Does lightning strike twice? How about three times? Sure seems like the coal industry has been hit by three lightning bolts in the past several years: a recession that reduced demand for electrical power, low prices for competing fuels (i.e., natural gas), and new federal regulations on smokestack emissions. Today we review regulations that have left coal power generators singing the smokestack blues.

Abiding by the federal laws that regulate coal-burning power plant emissions can cost power producers a lot of money. The high cost of complying with these regulations encouraged the retirement of 9 gigawatts (GW) of coal-burning power plant capacity in 2012 – about 3 percent of total US coal plant capacity of 316 GW. As we shall see more retirements are on the way in the coming years.

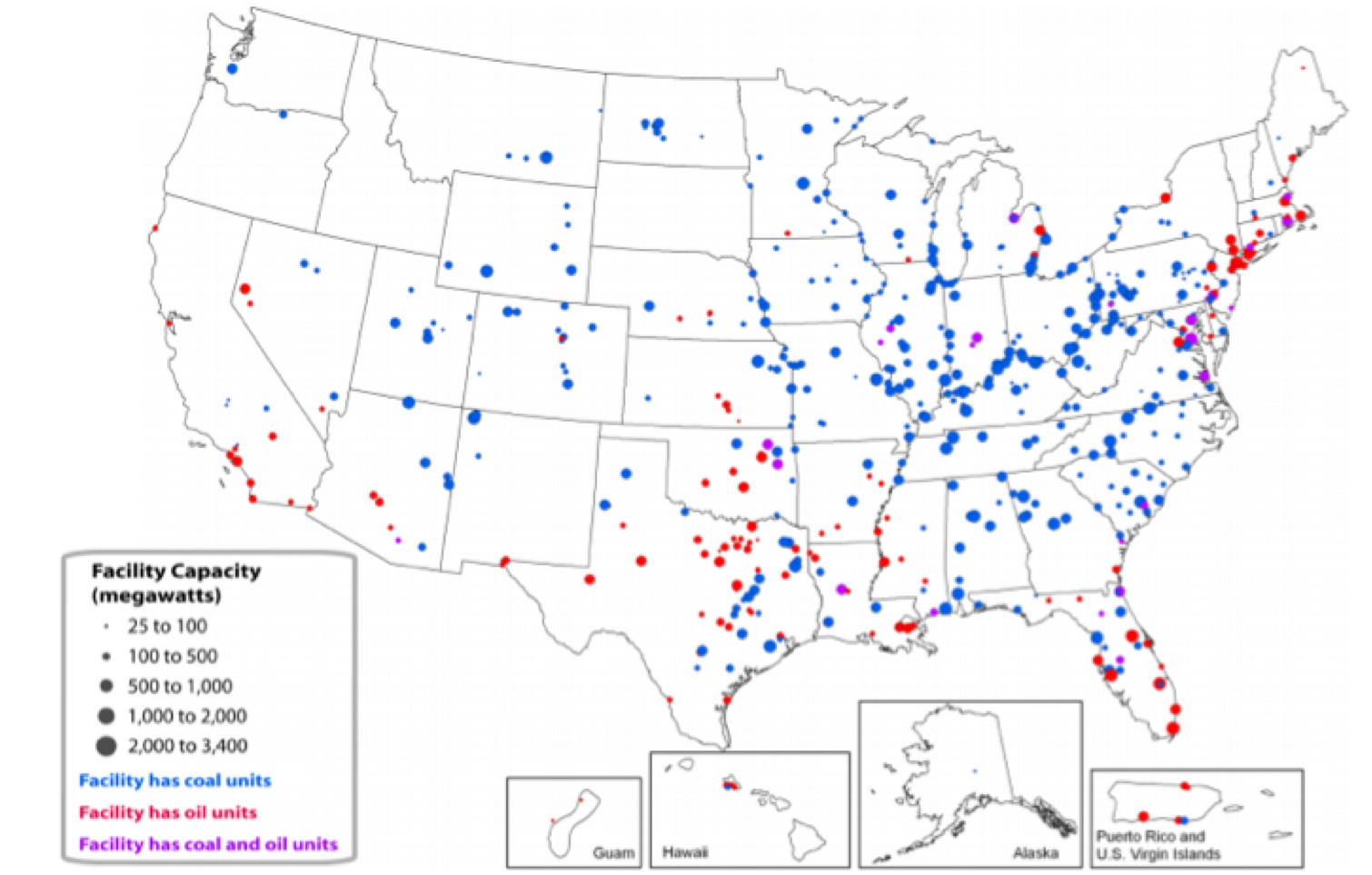

Let’s start with some perspective on how many coal-burning power plants are in the US, how big they are, and the amount and kind of emissions these plants produce. As illustrated in the map below (source: EPA), coal plants reside predominantly in the Midwest and Appalachian regions. Coal generation plants are marked in blue and oil generation plants in red. The regulations we’ll be talking about generally apply to both fuels, but we’ll focus on coal.

In 2012, some 540 US coal-fired plants collectively burned 1 billion tons of coal to produce 1.5 Million GWh of electricity, thereby providing 37% of the nation’s electric power needs. (Source: EIA). Gas-fired plants generated slightly less power, providing 30% of the nation’s total power needs. Nuclear plants provided another 19%. The remaining 14% of the nation’s power generation in 2012 was produced by a collection of plants fueled by oil, hydroelectric and renewable sources.

Collectively, these 500+ coal-fired plants are responsible for 33% of the nation’s output of carbon dioxide (CO2), a greenhouse gas considered by some to be a contributor to global warming. The plants also produce significant quantities of sulfur dioxide (SO2), which causes acid rain, nitrogen dioxide (NO2), which contributes to acid rain, and mercury (Hg). The coal industry has worked hard to minimize these emissions. Given the scale of coal-fired generation today it will continue to play a significant role in the country’s power generation mix going forward.

Legislation

No single piece of federal legislation has done more to reduce power plant emissions than the 1970 Clean Air Act (CAA). It’s worth noting that the 1970 legislation was actually a set of amendments: the original act was passed in 1963. Since 1970 the CAA has been amended two more times, in 1977 and 1990.

EPA regulations such as the CAA have been heavily contested in the courts, with lawsuits having been brought by both private entities and states. In 2001, nearly four decades after the original CAA was signed into law, the Supreme Court was compelled to affirm that the EPA even had the authority to regulate air pollution.

In March 2005, the EPA issued a Clean Air Interstate Rule (CAIR). This act placed further limits on emissions of SO2 and NO2 but not CO2 or mercury. The ruling, and those that follow below have been heavily contested in the courts. The CAIR for example, was reversed by an appeals court in 2008.

In July 2011, the EPA released a Cross-State Air Pollution Rule (CSAPR) to replace CAIR. This law required 27 states to significantly reduce NO2 and SO2 emissions from plants in the eastern half of the United States. The EPA’s intent was that CSAPR would be implemented in stages through 2014. The ruling was contested, however, and in August 2012 an appeals court vacated the rule, sending it back to the EPA for revision.

In December 2011 the EPA announced new standards to limit mercury emissions via the Mercury and Air Toxics Standards for Power Plants (MATS) rule. This rule affects both existing and new plants, and requires compliance by 2015. It is estimated that 1,100 coal-fired units will be affected with retrofits. Like the other emissions rules, MATS is also being contested, and members of Congress have introduced bills to halt the proposed standards.

Greenhouse Gases

In March 2012, the EPA released a New Source Performance Standard (NSPS), a pollution control standard authorized under the CAA which proposed new restrictions on CO2 emissions. The proposed limits would apply only to new build plants, both coal and gas. These limits will not affect current designs of gas-fired plants, which already meet the proposed limits. But new coal plants would face potentially insurmountable technological and financial obstacles to meet the limits. So if passed into law, these new limits on CO2 emissions could signal the end of any new coal plant construction.

Emissions Costs

As a consequence of legislation to control emissions, coal plant generators face mounting compliance costs on three fronts as follows:

Costs incurred at the power plant - when scrubbing or capture technologies are applied to reduce emissions of regulated materials. The EPA estimates that power generators have invested $100B since 1970 to meet the evolving federal emissions standards.

Costs to implement federal or state-mandated cap-and-trade programs. A cap-and-trade market for NO2 and SO2 began in 2003 as an early part of the CAIR act. But the act was reversed in 2008 and later partially re-instated, causing the over-the-counter market for these permits to essentially collapse. Since then Federal mandates for cap-and-trade appear to be dead in the water, but regional cap-and-trade programs remain in place. For example, ten Northeast and Mid-Atlantic states formed a compact whereby they voluntarily limit CO2, and trade permits to exceed allowances. RBN Energy recently reviewed a similar program in California (see AARGH Matey! Cap’n TradeSets Sail in California.)

Uncertainty Costs. These are potentially the highest costs that coal-fired plant generators face. Recent and proposed regulations could shut some plants and/or make the construction of new plants cost prohibitive. Power providers and investors dislike this uncertainty, and may direct capital elsewhere.

Shifting Generation Landscape

In the end, Federal regulations to limit power plant emissions encourage power producers to retire power plants that cannot be economically updated to meet higher standards. Uncertainty around challenges to and implementation of these regulations provides further encouragement for retirements. As one might expect, power companies are responding.

In 2012, producers retired 9 GW of coal-fired generation. Another ~30 GW of retirements between now and 2016 have been announced (source: Brattle Group). That’s 10% of the nation’s coal-fired capacity, and under various regulatory scenarios that number could double. These are tough times for coal, as we discussed a few months back in ‘Core Apps in Tough Times.’

Impact on Coal Producers

Since up to 90 percent of US coal supplies are consumed by power generation the future of coal producers and coal powered generation are joined at the hip. Coal producers have been left searching for new overseas markets to supply. Domestic coal production is falling. To see how badly the US coal industry has been hurting over the past four years, consider the current market capitalization of three of the largest US coal producers compared to their 2009 highs:

|

NAME |

PRE-2009 MARKET CAP HIGH ($M) |

MARCH 3, 2013 MARKET CAP ($M) |

|

Walter Energy |

4,254 |

1,880 |

|

Peabody Energy |

22,270 |

5,520 |

|

Consol Energy |

20,150 |

6,990 |

Conclusion

Suffice to say these are tough times for coal-fired power generation. Coal production, transportation and coal-fired power generation represent a multi-billion dollar industry. With deep pockets, various interests will lobby for fewer regulations and contest those already passed into law. There are also numerous clean coal technologies being researched. These efforts will certainly slow the decline of coal but at present do not look likely to reverse it.

About the song

Legendary blues singer Howlin' Wolf recorded Smokestack Lightning in 1956. According to Wolf, 'We used to sit out in the country and see the trains go by, watch the sparks come out of the smokestack. That was smokestack lightning.' Smokestack Lightning received a Grammy Hall of Fame Award in 1999 honoring its lasting historical significance. The song is ranked #285 in Rolling Stone magazine's list of the 500 Greatest Songs of All Time.

Comments

In March 2012, the EPA released a New Source Performance Standard (NSPS), a pollution control standard authorized under the CAA which proposed new restrictions on Carbon Dioxide emissions. The proposed limits would apply only to new build plants, both coal and gas. These limits will not affect current designs of gas-fired plants, which already meet the proposed limits. But new coal plants would face potentially insurmountable technological and financial obstacles to meet the limits. So if passed into law, these new limits on Carbon Dioxide emissions could signal the end of any new coal plant construction.

Possible investment opportunity, should the proposed (NSPS) bill become law, the older Coal Generation Plants, some of which have been recently decommissioned, or are scheduled for decommission, would now represent an investment opportunity as these facilities could be retofitted, enlarged, without qualifying as new build plants under the proposed legislation. Since infrastructure already exists on-site, expansion and retrofit seem more attractive to a coal company, which may seek to purchase and operate the coal generation plant privately, selling the electricity back to the power company. Certainly, if NSPS becomes law, power corporations will be discouraged from maintaining or constructing coal fired generation capacity. The Coal Company benefits: adds value to its end-sale product, diversifies the company's interests with minimal affect on domestic or international sales. A similar circumstance existed with PADD1 oil refineries becoming more of a nuisance than they were worth for the Oil Corporations, but private companies have been able to purchase and operate some of these same refineries at a profit. Therefore, a window of opportunity may exists for Coal Companies, before Electrical Corporations decommission their coal fired plants, as the option for any new construction could be closed by the proposed NSPS. Further, if future break-throughs in clean coal technology reduce N0x, S0x, & Hg emissions, and the future price for natural gas increases, the Coal Companies may find themselves significantly advantaged.