The West Texas Intermediate (WTI) discount to Brent has been as wide as $27/Bbl in the past two years and traded at an average of $17.50/Bbl in 2012. Since February this year the spread has narrowed 80 percent to less than $5/Bbl – closing at $4.55/Bbl on Friday (July 5, 2013). Surging WTI prices are over $100/Bbl for the first time since May 2012.Today we look at what is behind the recent sudden narrowing in the spread.

Story So Far

Last month in our latest update on the long running Brent/WTI spread story we wondered whether it was time to “Tie a Yellow Ribbon Round a West Texas Oak Tree”. Here’s the cliff notes on “the spread” so far in case you have been living on another planet. Three years ago in June 2010, prices for the international benchmark Brent crude and the US domestic benchmark West Texas Intermediate (WTI) traded within $1/Bbl of each other. Then in August 2010, WTI began to trade at a discount to Brent that widened out as far as $28/Bbl in November 2011. As noted above, the spread averaged $17.50/Bbl in 2012 but dropped to just $4.55/Bbl on Friday.

The WTI discount to Brent that began to deepen in August 2010 resulted from a build up of crude inventory at the Midwest Cushing, OK trading hub. Growing crude production in North Dakota and Western Canada overwhelmed Midwest refinery needs and got caught in Cushing because of inadequate pipeline transport capacity to Gulf Coast refineries. There has been some relief to the Cushing stockpile – noticeably after the reversed Seaway pipeline began to flow crude from Cushing to Houston in June 2012 at an initial 150 Mb/d and was expanded in January 2013 to carry as much as 400 Mb/d. And then in April 2013 the Magellan Longhorn pipeline (also a reversal) began to flow 75 Mb/d from the Permian Basin in West Texas to Houston that would otherwise have ended up in Cushing. During the past twelve months there has also been a boom in moving crude by rail – particularly from North Dakota to the Gulf, East and West Coasts.

This Year

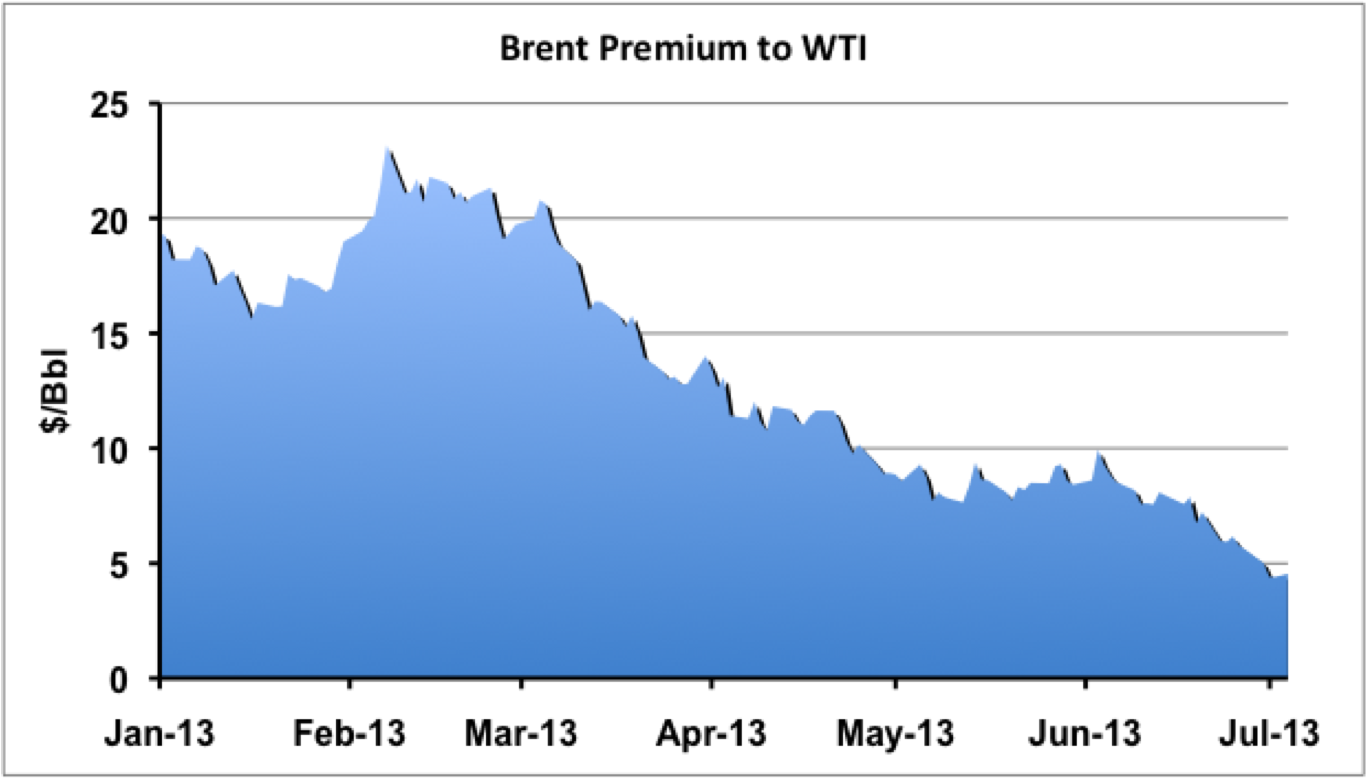

This year, as more capacity came online to transport crude past the Cushing logjam to coastal markets by rail and pipeline, the WTI discount to Brent has narrowed. The chart below shows the spread between the two crudes since the start of 2013. After reaching a high point in early February of $23/Bbl, the WTI discount narrowed to $10/Bbl in April 2013 in response to new capacity opening up from the West Texas Permian Basin on the Longhorn pipeline that redirected crude otherwise headed for Cushing, towards the Gulf Coast. From April through June, the spread traded in a range of $8 - $10/Bbl before starting to tumble again at the end of June to reach $4.55/Bbl at the end of last week.

Source: CME data from Morningstar

Midwest Drama

The spread had been expected to narrow this year by most commentators – in response to increased flows of domestic crude reaching coastal destinations. But the speed of that narrowing over the past two weeks from $10/Bbl to under $5/BBl caught most commentators off guard. And it appears to have been caused by events in the Midwest unconnected to the huge crude stockpile at Cushing – which is still there. Specifically two market events combined to create a sudden demand for supplies of light sweet crude such as Bakken from North Dakota and WTI from the Permian Basin at Midwest refineries. The first of these two events was the shutdown of a large production facility (known as an upgrader) in Western Canada that supplied up to 350 Mb/d of light sweet synthetic crude (syncrude) into the Midwest. The second event was the recent restart of the 250 Mb/d distillation unit at the BP Whiting, IL refinery after a shutdown and rebuild since last year. The BP rebuild will eventually allow the refinery to process heavy crude, but the new coker unit will take months to get ready for that task. In the meantime the refinery will process light sweet crude through the main distillation tower. The combination of these two events caused a new demand for 600 Mb/d of light sweet crude in the Midwest market. The result was a predictable increase in the price refiners are paying for Bakken crude and for WTI. The price of WTI has increased by over $6/Bbl since the end of June to trade over $100/Bbl for the first time since May 2012.

International Situation

As well as a domestic demand-pull on WTI supplies in the Midwest, the international situation also had a positive influence on WTI prices versus Brent. The futures markets that dominate the trade in these two storied crudes appear to have now received the message that the WTI discount to Brent is coming to an end and that this is not a bad thing. With that conclusion reached, fewer traders will speculate on the discount widening again – relieving downward pressure on WTI. At the same time the international position of Brent crude is perceived as weakened because the US is now far less reliant on international supplies of light sweet crudes like Brent or its West African equivalents. That throws a lot of those barrels (that the US previously imported) back onto the international market and the resulting oversupply places downward pressure on Brent prices. The Egyptian Coup on Wednesday and concerns about disruption to Libyan supplies have put upward pressure on world oil prices in general (both Brent and WTI) by threatening Mid East stability but has not strengthened Brent over WTI.

It is not clear if this recent narrowing of the WTI discount to Brent will stick. The sudden increase in demand for light sweet crude in the Midwest that we just described will be reversed when the BP refinery begins to process heavy crude in a few months and the Alberta syncrude upgrader is expected back online sometime in the fall. Both of those events will occur before a new pipeline expansion to Seaway (450 Mb/d twin line) and the completion of the Keystone Gulf Extension (700 Mb/d) bring large incremental flows of crude from Cushing to the Gulf Coast. So light sweet crude supplies could still get backed up in the Midwest and place downward pressure on WTI again this year – widening the discount to Brent again.

About the song

"Reunited" was written by Dino Fekaris and Freddie Perren and performed by Peaches & Herb. The song appears as the third track on Peaches & Herb's second studio album, 2 Hot! Released as a single in March 1979, the song went to #1 on the Billboard Hot 100 Singles chart. It has been certified 2x Platinum by the Recording Industry Association of America (RIAA). The has been covered by several artists and has appeared in various television shows and motion pictures. Personnel on the record were: Herb Fame (vocals), Linda "Peaches" Greene (vocals), Bob Bowles, David T. Walker and Wah Watson (guitar), Scott Edwards (bass), James Gadson (drums), Freddie Perren, Larry Farrow (keyboards), Electric Ivory Experience (synthesizers), Roger Glenn (flute), and Paulinho da Costa and Bob Zimmitti (percussion).

2 Hot! was recorded at The Mom & Pop's Company Store in Studio City, CA, in 1977-78, with Freddie Perren producing. All the songs on the album were written by Fekaris and Perren. Released in December 1978, the LP went to #1 on the Billboard Top R&B chart and #2 on the Billboard 200 Albums chart. The album has been certified Platinum by the RIAA. Three singles were released from the LP.

Peaches & Herb is an American vocal duo formed in Washington, DC, in 1966 by Herb Fame along with Francine "Peaches" Barker. Fame has remained a constant "Herb" in the duo while seven different women have sung as "Peaches." They have released 11 studio albums, 12 compilation albums and 32 singles. Peaches & Herb still tour, with Herb Fame and Wanda Tolson as "Peaches."

Comments