Henry Hub natural gas futures prices are up 90 percent since their 10 year low of $1.907/MMBtu on April 19, 2012 – closing at $3.872/MMBtu on Friday. Over the same period the price of Gulf Coast ultra-low sulfur diesel fell by 4 percent to $3.027/gal. Nevertheless if you use liquefied natural gas to power a rail locomotive the equivalent fuel cost is about $0.48/gal (before adding in liquefaction and other costs). That is the reason why BNSF is taking a second look at LNG powered locomotive technology and Shell is building LNG plants in Louisiana and Sarnia. In today’s blog we review the appeal of gas-powered locomotives.

Low natural gas prices are flushing all manner of applications out of the woodwork. Nearly a year ago we wrote about plans to build plants that convert natural gas to refined products (see Gas to Liquids – The Hydrocarbons Mash). The fact is that hydrocarbons in the form of natural gas have become a whole lot cheaper than hydrocarbons in liquid form. That relationship is measured by the crude to gas ratio that you can follow every day via the RBN Spot Check feature on our website. Right now that ratio has come down from its high over 50 X in April 2012 to around 25 X last week. Before 2007 the ratio was around 7.5 X for 10 years or so (see Easy Come Easy Go – Crude to Gas Ratio Back Down to Earth Again). So it is still riding pretty high, from a historical perspective. That means the price of crude oil and the refined products that come from crude are a lot more expensive than natural gas.

Two weeks ago the CEO of the BNSF railroad (a subsidiary of Berkshire Hathaway) announced that the company would invest in a pilot program to build six liquefied natural gas (LNG) powered locomotives this year (2013). The move is motivated by the wide price difference between natural gas and the diesel fuel that the majority of US locomotives currently use. What is LNG? The process of liquefaction lowers the temperature of dry natural gas to -2630 Fahrenheit causing it to liquefy. In its liquid state 600 standard cubic feet of natural gas take up only 1 cubic foot of space, making it economical to transport natural gas where pipelines can’t work. Several previous RBN blogs have covered proposals to export natural gas as LNG in large vessels (see LNG Prices Shaky as DOE Approvals get NERA). The BNSF proposal is to liquefy natural gas and use it to fuel locomotives.

Before we get into the pro’s and con’s of the technology lets start with the math. As we learned when looking at coal-to-gas power generation switching, the economics at the margin boil down to the difference in the equivalent fuel costs required to do the same work (see Talkin ‘Bout My Generation). The energy content and efficiency of natural gas and diesel are different. The energy content of a gallon of diesel is 128.1 MBtu and the energy content of a gallon of LNG is 73.1 MBtu. However diesel is 1.68 X more efficient than LNG so it takes 1.68 gallons of LNG to do the same work as 1 gallon of diesel.

1 gallon of Diesel = 128.1 MBtu

1.68 gallons of LNG = 73.1 X 1.68 = 122.808 MBtu

The equivalent LNG to a gallon of diesel costs the same as 122.808 MBtu of natural gas or 0.122808 X 1 MMBtu

Based on Friday’s prices the cost of NYMEX natural gas was $3.872/MMBtu and Gulf Coast ultra low sulfur diesel (ULSD) was $3.0207/gal.

The equivalent LNG to a gallon of diesel therefore costs 0.122808 X $3. 872/MMBtu = $0.476

Diesel cost = $3.0207 – LNG equivalent = $0.476 – a difference of $2.54

Of course, that difference does not include the cost of liquefying the LNG, additional costs of getting the LNG to the right refueling locations, cost of conversions or any other of a myriad of additional factors. But considering only the cost of fuel, there is a very wide cost spread.

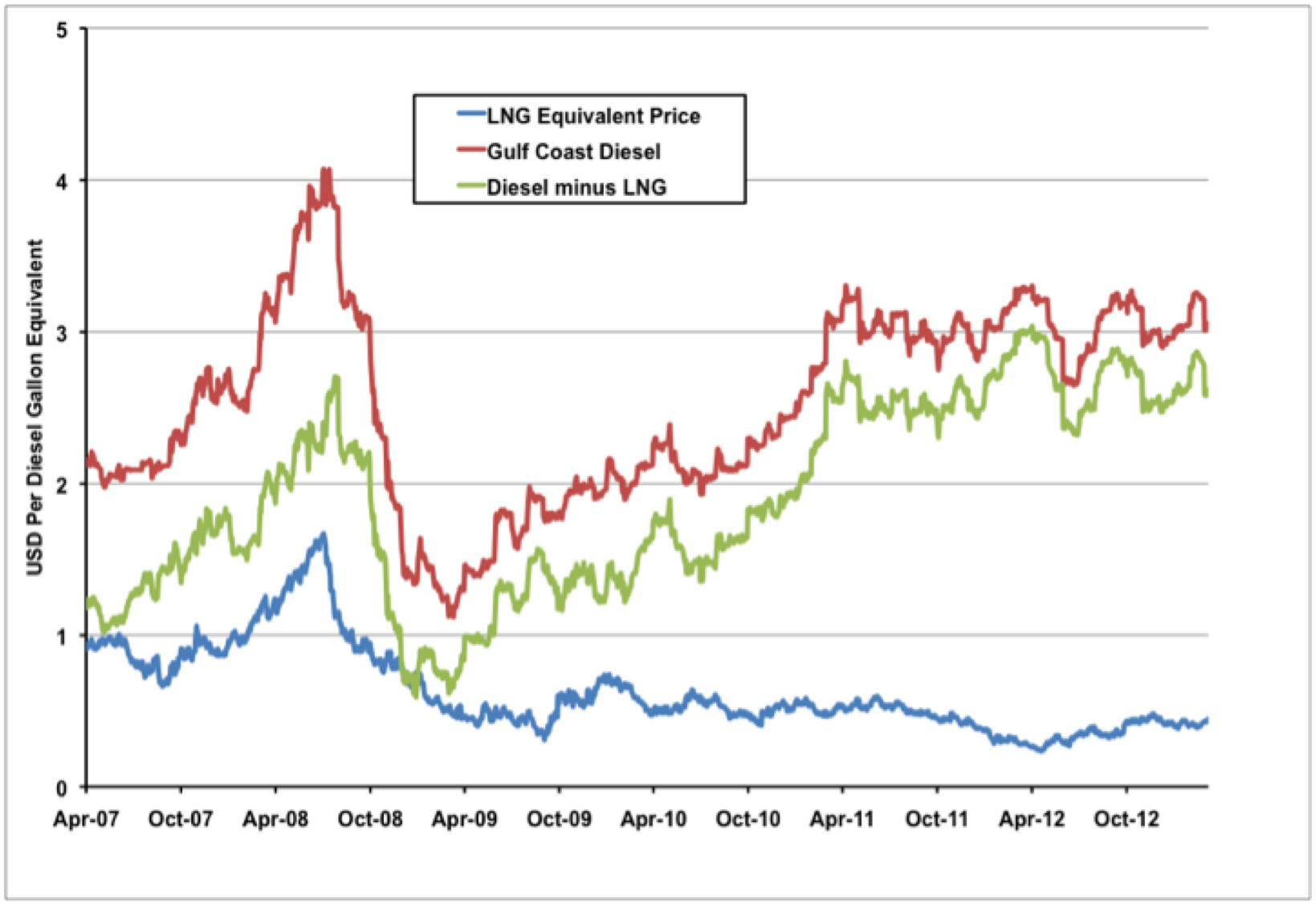

The chart below shows the Gulf Coast ULSD price over the past five years (red line) as well as the equivalent LNG cost (blue line) based on Henry Hub NYMEX natural gas prices. The green line on the chart is the difference between diesel and LNG costs. That difference has widened consistently since energy prices crashed after the recession in 2008. According to Energy Information Administration (EIA) data the railroads used 3.1 billion gallons of diesel in 2011. Based on the most recent differential we just calculated the differential in fuel cost from using LNG would be 3.1 B X $2.54 or about $8 B a year.

Source: CME Data from Morningstar (Click to Enlarge)

If you include many of the other cost factors mentioned above, the differential is not nearly so wide. But regardless of the factors included it is enough money to catch the attention of BNSF - the largest US railroad operator. The proposed pilot scheme involves constructing and testing six locomotives - three each from manufacturers GE and Caterpillar. BNSF did not share the cost of their investment in the pilot but it is clearly a worthwhile hedge against a continued high crude to gas ratio. The BNSF pilot scheme is also a timely hedge against forthcoming diesel fuel regulations that could prove very expensive for US railroads. Those regulations are the so-called “Tier 4” of the Environmental Protection Agency (EPA) emissions standards for railway locomotives. Those EPA standards came into force in 2000 and have progressively tightened since then. Tier 4 standards, which are expected to require exhaust gas after treatment technologies, become effective from 2015. From that point new build locomotives must conform to Tier 4 standards. Using LNG as a fuel would reduce the need for emissions controls because natural gas is relatively clean burning compared to diesel. So the fuel savings and regulatory avoidance potential make checking out LNG locomotives a no-brainer for the railroads.

Whether the pilot investment pays off by producing a practical prototype that can take the place of diesel locomotives is a lot less clear than the incentives to check it out. BNSF have been down this technology road before – in the 1980’s and again in the 1990’s. The picture below shows the locomotive that BNSF converted to dual fuels that ran on a mixture of diesel and a purified form of LNG called refrigerated liquid methane (RLM) for three years. The fuel was carried in a specially designed tender car that you can see behind the locomotive.

Source: Evaluation of Natural Gas Fueled Locomotives

Getting this technology to work is pretty complex and none of the earlier prototypes have ended up being commercially viable. One reason is that natural gas on its own does not support the workload expected from locomotives. The engines therefore have to use a small amount of diesel fuel as well as LNG to achieve the same performance as a diesel locomotive. Carrying the LNG in a tender car behind the locomotive has safety risks and uses up space on the train. The refueling logistics are complex because the LNG is stored at such low temperatures. The fuel cost savings that we described above could evaporate once higher transportation costs are factored in. Of course the cost of converting the existing fleet of locomotives (BNSF has 6,900) will not come cheap either.

All the same the possibility of using natural gas to power transportation is not just something the railroads are researching. At the same time as BNSF were talking about their pilot LNG locomotive scheme, Royal Dutch Shell announced that they will build two LNG plants at Geismar, Louisiana and Sarnia, Ontario in the next three years. Each plant will produce 12 Bcf/year of LNG. The output will be used to operate Gulf of Mexico supply vessels and potentially to power land based drilling rigs. In Sarnia Shell has signed up a Great Lakes cargo-ship operator as a future customer. US truck fleet companies are also ramping up their use of compressed natural gas (CNG) as an alternative to diesel. CNG is less complex than LNG to distribute since the gas is sold under pressure rather than at very low temperatures. Many municipal bus fleets already use CNG. Love’s Travel Stops last week announced plans to add CNG fueling pumps for heavy-duty trucks at eight locations in Texas and are adding 50 CNG-fueled tanker trucks to its fleet.

As long as the crude to gas ratio justifies the economics, the use of natural gas for transportation will attract market investment. The infrastructure costs of converting every gas station in the nation to natural gas is a huge barrier to entry that means you aren’t likely to be filling up the family Suburban with CNG anytime soon. For the railroads however the economics of more than a $2/gal fuel cost differential are powerful enough to justify investing in the technology to give them the option to change fuels in the future. For long distance predictable journeys like those that railroads, truck fleets and seaborne vessels make, there is every reason to look seriously at natural gas. US gas producers are also keen to develop new markets for their expanding production as they anxiously await approval to begin exporting LNG. Who knows where the crude to gas ratio will take us next?

About the song

"Long Train Runnin'" was written by Doobie Brothers band member Tom Johnston. The song appears as the second track on The Doobie Brothers third studio album, The Captain and Me. The song features Johnston on lead vocals and the rhythm guitar groove that propels the song. Although uncredited on the album, bay area blues harpist Norton Buffalo performed the harmonica solo on the tune. "Long Train Runnin'" evolved out of an instrumental jam tune the band had been performing live called "Osborn." As they were going through song ideas for their third album, producer Ted Templeman liked the groove on it and persuaded Johnston to come up with words and a melody for it. It was released as the first single from the album in March 1973, and went to #8 on the Billboard Hot 100 chart.

The Captain and Me was recorded at Warner Bros. Studios in North Hollywood between late 1972 and early 1973, with Ted Templeman manning production duties. It was released in March 1973, and went to #7 on the Billboard Top 200 Albums chart. Two singles that hit the top 20 were released from the album. Personnel on the record were: Tom Johnston (vocals, guitar, synthesizer, harmonica), Pat Simmons (vocals, guitar, synthesizer), Tiran Porter (bass, backing vocals), John Hartman (drums, backing vocals), and Michael Hossack (drums, congas, cymbals, timbales).

The Doobie Brothers are an American rock band formed in San Jose, CA, in 1970. They have been active for nearly five decades, with 29 different touring and recording members passing through its ranks during that time. The Doobie Brothers were featured on the debut of Don Kirshner's Rock Concert show in 1973. They have released 14 studio albums, five live albums, nine compilation albums, and 36 singles to date. They have won two Grammy Awards and were inducted into the Vocal Group Hall of Fame in 2004. The Doobie Brothers still record and tour to this date. The band, featuring long-time members Tom Johnston, Pat Simmons, and John McFee, are on tour with Santana through September. They are assisted on the road with five additional touring members, including Bill Payne (Little Feat) on keyboards.