Refined product supply in Petroleum Administration for Defense District (PADD) 1, which comprises Atlantic Coast states from New England to Florida, has been in trouble all year. Maintenance issues beset refineries during the first quarter, and then in June, the region's largest refinery, a 355-Mb/d plant owned by Philadelphia Energy Solutions (PES), was shuttered after a fire. The loss of the PES output would've been manageable if imports had taken up the slack. But although gasoline imports increased, distillate shipments have actually been lower than normal since June. As a result, the PADD 1 distillate market has been drawing an average 163 Mb/d from inventory since mid-August, according to weekly Energy Information Administration (EIA) reports, leaving stocks in the region at a 10-year low. That storage deficit versus previous years will increase when the weather turns colder and heating oil demand kicks into high gear. With stocks at historical lows and market prices not attracting new supplies, the shortage may well foreshadow price spikes this winter. A potential strike by unionized workers at the Phillips 66 Bayway refinery in northern New Jersey could make matters worse. Today, we look at what's behind the PADD 1 distillate shortfall.

This blog is based on research from Morningstar Commodities and Energy. Click here for a copy.

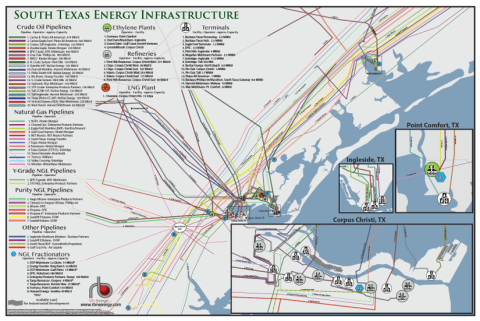

RBN Energy’s South Texas Energy Infrastructure Map brings together all the pieces of the critical and complex puzzle of the greater Corpus Christi region. Spanning from Point Comfort, TX to Corpus Christ, TX and south of the Agua Dulce natural gas hub, the map details the processing, transportation and export facilities in RBN Energy’s classic clear, concise and easy to comprehend style.

The ebbs and flows of crude feedstocks and refined products for East Coast demand centers is a running topic in the RBN blogosphere; it seems that just as a trendline appears in the region, something disruptive changes the dynamics. We've tracked the plight of refiners in PADD 1 in recent years, including a comprehensive outlook in Back to Red on refining in the region in October 2016. In June, we described in Another One Bites the Dust how the PES closure would mostly affect the Mid-Atlantic refining district fed by Philadelphia refineries. At that time, it looked as though an increase in refined product imports would resolve any product shortage issues in the short term, with the potential partial reversal of Buckeye Partners’ Laurel Pipeline offering prospects for increased product shipments from the Midwest to help make up for the loss of PES output in the longer term.

We begin today’s analysis with a recap of the big picture for PADD 1 refined product supply, specifically of gasoline and distillate. Distillate includes diesel used for road transport and heating oil used primarily for home heating. PADD 1 is net short of refined products because the region’s refining capacity, which totaled 1.2 MMb/d before the PES closure, only produced about 800 Mb/d of gasoline and distillate, according to 2018 annual average data from the EIA. That volume met just 20% of the regional demand for 2.9 MMb/d of gasoline and 1.3 MMb/d of distillate in 2018. The shortfall was primarily met with supplies shipped into PADD 1 by pipeline, barge and tanker from the Gulf Coast PADD 3 region, including an average 1.8 MMb/d of gasoline and 800 Mb/d of distillate in 2018 — the majority of that moving on the 2.7-MMb/d Colonial Pipeline system that runs up the East Coast from Houston to Linden, NJ. The balance of PADD 1 demand last year was met by imports, which averaged 600 Mb/d of gasoline and 150 Mb/d of distillate during 2018. The difference this year is that refinery crude throughput averaged only 989 Mb/d between January and June, and just 834 Mb/d since the PES fire, leaving the region increasingly reliant on outside supplies.

About the song

“Tighten Up” was written by Archie Bell and Billy Butler, and was originally released as a single by Archie Bell and the Drells on the Houston independent label Ovide Records in October 1967. The origins of the song start with popular KCOH-AM Houston deejay and business entrepreneur Skipper Lee Frazer hearing a two-chord funk instrumental song being played in live shows and filling the dance floor by the TSU Tornadoes. He suggested Archie Bell add some vocalizations to the tune, and Bell, with the Drells and the Tornadoes, cut the song at Jones Town Studios in Houston. Produced by LJF Productions (Skipper Lee Frazer), the Ovide Records (Frazer’s label) version quickly became a hit in the Houston market, attracting the attention of Atlantic Records, which picked it up and released it on its label in April 1968. The record then went to #1 on the Billboard Hot 100 and Hot Rhythm and Blues charts. It has been certified Gold by the Recording Industry Association of America. Personnel on the record were: the TSU Tornadoes, featuring Cal Thomas (guitar), Will Thomas (guitar), Jerry Jenkins (bass), Robert Sanders (organ), Dwight Burns (drums), Darryl Bursby (sax) and Clarence Harper (trumpet). The Drells featured: Archie Bell, James Wise, Willie Parnell and Billy Butler.

Due to the success of the single, Atlantic quickly released an album made up of songs from the Drells and Tornadoes’ Houston sessions. The Tighten Up album went to #15 on the Billboard Hot Rhythm and Blues Albums chart and #142 on the Billboard Top 200 Albums chart. Ironically, Archie Bell was serving in Vietnam as his records were on the charts. In 1968, due to an injury, Bell was reunited with his group, and the band recorded a new album with Gamble and Huff’s Philadelphia International label, which produced their second hit single, “I Can’t Stop Dancing,” which went to #9 on the Billboard Hot 100 chart.

Archie Bell and the Drells were a rhythm and blues vocal group that formed in Houston in 1966. They were active from 1966 to 1980. The group released eight studio albums and 24 singles. Archie Bell has released one solo album and three singles.