The recent dramatic narrowing of the WTI discount to Brent to around $3/Bbl (from $23/Bbl in February) took place at the same time as Cushing, OK crude inventories fell by 23 percent. Both these events have been trumpeted as signaling an end to the three-year logjam preventing landlocked crude supplies from reaching the Gulf Coast by pipeline. Yet the turnaround in Cushing inventories owes as much to declining inflows to Cushing from Canada and West Texas as it does to a flood of crude to the Gulf Coast. An uptick in refinery consumption in the Midwest and falling prices on the CME NYMEX West Texas Intermediate (WTI) futures market (backwardation) have also played an important part in the drop in Cushing inventories. Today we look at what lies behind the crude inventory slide.

Source: EIA

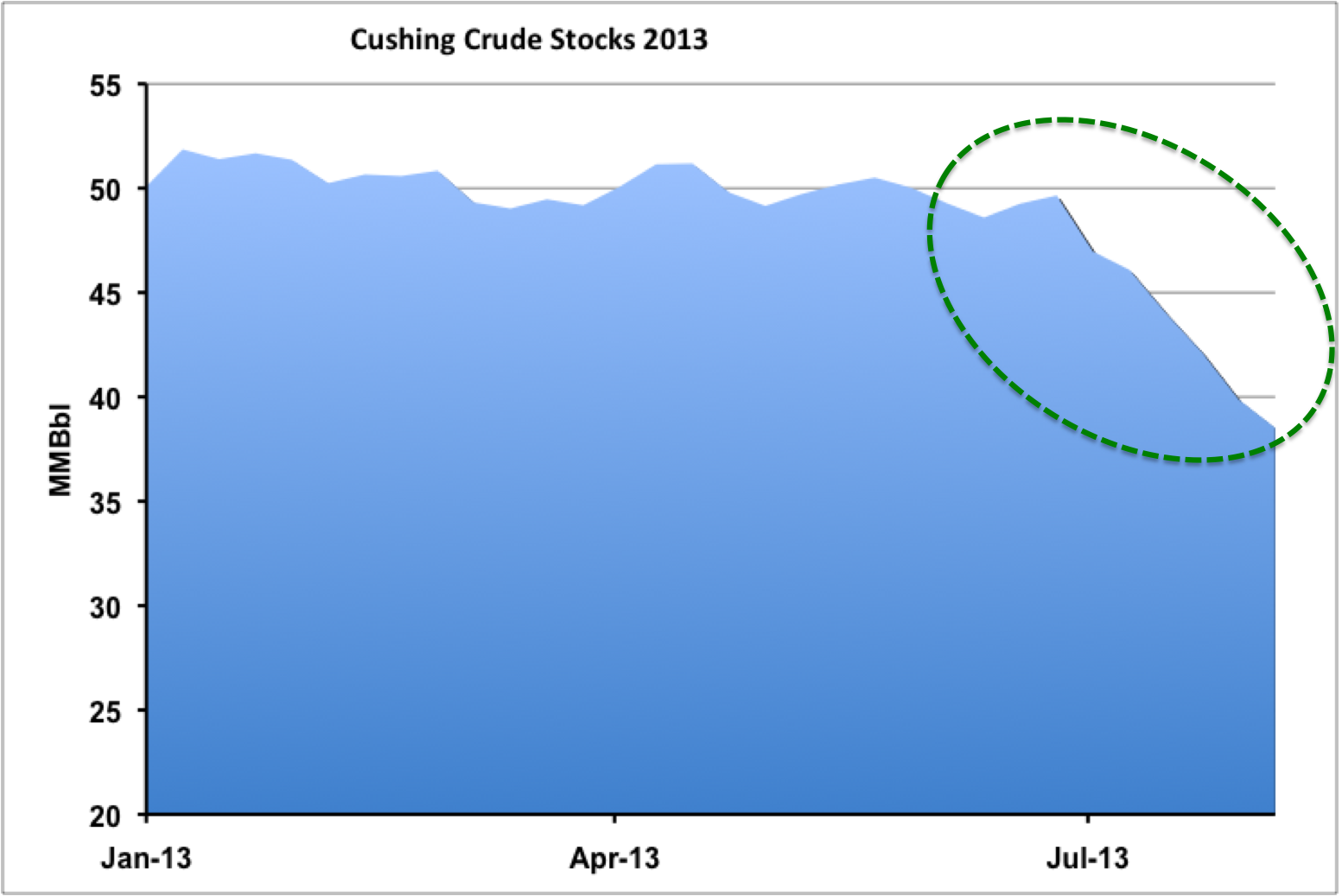

Since the end of May 2013, inventories at the Cushing, OK trading hub that is the delivery point for the CME NYMEX WTI futures contract have fallen from just over 50 MMBbl to 38.5 MMBbl, as reported last week (week ending August 9, 2013) by the Energy Information Administration (EIA). The chart above shows that Cushing stocks climbed close to 52 MMBbl at the end of January and stayed near 50 MMBbl through May before declining significantly in June and July (green dotted circle). Cushing inventories have been at record levels over the past three years as a result of pipeline constraints out of the Midwest hub to refining markets on the Gulf Coast. The glut of crude built up as a result of increases in domestic production shipped to the region from North Dakota and Canada. Rapid increases in production overwhelmed Midwest refining capacity and the limited pipeline infrastructure out of Cushing to Gulf Coast refineries. As a consequence of oversupply in the Midwest, inland crudes priced against WTI were heavily discounted against coastal crudes priced against the international crude benchmark Brent. The WTI discount to Brent reached as high as $28/Bbl and averaged $18/Bbl during 2012. In recent weeks the drawdown in Cushing stocks has been accompanied by the narrowing of the WTI discount to Brent so that the two crudes are now trading in a range about $2-$3/Bbl apart (see Strangers in the Night).

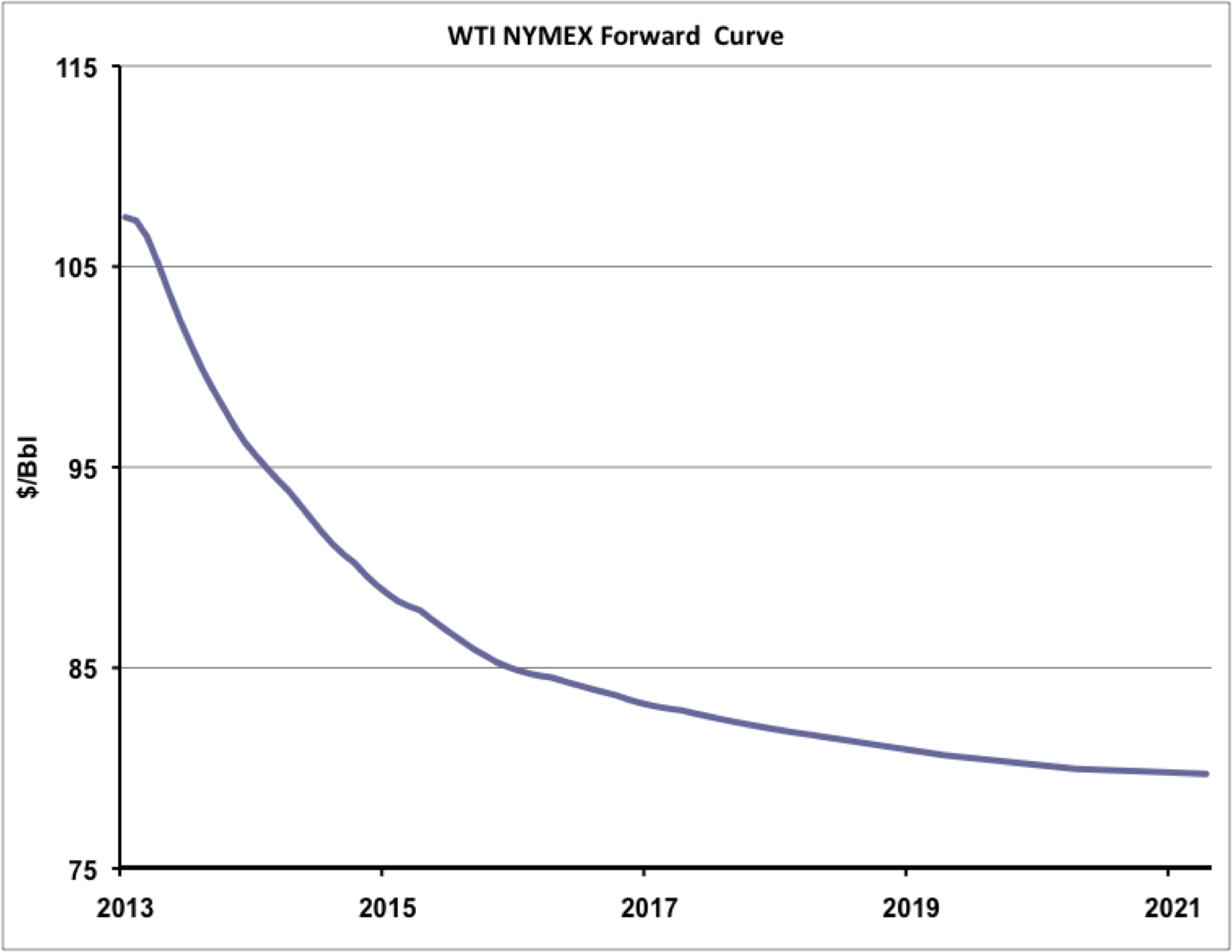

There are a number of factors that explain the drawdown in Cushing stocks over the past two months. For starters there is a clear financial motive for producers and marketers who have been holding crude in Cushing storage to start selling their supplies now. Prompt cash WTI prices have increased by 24 percent from their low this year of $86.68/Bbl in April to close at $107.46/Bbl on Friday (August 16, 2013). With WTI closing the gap on Brent (the discount Friday was $2.94/Bbl) crude sellers at Cushing are getting a much better deal than when WTI was more heavily discounted. The pricing signal from the forward curve is also loud and clear. The chart below shows the WTI forward curve of futures prices as of Friday August 16, 2013.

Source: CME data from Morningstar

The WTI curve is clearly in big-time backwardation. We have described backwardation – where prices in the future are lower – and its opposite, contango – where prices in the future are higher than today, previously (see Crude Oil Blues and Record Stocks). At the moment prices for WTI delivered next month (September) are 17 cnts/Bbl higher than they are for delivery a month further out in October. The downward slope of the backwardation after October gets steeper. Prices for WTI delivered in January 2014 are $3.74/Bbl lower than for September. Prices for delivery a year from now in August 2014 are a whopping $11/Bbl lower than today. Falling prices in the futures market indicate that market sentiment believes physical prices will be lower in the future. Generally backwardation is a signal to take crude out of storage and sell – especially at today’s high prices.

About the song

“Proud Mary” was written by John Fogerty and appears as the third song on side two of Creedence Clearwater Revival’s second studio album, Bayou Country. Released as a single in January 1969, it went to #2 on the Billboard Hot 100 Singles chart and has been certified 2x Platinum by the Recording Industry Association of America (RIAA). Ike and Tina Turner’s version of the song, released in January 1971, went to #4 Billboard Hot 100 Singles chart and earned them a Grammy Award. “Proud Mary,” a swampy blues raver with its refrain of “rollin’ on the river” (a line Fogerty borrowed from Will Rogers’ 1935 film, Steamboat Round the Bend), is hard to resist singing along to. Personnel on the record were: John Fogerty (lead, backing vocals, lead guitar), Tom Fogerty (backing vocals, rhythm guitar), Stu Cook (bass), and Doug Clifford (drums).

Bayou Country was recorded in October 1968 at RCA Studios in Hollywood, with John Fogerty producing. Released in January 1969, the album went to #7 on the Billboard 200 Albums chart and has been certified 2x Platinum by the RIAA. “Proud Mary” was the only single released from the LP.

Creedence Clearwater Revival, also referred to as Creedence and CCR, were an American rock band formed in El Cerrito, CA, in 1967 by John Fogerty, Tom Fogerty, Stu Cook and Doug Clifford. They had all played in bands together since 1959, first as The Blue Velvets and then The Golliwogs before settling on the CCR name in 1967. They released seven studio albums, three live albums, 41 compilation albums and 29 singles. The band officially broke up in 1972. They were inducted into the Rock and Roll Hall of Fame in 1993. Tom Fogerty died in September 1990 at the age of 48. John Fogerty continues to record and perform as a solo artist. Stu Cook and Doug Clifford have performed together as Creedence Clearwater Revisited with touring musicians since the 1990s.

Comments

I read with interest your comments on the possible disappearance of the WTI discount vs. Brent when two newpipelines totalling 1150 Mb/d open in a few months. Your observations seem well taken.

Why, then, is the Dec 14 Brent-CL spread stil around $9 as of mid-morning Aug 30?

In reply to WTI Cushing Discount by Rick Marshall

My analysis of the current market is based on fundamental factors as best we understand them today.

The futures market represents trader's valuations today of commodities to be delivered at some point in the future. Three years ago (Aug 30 2010) the Dec 14 Brent - Cl spread was $1.59 and it has ranged to over $12 since then. Which one is correct?

The current futures market value for December 2014 assumes a discount of US crude to international crudes but it is not impossible to imagine that increased production outside the US together with lower international consumption (eg in China) would place downward pressure on international crude prices as reduced US consumption of imports leaves a glut of international supplies.

- This comment was submitted by member C Scouton -

Thinking about the last paragraph makes me wonder also what will happen when US Gulf Coast refineries get oversupplied and then Keystone XL dumps its load of dilbit into the market? Anyone there asking this question? Thanks.