Producers in the Haynesville Shale had anticipated that growth in LNG exports in 2024 would goose prices and propel the play’s role as a crucial source of LNG feedgas. Instead, lackluster demand, exacerbated by delays at the Golden Pass LNG project, contributed to lower-than-expected natural gas prices, which caused some producers to scale back drilling plans and trimmed Haynesville production from about 16 Bcf/d in the first half of 2023 to less than 14 Bcf/d by the end of 2024. So, what do they have planned for 2025? In today’s RBN blog, we’ll discuss the Haynesville’s promise and challenges and highlight what E&Ps there are planning.

Visualize the infrastructure behind U.S. NGL movement.

The U.S. NGLs Map provides a comprehensive view of the transport, processing, and export networks moving NGLs across the U.S.

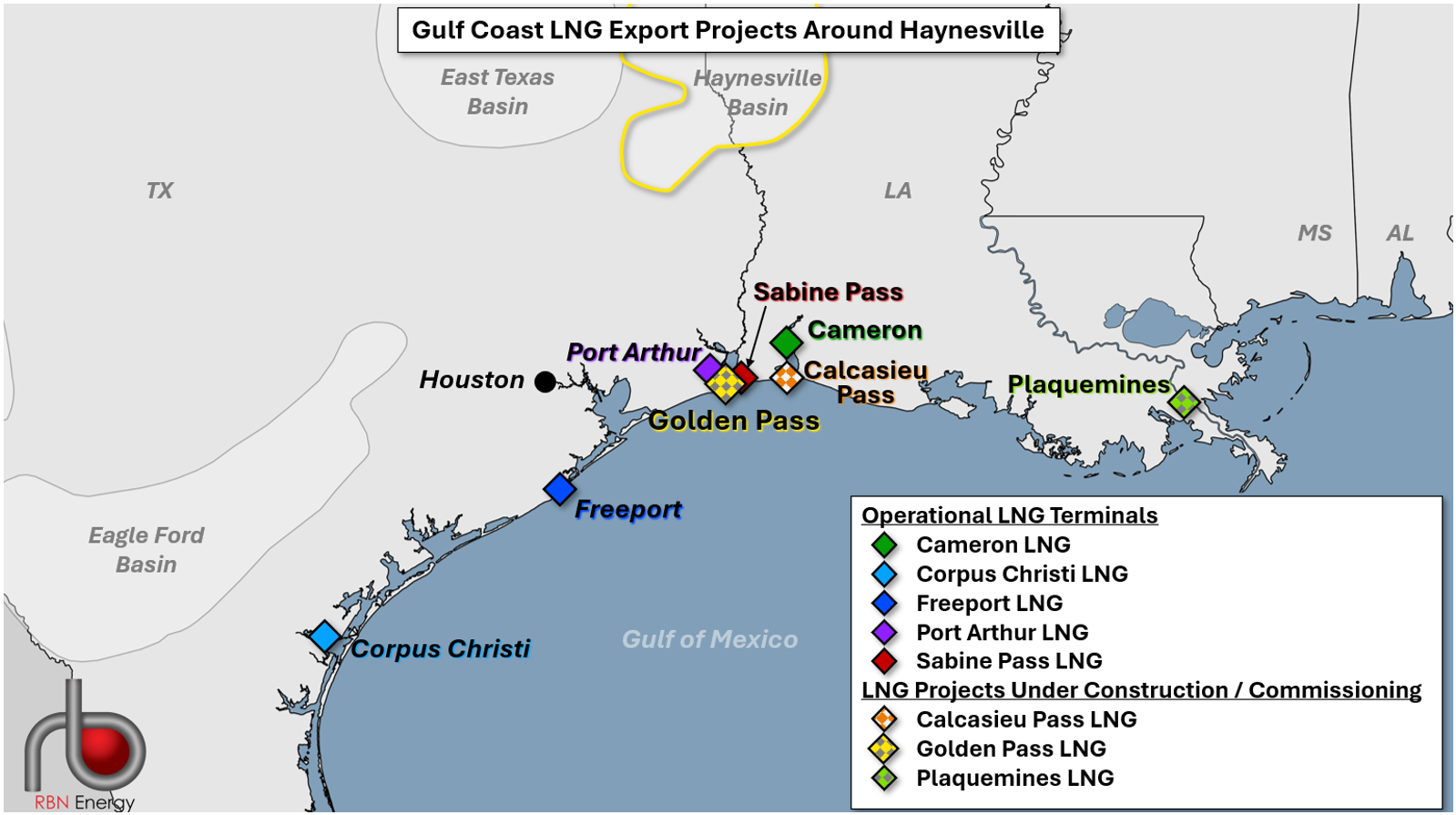

We’ve written a great deal about the Haynesville Shale (yellow-bordered region in Figure 1 below) — one of the OG’s of shale development which stretches across portions of Northeast Texas and Northwest Louisiana — in the RBN blogosphere (see 50 Ways to Leave Louisiana) and its role as an essential source of LNG feedgas. The Haynesville along with the prolific Permian Basin and the Eagle Ford are among the most prominent and promising sources of additional feedgas for new export facilities being built along the Gulf Coast (colored diamonds in Figure 1), and a long list of pipeline projects are being planned and built to transport increasing volumes of gas from those basins to LNG export facilities. However, unlike the Permian (and a large swath of the Eagle Ford), where gas is produced largely as a byproduct of oil, and thus sensitive to oil prices, the Haynesville (along with parts of the southern Eagle Ford) is primarily a gas-producing region, and is correspondingly sensitive to gas prices.

Figure 1. Gulf Coast LNG Export Projects Around the Haynesville Basin. Source: RBN

So, when the pace of new export-capacity additions began to slow dramatically in 2023 and no new liquefaction/export capacity came online in 2024 (dashed red box in Figure 2 below) for the first time since the start of the U.S. LNG export boom in 2016 due to major construction delays at Golden Pass LNG and minor delays at Plaquemines LNG (see Tired of Waiting for You), that stifled a forecast price rise which, in turn, cascaded back to gas-focused producers in the Haynesville. Producers are not incentivized to boost output when prices aren’t supportive or when doing so would only serve to oversupply the market. More often these days, sophisticated producers adjust their plans based on current price signals balanced against any hedging they’ve done (see I Walk the Line).

About the song

“Sitting, Waiting, Wishing” as written by Jack Johnson and appears as the sixth cut on his third studio album, In Between Dreams. Released as a single in March 2005, it went to #25 on the Billboard Modern Rock Tracks and #66 on the Billboard Hot 100 Singles charts. Personnel on the record were: Jack Johnson (vocals, acoustic guitar), Sam Lapointe (lead guitar), Simon Tessler (bassoon), Zach Gill (piano, accordion, melodica), Adam Topol (drums, percussion), and Merlo Podlewski (bass).

In Between Dreams was recorded at Jack Johnson’s The Mango Tree studio in Hawaii. Produced by Mario Caldato Jr., it was released in March 2005 and went to #2 on the Billboard 200 Albums chart. It has been certified 2x Platinum by the Recording Industry Association of America. Four singles were released from the LP.

Jack Johnson is an American singer, songwriter, musician, record producer, documentary filmmaker, actor, and former professional surfer. He has released eight studio albums, two live albums, a soundtrack album, three EPs, and 33 singles. He has won an ASCAP Award, a Brit Award, and three Billboard Music Awards. His last release was the Meet the Moonlight studio album, released in June 2022. The Meet the Moonlight World Tour took place in 2022-24. He continues to record and tour.