas. Those numbers disappointed investors hoping for evidence of another Bakken or Eagle Ford. But the State data does not tell the whole story. There should be a surge in production now that infrastructure is coming online. And significant condensate production will present new challenges for midstreamers. Today we take a closer look at Utica production.

Excitement about potential increased oil production in the Utica shale in Ohio this year was tempered by a 7-week delay in the Ohio Department of Natural Resources (ODNR) releasing its 2012 production data. The numbers were supposed to be available during the first week of April (2013) but showed up in the 3rd week of May. When finally published the ODNR data dashed expectations by reporting that oil production from 87 wells was only 1750 b/d and natural gas production was 35 MMcf/d. The data suggests first that oil production is far lower than expectations of production based on early results from more prolific shale plays such as the Bakken and Eagle Ford. Second the data indicates that the Utica will produce more gas than oil. In various reports, industry commentators indicated disappointment in the data because the Utica had been touted as one of the next big oil plays.

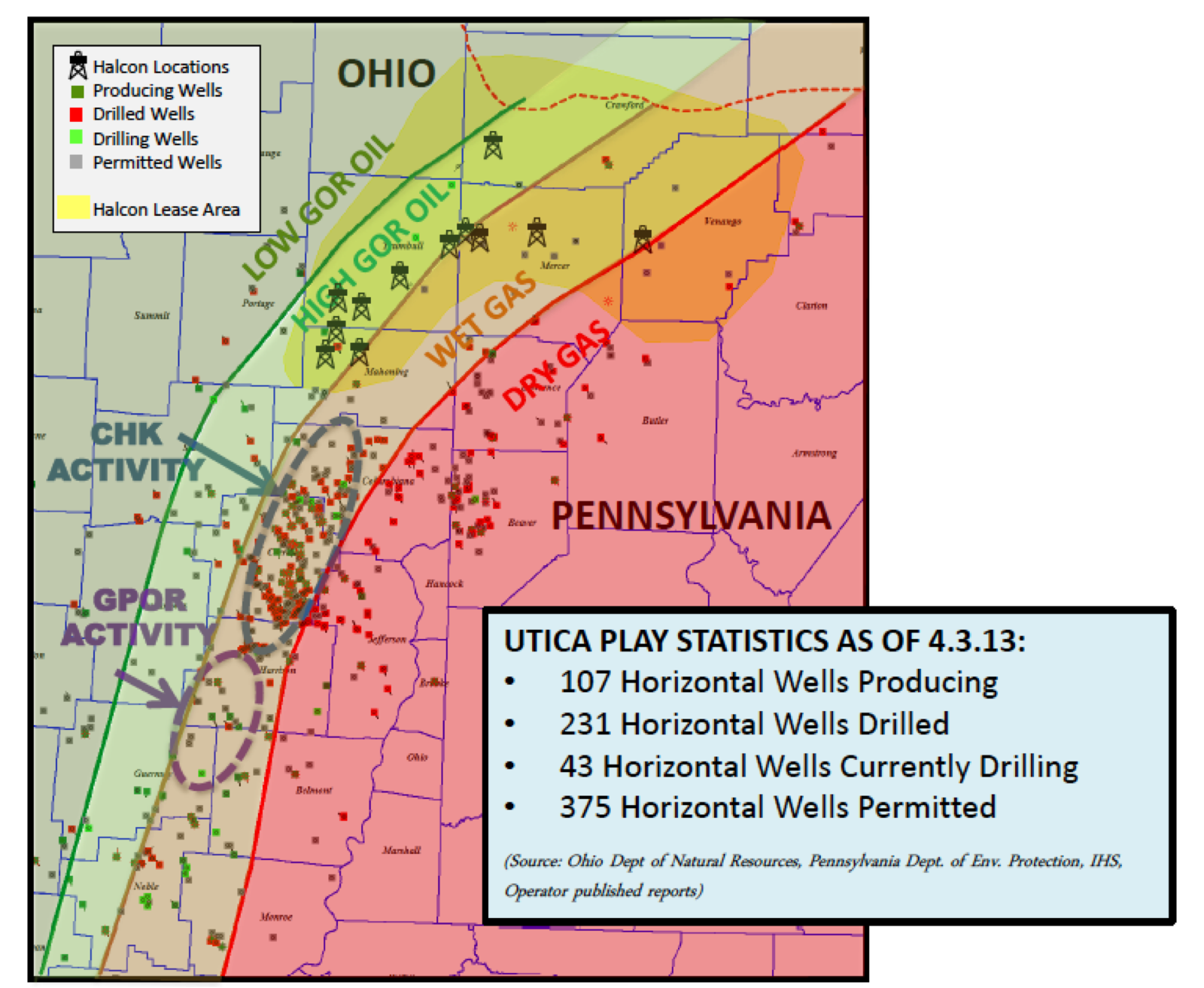

Actually the news is not all bad and we need to look deeper to understand the results and the real opportunities in this play. Part of the reason that the ODNR results are misleading stems from the fact that 2012 drilling in the Point Pleasant shale formation in Northeast Ohio – the sweet spot for producers - was targeted in that part of the shale that produces primarily wet gas and not oil. Although initially attracted to the oil window to the west of the formation, producers found less success there because oil accumulations are located in a geological structure that lacks pressure to force the hydrocarbons out of the shale. That makes extraction more complicated. So instead of chasing oil Utica producers targeted the wet gas area of the shale in search of gas liquids (see map below). But when the analysts see data that indicates higher natural gas production they conclude that the Utica is a gas play rather than an oil play and expectations are reduced. That is because low natural gas prices relative to oil mean that “gas” plays don’t generate the same excitement in the financial community as oil plays. However it seems likely that the wet gas area of the Utica will produce large volumes of natural gas liquids and condensate. While these liquids may not be quite as valuable as oil they do provide considerable uplift over and above the price of natural gas.

Source: Halcon Resources Presentation

For example, in advance of the ODNR data announcement last week several independent producers published optimistic Utica Point Pleasant drilling results for the first quarter of 2013. The third largest Utica producer, Gulfport Energy said that their first fourteen wells averaged an initial production rate of 807 b/d of condensate, 7.8 MMcf/d of natural gas and 946 b/d of NGLs. The production mix was 36 percent condensate, 36 percent natural gas, and 28 percent natural gas liquids – that is 64 percent liquids, and that is very good news for well economics.

Another misunderstanding about the ODNR data is that many more wells have been drilled than are actually in production. To date, Ohio has approved permits for 660 shale wells of which 326 have been drilled and only 97 are now in production. That is because producers are holding off bringing wells into production until pipelines, natural gas processing plants and other infrastructure is complete. The largest Utica player, Chesapeake, reported only moderate Utica Shale production growth last year because they were sitting on wells and waiting for infrastructure. At the end of the third quarter 2012, nearly 40 Chesapeake operated Utica Shale wells had been drilled but were not yet producing. Since these wells are not producing they do not show up in the ODNR production data and the lack of “actual” production weighs heavy on analysts used to hearing about dramatic increases in production every month in North Dakota. In this environment, no news is viewed as bad news.

So despite the disappointing pronouncements from the ODNR about 2012 we should actually expect a surge in gas and liquids production from the Utica this year because, as we discussed last week (see The Big Surge Comes to Whoville) significant takeaway and processing capacity is coming online in the Appalachian Marcellus and Utica shale regions over the next six months. That new infrastructure will allow producers to unleash their inventory of completed wells into production.

And the downside, if there is one, to that production surge is that – as suggested by Gulfport’s early results – it will not just include natural gas and NGLs but also significant volumes of condensate. Not that condensates are a bad thing – its just that their value seems to be generally misunderstood -- by producers, refiners and especially by analysts. . Condensates seem to be like problem children. As we have discussed many times in RBN blogs, condensates are variously lumped in with crude production from oil wells and with NGL production from gas wells (see Fifty Shades of Condensate Which One Did You Mean?). The reality is that in shale basins where the liquids output from gas wells is as high as it appears to be in the Utica, condensate has to be recognized for what it is and handled as a product its own right. Unfortunately that means the infrastructure challenge in the Utica is not just one of building pipelines and plants to process natural gas and NGLs. A whole other set of infrastructure is also needed to process and market the large volumes of lease condensate being produced from wet gas wells.

So Utica producers in the wet gas window of the play now find themselves having to install condensate-processing equipment at the wellhead in the form of stabilizers. That is because so much of the Utica liquids production consists of very light condensate that has an unusually high Reid vapor pressure (RVP - an indicator of the level of volatile compounds in hydrocarbon liquid - see Regulatory Gas Pressure Party for a fuller explanation). That RVP level has to be reduced to meet pipeline specifications before the condensate can be shipped to market. Condensate stabilizers installed at each well pad site reduce the RVP of condensate to permit safe transport. These condensate stabilizers can be pretty complicated pieces of equipment. The picture below shows a 2Mb/d stabilizer manufactured by Exterran, Inc, that includes a distillation tower and separation system that some might call a condensate splitter. [A condensate splitter extracts refined products such as naphtha, kerosene and distillate from raw condensate - Exterran can sell you one of those as well].