Gulf Coast diesel crack spreads (the margin between diesel prices and Light Louisiana Sweet crude - LLS) are averaging just under $16/Bbl this year – about 75 cnts/Bbl lower than 2012 but still pretty healthy. Gulf Coast diesel exports increased by 25 percent in 2012 – mostly to meet increased demand in Latin America. By December Gulf Coast refineries were running at 95 percent capacity to meet export demand. Yet during the first 2 months of 2013 refinery utilization plummeted to 80 percent, diesel production fell and Gulf Coast diesel exports dived by 300 Mb/d. Today we describe the impact that a heavier than usual Gulf Coast refinery repair season had on product exports.

We previously described how Gulf Coast refineries ramp up production and exports of diesel to take advantage of healthy diesel “crack” margins (see Gulf Coast Diesel Crack Habit). The diesel crack refers to the price spread or “crack” between Gulf Coast diesel and LLS crude. The gasoline crack is the equivalent spread between Gulf Coast gasoline and LLS Crude. As always we caution readers that crack spread analysis runs the risk of over simplifying the complex economics that dictate refinery profitability. However, as a rule of thumb, these crack spreads (or just “cracks” if you want to sound credible) tell us whether it is profitable for refiners to make distillate or gasoline.

Before we start - a quick note on the data used in our analysis. We will mostly be referring to data from the Energy Information Administration (EIA) for Gulf Coast diesel and gasoline. When we use the term “Gulf Coast” we are referring to the same geographic region that the EIA guys call Petroleum Administration Defense District Three (PADD 3). We also refer to “diesel” produced by Gulf Coast refiners. Diesel is part of a pool of refined products with similar qualities that are more properly called distillates. We will use EIA export and production data that groups together all distillates in PADD 3 and refer to it as diesel. The main differences between distillate products produced by Gulf Coast refiners are in the sulfur content. US refiners now mostly produce ultra low sulfur diesel (ULSD) to meet new 15 parts per million (ppm) sulfur specifications mandated by the Environmental Protection Agency (EPA) since 2010. The sulfur specifications required by countries that the US exports diesel to can be lower or higher than for ULSD. When we analyze diesel cracks we use ULSD prices for diesel.

Good Times

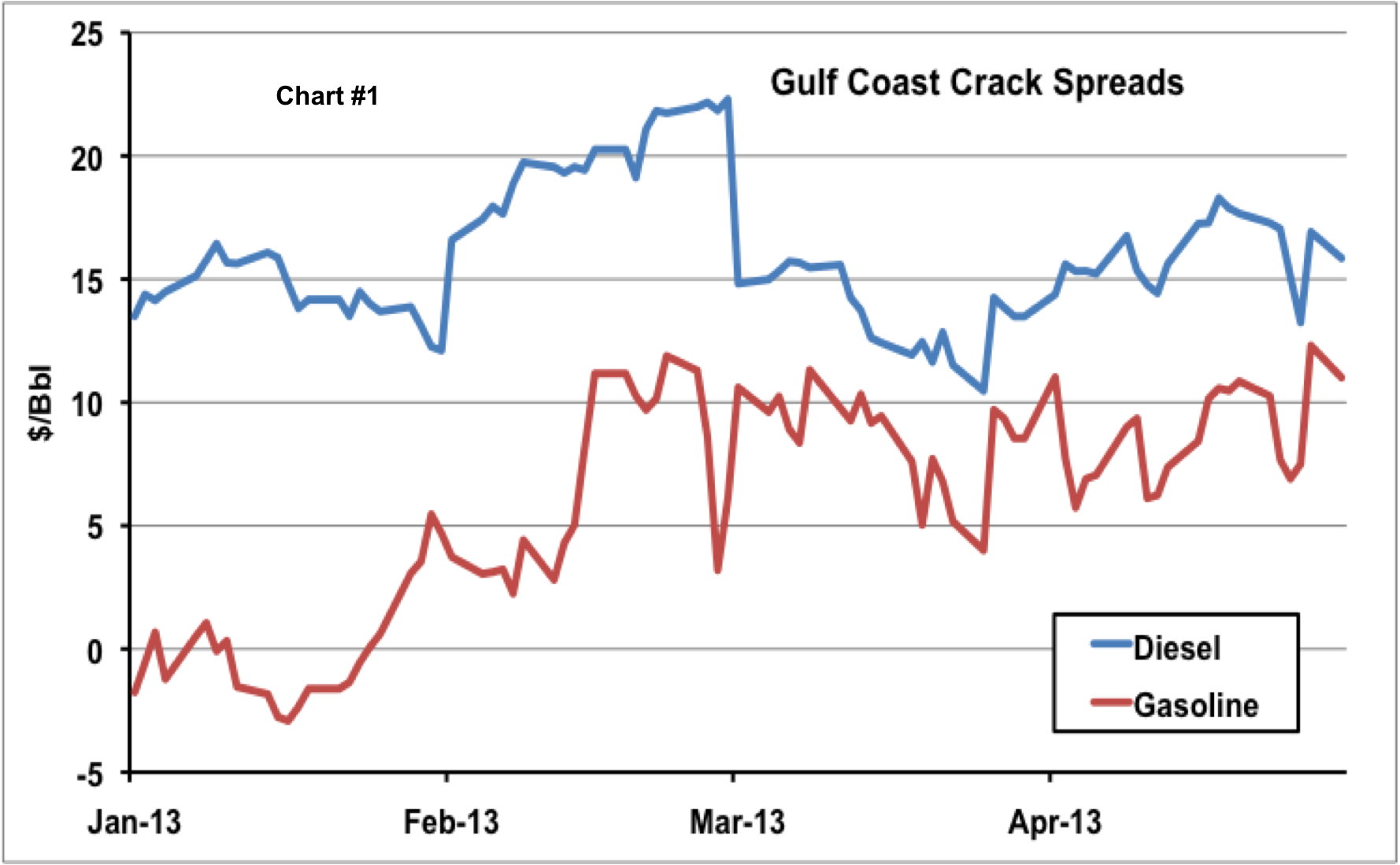

Last year the Gulf Coast diesel crack averaged about $16.75/Bbl – making it a big money earner for regional refineries (see Gulf Coast Diesel Crack Habit). The Gulf Coast gasoline crack averaged $9/Bbl in 2012. Last year exports of diesel from the Gulf Coast increased by 25 percent and gasoline exports increased by 45 percent. US exports of gasoline and diesel have increased significantly in the past few years as demand increased in Latin America where growing consumption has outpaced local refinery capacity. Chart#1 below shows Gulf Coast Gasoline and Diesel cracks since the start of this year (2013). So far this year the Gulf Coast diesel crack has averaged just under $16/Bbl and the gasoline crack has averaged $5.80/Bbl after starting the year in negative territory.

Source: EIA data from Morningstar

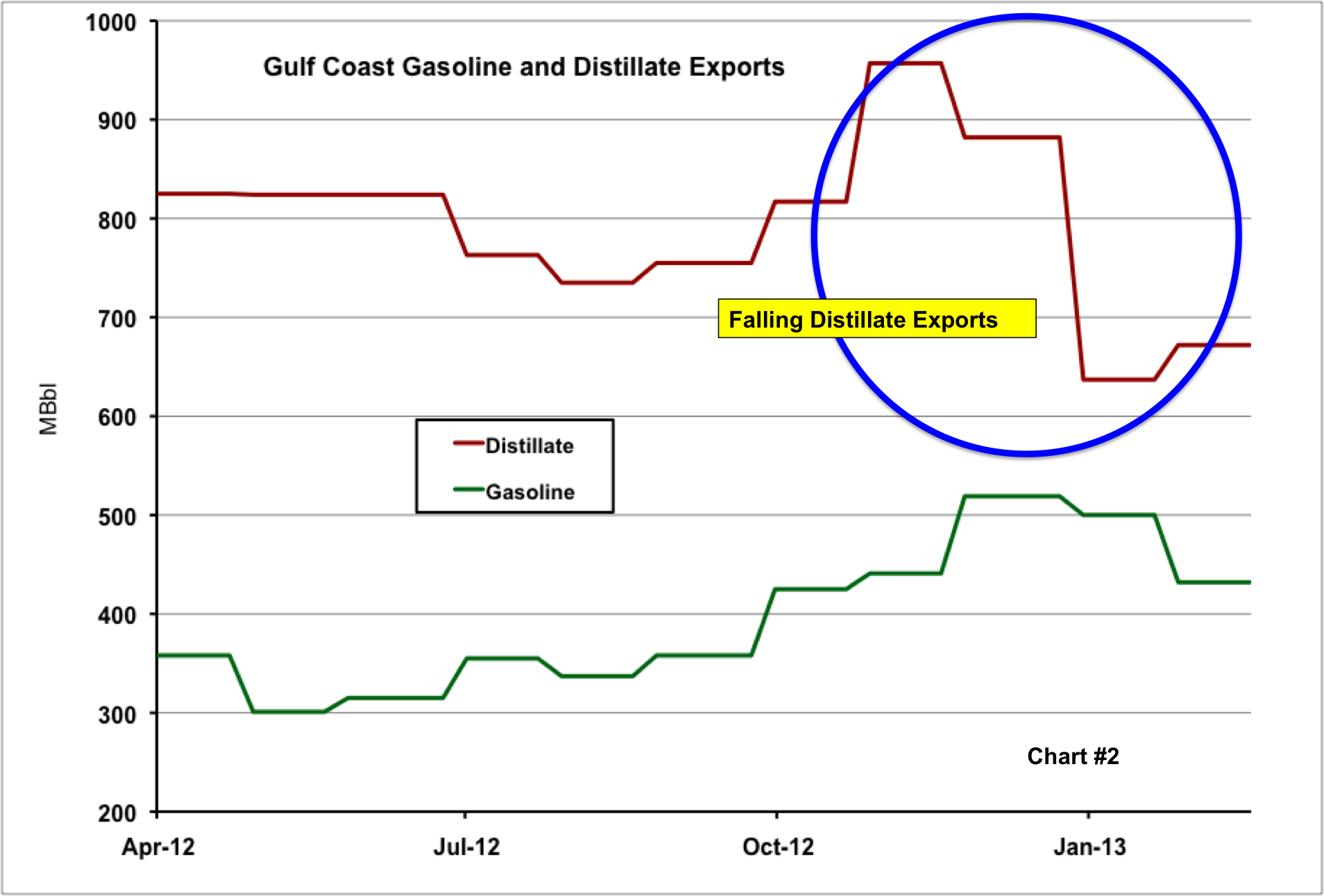

You would expect that continued healthy crack spreads and a buoyant export market would ensure that Gulf Coast refiners would keep pumping out gasoline and diesel at the same rate in 2013 that they did in 2012. Instead diesel and gasoline exports from the Gulf Coast fell by 25 and 14 percent respectively between December 2012 and February 2013 according to EIA data (see Chart #2 below). The main cause of the sudden drop in Gulf Coast exports appears to have been a dramatic reduction in output from Gulf Coast refineries caused by something called refinery turnarounds.

Source: EIA data from Morningstar

Refinery turnarounds are defined by the American Petroleum Institute (API) as:

“a planned, periodic shut down (total or partial) of a refinery process unit or plant to perform maintenance, overhaul and repair operations and to inspect, test and replace process materials and equipment.”

As we have explained previously, refineries are extremely complicated and capital intense processing plants (see Complex Refining 101). They typically run 24 * 7 at high utilization rates. In general, the less often refinery units are started up or taken down the better they run since operational problems are more likely to develop at these times. Turnarounds allow for necessary maintenance and upkeep of operating units and are needed to maintain safe and efficient operations. Bringing down major units such as the crude distillation unit or catalytic cracker results in significantly reduced crude throughput.

Turnarounds are generally planed well in advance to enable the work to be carried out as quickly and safely as possible with all the necessary equipment and manpower in place. Refiners tend to carry out turnarounds during periods of lower refined product consumption, which usually means wintertime in the US. During the winter demand for gasoline is typically lower because fewer people are making long auto journeys. Demand for diesel used as heating oil is higher during the winter in the Northeast but much of that demand is fed from inventory built up during the summer so reduced diesel production during the first quarter does not have such a big impact. Unfortunately since refineries need to perform maintenance regularly – typically at least every four years on major units, the number of refineries in turnaround during any one winter season can add up to a significant reduction in capacity.

About the song

“Total Eclipse of the Heart” was written by Jim Steinman and appears as the fourth song on Bonnie Tyler’s fifth studio album, Faster Than the Speed of Night. Songwriter Steinman (who also produced the album) was famous for writing all of the songs on Meat Loaf’s 1977 debut hit album, Bat Out of Hell. He is known for writing songs that are epic tales, usually involving unique twists in the narrative, and reflective of Steinman's fascination for Phil Spector’s “wall of sound” production techniques. The song was reduced from its seven-minute album length to four minutes and 30 seconds for the single version. Released as a single in the U.S. in June 1983, it went to #6 on the Billboard Hot 100 Singles chart and has been certified Platinum by the Recording Industry Association of America (RIAA). Personnel on the record were: Bonnie Tyler (lead vocals), Larry Fast, Steve Margoshes (synthesizers), Roy Bittan (piano), Rick Derringer (guitar), Steve Buslowe (bass), Max Weinburg (drums), Jimmy Maelen (percussion), and Rory Dodd, Eric Troyer, Holly Sherwood (backing vocals).

Faster Than the Speed of Night was recorded in 1982 at The Power Station and Right Track Studios in New York City with Jim Steinman and John Jansen producing. The album includes five radically re-worked cover songs by John Fogerty, Blue Oyster Cult, Bryan Adams, Frankie Miller, and Lee Kasmin. The album was released in September 1983 and went to #4 on the Billboard 200 Albums chart. It has been certified Platinum by the RIAA. Eight singles were released from the LP.

Bonnie Tyler (Gaynor Sullivan) is a Welsh singer known for her gruff whiskey voice. She has been compared to Rod Stewart in her vocal timbre. In 1975, she was discovered singing in a club in the Welsh city of Swansea by talent scout Roger Bell, who was able to secure her a deal with RCA Records. Her first big hit in the U.S. was “It’s a Heartache,” which went to #3 on the Billboard Hot 100 Singles chart in 1978. She has released 18 studio albums, two live albums, 64 compilation albums, four EPs, and 83 singles. She was appointed Member of the Order of the British Empire (MBE) in 2022. Her memoir, Straight from the Heart, was released in September 2023. She continues to record and started a European tour in early October.