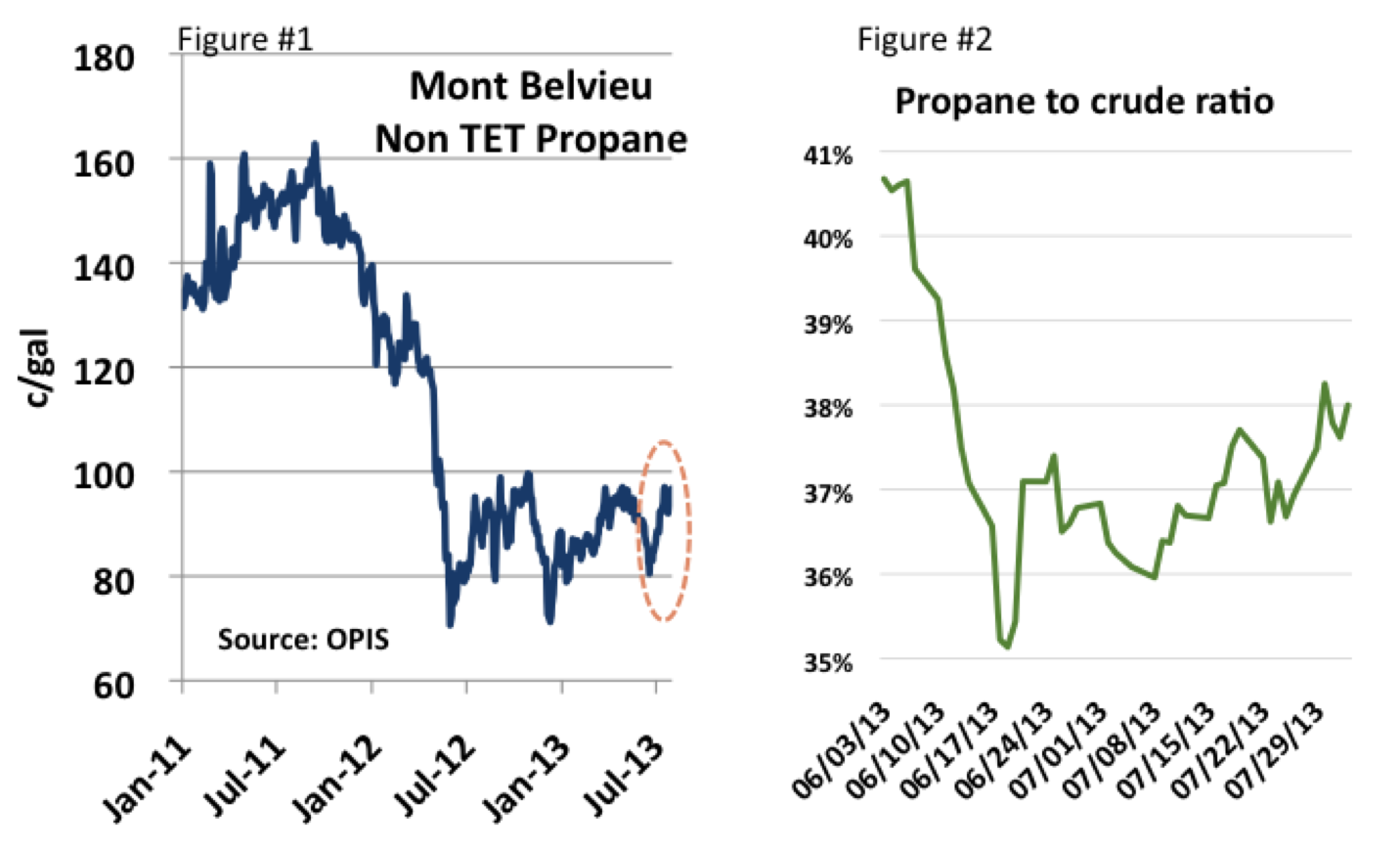

Over the past six weeks, the price of Mont Belvieu propane has strengthened by more than 20%. That’s not supposed to happen in the middle of the summer doldrums when the only growth market for propane is backyard BBQ grills. Could supply be falling? Not hardly. The most recent Energy Information Administration (EIA) numbers show propane production from natural gas processing plants hitting another record, up 42% in the past four years. You might think that kind of supply growth would crush prices. But there is an escape valve for excess propane supplies: Exports – and lots of them. Fortunately international markets have been there to soak up the barrels. Today we will examine how this is all shaking out in the U.S. propane market.

This is Part 2 of a series on NGL markets that we started last month, with Part 1 titled Dirty Deeds Done Dirt Cheap – Will NGL Prices Continue to Drop? In that posting we surveyed each of the NGL markets and how all NGL prices had hit the skids, with the light ends (ethane and propane) taking the brunt of the hit, while the heavies (butanes and natural gasoline) fared slightly better. We also drilled down on the propane market to see how propane prices had been squeezed down to only 35% of the price of WTI crude -- “dirt cheap” compared to a historical ratio of somewhere in the 60% range.

But no sooner than we posted that blog, propane prices started to rebound – increasing from about 80 cnts per gallon into the mid to upper 90’s per gallon over the past few trading sessions (see Figure #1, orange oval). Yes, one reason is WTI moving up to $107/bbl. But that’s not all. The ratio of propane to crude oil has actually moved up to 38% (Figure #2).

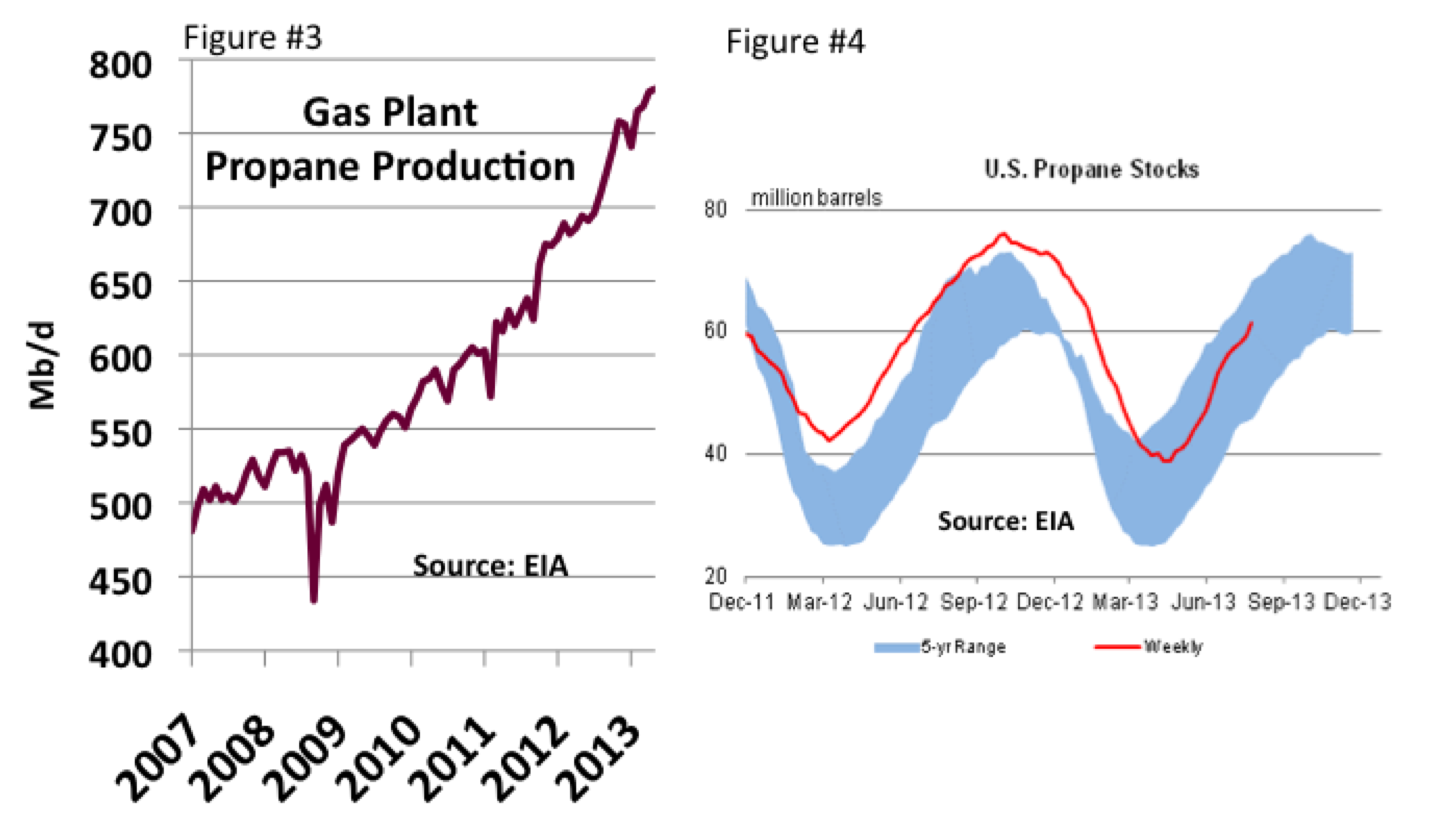

Granted that is not a huge move. But the interesting thing to note is that the direction is up, not down. You might think that this time of year propane should be getting relatively weaker. It is the low point for residential/commercial demand. And supply keeps coming on strong. Figure #3 shows EIA natural gas production of propane through May 2013. From about 500 Mb/d back in 2007, production is now approaching 800 Mb/d. And all that growth is happening at a time when the residential/commercial demand for propane has been on a downhill slide for years.

Again you might think that kind of supply growth would result in a huge inventory overhang. But as shown in Figure #4, propane inventories are not that far ahead of the midpoint of the five year range for this time of year. Clearly all that extra propane is going somewhere. It is headed overseas.

Here Come the C3 Exports

We’ve addressed expectations for a major expansion in U.S. propane exports in several previous blogs. In Exports Prescribed for Propane Relief we looked at new dock capacity that is making the increase in exports possible. In Come On, Move Your Propane, Do the Conga; Latin America Exports Getting Stronger we explored the global markets that are absorbing all of the surplus propane. These postings from months back talked about the coming surge in exports. Now that surge is upon us.

Figure #5 and #6 below illustrate the magnitude of the surge. These numbers are sourced from our good friends at IHS/Waterborne Energy who track the lifting and delivered volumes for every voyage of every NGL tanker in the global market. Exports have grown from next to nothing in 2007 to more than 250 Mb/d in 2Q2013 through July 2013. At the same time, waterborne propane imports have declined from over 100 Mb/d in 2007 to next to nothing today. That is a 350 Mb/d shift in the propane import/export balance – and recall that total natural gas plant production was only 500 Mb/d in 2007. By any standard that is a market shift of biblical proportions.

About the song

"Cocaine" was written and recorded by the great JJ Cale in 1976, but is mostly known from the cover version released by Eric Clapton in 1980. JJ Cale passed away on July 26, 2013 in La Jolla, CA.

Comments

The Panama canal expansion should come online in 2015. Will that increase propane exports to Asia?

In reply to How will exports to Asia be affected by Panama Canal Expansion? by Tom Morgan

It will definitely reduce the transportation cost, and thus should increase the volumes going to Asia.