Midstreamers have been struggling to keep processing and natural gas pipeline constraints at bay in Oklahoma’s SCOOP/STACK plays, and the situation hasn’t gotten any easier in the past 18 months or so. Associated gas production from the Cana-Woodford has surpassed expectations, climbing 1 Bcf/d in that time to new highs near ~4.5 Bcf/d. Efforts by pipeline operators to keep pace with production gains have largely been on a piecemeal basis, mostly to tie in processing plants or modify/expand existing systems. Cheniere Energy’s Midship Project is looking to change that. The greenfield project, which received its final notice to proceed with construction from the Federal Energy Regulatory Commission (FERC) late last month, will level-shift takeaway capacity out of Oklahoma up by 1.44 Bcf/d in one fell swoop by the end of 2019. Today’s blog provides an update on Midship and other expansions in the region.

When we looked at associated natural gas production and the takeaway capacity situation in the crude- and condensate-focused SCOOP/STACK in central Oklahoma a couple of years ago, in early 2017 (see our Stardust blog series), midstream constraints for natural gas out of the plays were on the horizon but not imminent. Crude production from Oklahoma as a whole was recovering after the drilling slowdown in 2015-16 that followed the crude price crash of mid-2014. The comeback was almost entirely concentrated in the Woodford Shale’s Cana region (a.k.a. the Cana-Woodford) — the part of the Anadarko Basin underlying the 11-county SCOOP/STACK (as RBN defines the plays), and an area that had remained somewhat of a bright spot for producers even through the downturn in crude prices.

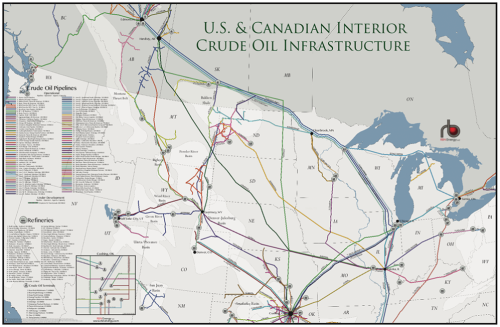

RBN's US & Canadian Interior Crude Oil Infrastructure Map features pipelines, refineries, and terminals that are new, existing, and under development from Canada to the Bakken Shale to Cushing.

With crude prices on the uptick and crude production rebounding, Oklahoma’s associated gas production output, which had stagnated in 2016, was also on the rise by early 2017 (again, led by the SCOOP/STACK area). Dry gas volumes from Cana-Woodford (Figure 1) at the time were approaching 3 Bcf/d, up from just under 2 Bcf/d in 2014, while gas pipeline takeaway capacity sat at around 3.5 Bcf/d, leaving some room for production to grow into. Expectations were that crude and gas production out of the area would continue climbing, but futures prices at the time suggested the growth would be more gradual and gas volumes wouldn’t hit that 3.5-Bcf/d capacity ceiling until sometime in 2020. But then, as crude prices took off to well above $60/bbl in 2017 and above $70/bbl through mid-2018, producers in the Cana-Woodford pressed on; gas production surpassed 3.5 Bcf/d by the end of 2017 and climbed nearly 1 Bcf/d from there to top 4.5 Bcf/d a year later. Now, crude prices are back down near the $60/bbl level, rig counts are again coming off as producers pare back their capex budgets, and production growth appears to be flattening near that 4.5-Bcf/d level, at least for now. However, as we noted last month in our blog The Upside of Down, that won’t necessarily translate to production declines in 2019 — many oil- and gas-weighted producers that reported capex declines also are expecting to post solid gains in output this year (albeit some of that as a result of the steep increases in 2018 carrying over into 2019).

About the song

"Moves Like Jagger" is an electro-pop song written by Adam Levine, Ammar Malik, Benjamin Levin, and Shellback. The record was produced by Shellback and Benny Blanco (Levin). It was the final single on the re-release of Maroon 5's third studio album, Hands All Over. The song features a guest vocal from Christina Aguilera and was first performed on the television talent show, The Voice, where Aguilera and Maroon 5 lead singer Adam Levine have been coaches. It reached #1 on the Billboard Hot 100, Adult Top 40, and Mainstream Top 40 charts. It went on to sell over 15 million digital copies, making it one of the most successful digital singles of all time. The video of the song, featuring Maroon 5 and Aguilera, with authorized vintage footage of Mick Jagger, was directed by Jonas Akerlund. It has received over 600 million views on YouTube. "Moves Like Jagger" was certified 9x Platinum by the Recording Industry Association of America (RIAA).

Hands All Over was produced by Mutt Lange and originally released in September 2010. It went to #2 on the Billboard Top 200 Albums chart and has been certified Platinum by the RIAA. It was re-released with the addition of "Moves Like Jagger" in June 2011. Personnel on the record were: Adam Levine (lead vocals, guitar), Jesse Carmichael (keyboards, guitar, backing vocals), Mickey Madden (bass), James Valentine (lead and rhythm guitar, backing vocals), and Matt Flynn (drums, percussion).

Maroon 5 is an American pop rock band from Los Angeles. They have made six studio albums. They have won one MTV Video Music Award, three AMAs, three Grammy Awards, and four Billboard Music Awards. Maroon 5 has sold more than 109 million singles and 27 million albums worldwide. The band still records and tours to this date, with a short European tour scheduled for this June.