West Texas Intermediate (WTI) crude prices reached $110.53/Bbl last Friday, their highest daily settlement since May 2011 - in response to expectations of a US military attack on Syria. The sudden prospect of a Russian brokered peaceful solution to the Syrian chemical weapons crisis prompted a $3/Bbl fall in WTI prices since then. These wild price gyrations in response to events far away continue to impact US crude markets so long as we are major importers. Today we look at how the Syria crisis affects the US oil market.

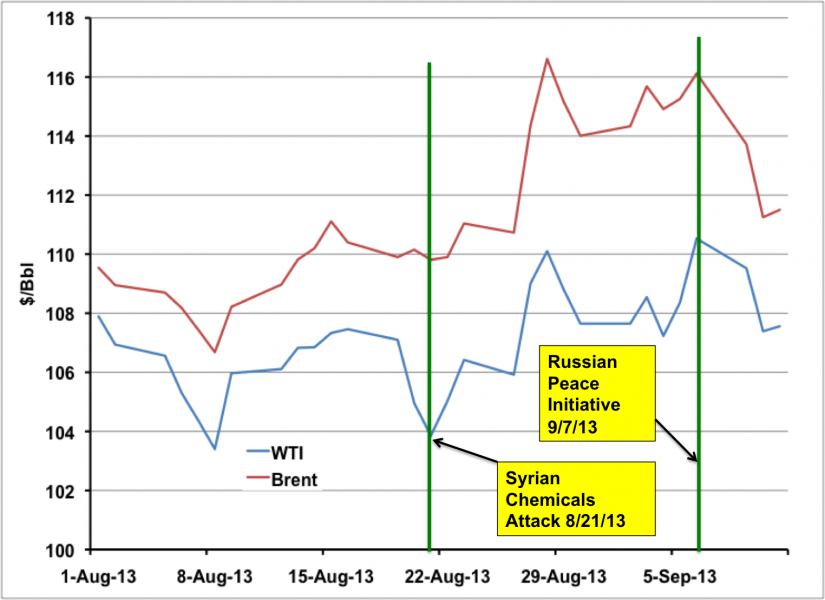

Since the 1970’s Middle East crises has always proven to be a reliable tinderbox for crude oil prices and last week was no exception. With no apparent change in the fundamental crude supply position the war headlines caused a jolt in the arm to prices worldwide. The chart below shows WTI and Brent crude prices over the past month. Between the dates the Syrian chemical weapons attack started the crisis on August 21 and the first signs of a peaceful resolution this Monday (green lines on the chart) prices increased markedly. The “crisis” premium was higher in the US as WTI increased $6.68/Bbl, while the European North Sea crude benchmark Brent jumped $6.30/Bbl over the same period.

Source: CME data from Morningstar (Click to Enlarge)

These crisis premiums end up being an unexpected bonus to US crude producers who get a higher price for their oil even though they are nowhere near Syria. Of course these payouts don’t always last long – a few days in this case (until the next time) but they remind us that even as the US crude shale revolution increases production, the market here is still subject to influences outside our borders. And that is because international markets largely set crude prices here in the US since we are still a significant importer of crude oil. Yesterday’s EIA weekly data showed the US still importing 8 MMb/d of crude oil – more than half its requirements. That means incremental barrels purchased at coastal locations continue to set the prices US refiners pay for crude oil.

The US domestic crude oil market is not always aligned with international prices of course. For a period of three years ending this past July, inland crude prices set using WTI as a benchmark, were heavily discounted to international Brent prices. That disconnect was caused by US crude supplies from new production getting land locked in the Midwest (see Strangers in the Night). The crude logjam in the Midwest prevented US supplies reaching coastal refineries and the latter paid as much as $30/Bbl more than their inland counterparts for crude priced at international levels. Refiners in the Midwest paid a lot less for their crude because of the supply glut that pushed down the value of landlocked supplies.

Now, however, US domestic and international crude prices are trading in a narrower range. As a result international events such as those unfolding in Syria have a more immediate impact throughout the US market. And while producers might be benefited by higher “war premium” crude prices, US refiners are not happy at all. Refiners tend to take it on the chin when crude prices move up rapidly. That is because refined product markets generally take longer to respond to increases in crude prices as supplies work their way through the distribution system. That means refiners pay more for raw materials (crude) and get less for their finished goods (refined products) meaning lower refining margins. Of course that delay in refined product markets when crude prices change is a two-way phenomena because when crude prices fall, refined products inevitably take longer to respond – allowing refiners to take advantage. But this year it has been a one-way ticket for US refiners as their crude costs have increased and product prices have hardly responded.

Join Backstage Pass to Read Full Article