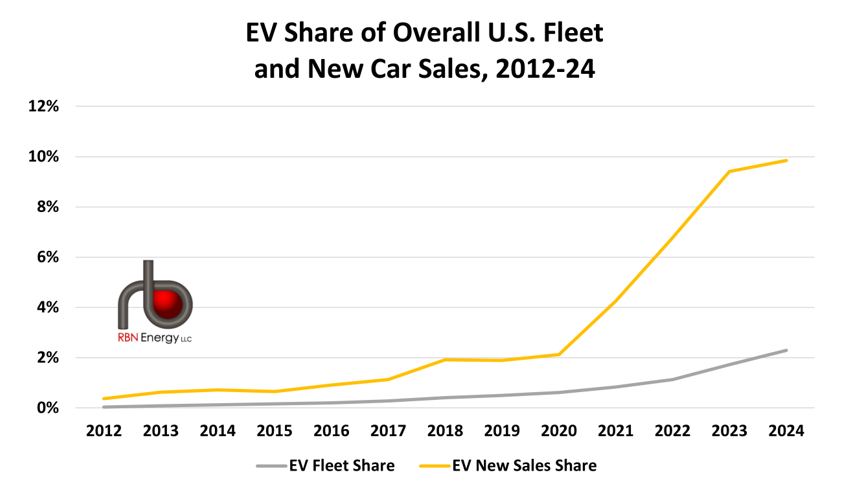

Expectations for electric vehicle (EV) adoption in the U.S. took a sharp detour into uncharted territory earlier this month when President Trump signed the landmark budget reconciliation bill into law. Known as the One Big Beautiful Bill Act (OBBBA), the law dramatically scales back EV subsidies, eliminates penalties for automakers that don’t meet fuel-efficiency standards, and significantly restricts state-level zero-emission vehicle (ZEV) programs. In today’s RBN blog, we look at why the law is likely to slow the pace of EV adoption and impact forecasts for vehicle sales and gasoline demand — a key topic in the just-published Future of Fuels report from our Refined Fuels Analytics (RFA) practice.

We’ll start with one of the most significant changes in the OBBBA, or at least one that is very noticeable to consumers: the early termination of the New EV Tax Credit (30D), which has helped EVs move closer to price parity with internal combustion engine (ICE) vehicles. Under changes made to the tax credit in 2022’s Inflation Reduction Act (IRA), EVs complying with either critical mineral or battery component requirements are eligible for tax credits of $3,750 each, or $7,500 if a vehicle meets both. In addition, a tax credit of up to $4,000 was for the first time extended to used EVs. The IRA also gave buyers the option of using the credit as part of their down payment or as cash-back from the dealer. (Under earlier legislation, buyers had to wait until they filed their taxes in the following calendar year to receive the value of the credit.)

Those tax credits are ending as of September 30 — seven years earlier than under the IRA — but the OBBBA makes a couple other key changes as well. Leased EVs will no longer be classified as commercial vehicles, a loophole that has allowed leasing companies to claim the full tax credit, then pass it on to the consumer. (About half of new EVs are now leased, according to market reports, up from 15% in 2022. The industrywide lease rate for all new vehicles is about 25%.) In addition, the Commercial Clean Vehicle Tax Credit (45W) is also being discontinued. Businesses and tax-exempt organizations that purchase qualified clean vehicles — battery-electric, fuel cell and plug-in hybrid vehicles — for commercial use qualify for the credit. The credit can be up to $40,000 for larger vehicles (14,000 pounds or more, such as heavy-duty trucks, school buses and semis) and up to $7,500 for smaller vehicles.

Figure 1. EV Share of Overall U.S. Fleet and New Car Sales, 2012-24. Source: RBN Refined Fuels Analytics

About the song

“Shake It Up” was written by Ric Ocasek and appears as the second song on side one of The Cars’ album of the same name. Released as a single in November 1981, it went to #4 on the Billboard Hot 100 Singles chart. According to Cars drummer David Robinson, “The song had been kicking around for years,” and when the band decided to approach it again as a fresh tune, it changed every element of it and “put back together, it was like a brand-new song.” Of note is lead guitarist Elliot Easton’s guitar solo, in which he switches from a Fender Telecaster for the country-infused parts to a Gibson SG for the heavier rock riffs. Elliot’s country inflections in his soloing always gave The Cars’ songs a unique flavor. Personnel on the record were: Ric Ocasek (lead vocal, rhythm guitar), Benjamin Orr (bass), Elliot Easton (lead guitar, backing vocals), Greg Hawkes (keyboards, backing vocals), and David Robinson (drums, percussion).

The album Shake It Up was recorded in early 1981 at Syncro Sound in Boston, with Roy Thomas Baker producing. Released in November 1981, it went to #9 on the Billboard 200 Albums chart and has been certified 2X Platinum by the Recording Industry Association of America. Four singles were released from the LP.

The Cars were an American rock band formed in Boston in 1976 by Ric Ocasek, Benjamin Orr, Elliot Easton, Greg Hawkes and David Robinson. Emerging from the new wave scene, the band featured Ocasek and Orr alternating on lead vocals, with Ocasek being the primary songwriter. They released seven studio albums, eight compilation albums and 26 singles before disbanding in 1988. The Cars were inducted into the Rock and Roll Hall of Fame in 2018. Benjamin Orr died in 2000 and Ric Ocasek passed away in 2019. The surviving members continue to record and perform in various projects.