Fast-rising NGL supplies during the early years of the Shale Era fueled excitement about the potential for new petrochemical plants in the U.S., especially ethane-only crackers to make ethylene and other byproducts, along with propane dehydrogenation (PDH) plants to make propylene. While 11 new ethane-fed crackers have come online in the U.S. since the mid-2010s and the world’s largest — Chevron Phillips Chemical and QatarEnergy’s 4.8-billion-lb/year facility — is under construction in Texas, only three of the many PDH projects proposed over the same period were actually built. In today’s RBN blog, we’ll look at why the initial rush of new PDH project announcements resulted in so few new U.S. plants.

Visualize the infrastructure behind U.S. NGL movement.

The U.S. NGLs Map provides a comprehensive view of the transport, processing, and export networks moving NGLs across the U.S.

The Shale Revolution changed a lot of energy fortunes in the U.S. Pre-shale, the U.S. had become heavily dependent on foreign crude oil and was planning to import LNG to help meet natural gas demand, but with shale, the U.S. is now the world’s largest producer of oil, gas and NGLs and a significant exporter of all three. Plentiful domestic supplies of NGLs and purity products like ethane, propane, butanes and natural gasoline also helped revive the petrochemical industry and turn the U.S. into a global supplier of both petchem feedstocks and plastic resins.

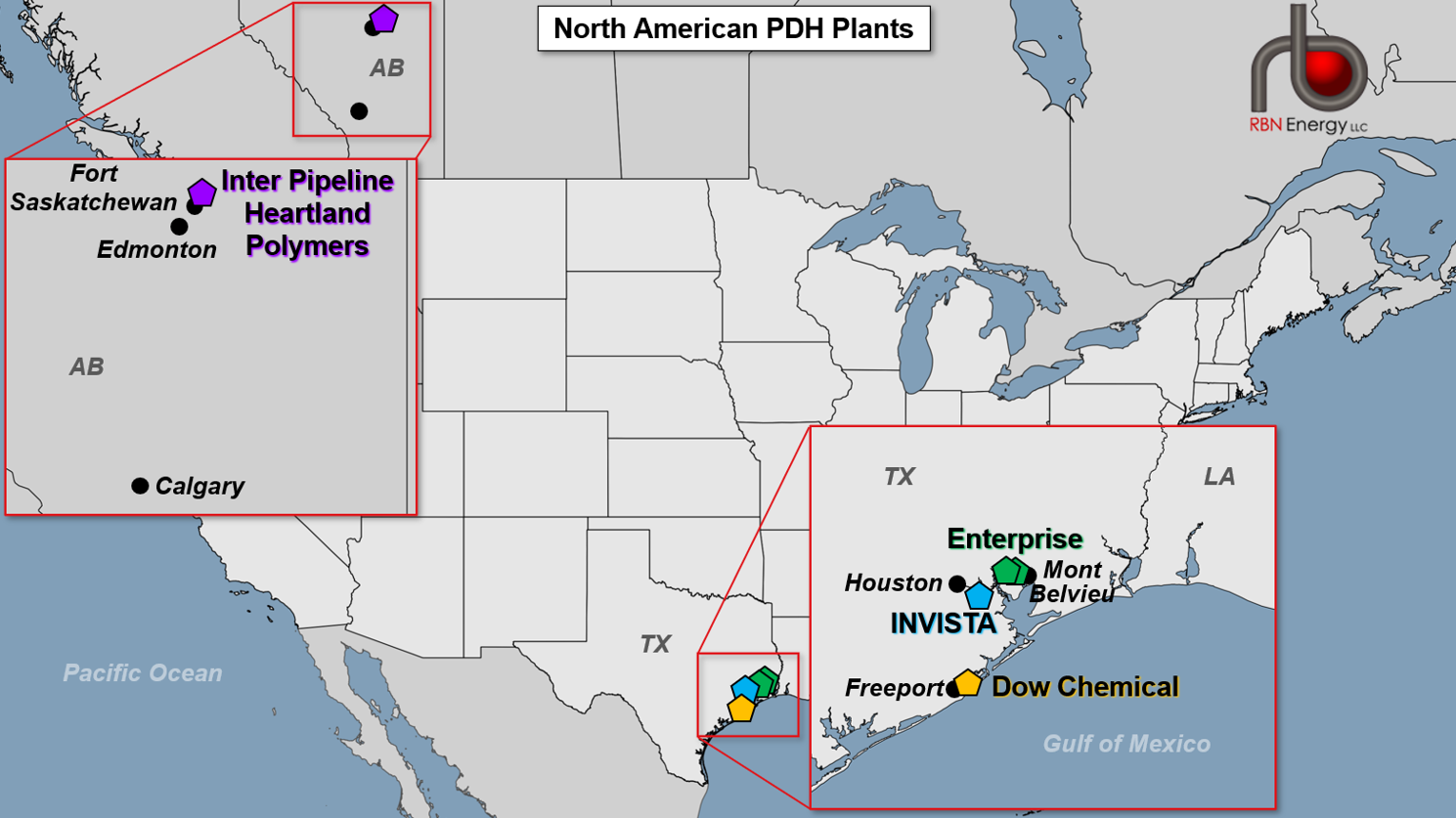

Figure 1. North American PDH Units. Source: RBN

Before 2015, the U.S. had a slew of mixed-feed crackers that were built to “crack” different feedstocks such as ethane, propane, butane, naphtha and gas oil to produce ethylene, propylene and other byproducts — the building blocks of too many chemicals to count. INVISTA’s Houston-area facility (blue pentagon in Figure 1 above) — built by PetroLogistics LP in 2010 and later sold to Koch Industries — was the only PDH unit in North America at the time as propylene demand was largely met with enough “byproduct” production — propylene output from mixed-feed crackers or refineries. There are now five PDH units operating in North America (more on those later).

About the song

“Stop Draggin’ My Heart Around” was written by Tom Petty and Mike Campbell. It appears as the third song on side one of Stevie Nicks’ debut solo studio album, Bella Donna. The song was originally recorded to be included on Tom Petty and the Heartbreakers’ Hard Promises album. When producer Jimmy Iovine, who was working on Stevie Nicks’ album, heard the song, he told Petty that he thought it would be a good duet for them, and the idea expanded from there. Released as a single in July 1981, it went to #3 on the Billboard Hot 100 Singles chart. Personnel on the record were: Stevie Nicks (lead vocals), Tom Petty (co-lead vocals, rhythm guitar), Mike Campbell (lead guitar), Benmont Tench (organ), Stan Lynch (drums), Duck Dunn (bass), Phil Jones (percussion), and Lori Perry, Sharon Celani (backing vocals).

Bella Donna was recorded from the fall of 1980 to the spring of 1981 and produced by Jimmy Iovine and Tom Petty. In addition to using Tom Petty and the Heartbreakers, Nicks brought in Don Henley, Waddy Wachtel, Roy Bittan and Duck Dunn to assist in doing the album. Released in July 1981, it went to #1 on the Billboard 200 Albums chart and has been certified 4x Platinum by the Recording Industry Association of America. Four singles were released from the LP.

Stevie Nicks is an American singer-songwriter known for her work in Fleetwood Mac and as a solo artist. She started her professional career as half of the duo Buckingham Nicks with then-boyfriend Lindsey Buckingham. The pair joined Fleetwood Mac in 1975 and helped propel the group to becoming one of the most successful acts of all time, with record sales of over 120 million worldwide. As a solo artist, Nicks has released eight studio albums, three live albums, five compilation albums, and 36 singles. She has won one Grammy Award and a Grammy Hall of Fame Award. As a member of Fleetwood Mac, she was inducted into the Rock and Roll Hall of Fame in 1998. The group also has a star on the Hollywood Walk of Fame. She continues to record and perform and is currently on tour, moving to Europe in July.