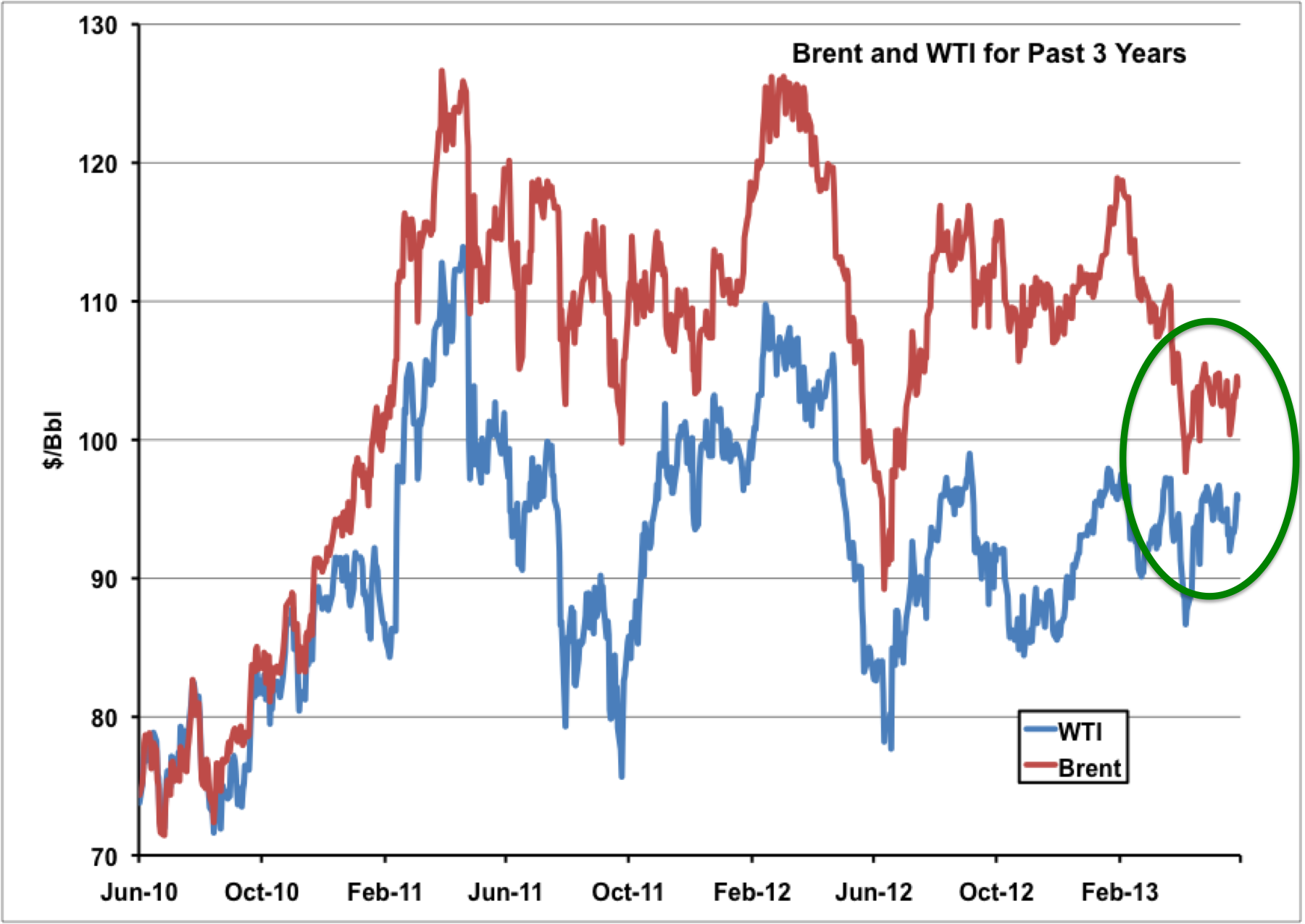

Three years ago in June 2010, prices for the international benchmark Brent crude and the US domestic benchmark West Texas Intermediate (WTI) traded within $1/Bbl of each other. Then in August 2010, WTI began to trade at a discount to Brent that widened out as far as $28/Bbl in November 2011 and averaged $17.50/Bbl in 2012. Since May 2013 the WTI discount to Brent has narrowed to an average $8.50/Bbl. Today we wonder if it’s time to tie a yellow ribbon round a West Texas oak tree.

Through the past 18 months of ups-and-downs between these two “Hollywood” crudes, we at RBN Energy have done our best to keep you up-to-date with their relationship. Our last blog on the Brent/WTI relationship was back on March 24 2013 (see Are They Never Ever Getting Back Together Again?). Before that we provided a post super bowl update in February (see Brent/WTI Reconciliation Dreams Shattered) and a New Year special in early January (see The Seven Gates of Hell for WTI Crude Traders). Since March of this year we have referred to the impact of the narrowing WTI discount to Brent on crude prices in North Dakota (see Brent WTI and the Impact on Bakken Netbacks) and on rail shipments from the Bakken to the Gulf Coast (see To The Pipeline’s Robin).

Understanding the relationship between these two crudes is important because their relative prices reflect US reliance on foreign crude imports (priced relative to Brent) to meet refining needs versus domestic crude (priced relative to WTI). Over the past three years the US reliance on imported crude has declined as domestic production of crude from shale has increased. Energy Information Administration (EIA) data indicates that US crude imports declined by 2.3 MMb/d between June 2010 and the end of May 2013. Even though domestic production is increasing, the US is hardly energy independent yet. We still import over 7 MMb/d of crude including roughly 2.5 MMb/d from Canada that is effectively priced against WTI. That leaves about 4.5 MMb/d of “foreign” imports that are priced relative to Brent. Because most of the new US domestic production is light sweet crude oil, we expect imports of similar grade light sweet crudes at the Gulf Coast to reduce to a trickle by the end of this year. As light crude from the Bakken increasingly meets East and West Coast demand, light crude imports will be pushed out altogether. That trend has already had an impact on West African sweet crudes – once popular in Gulf Coast refineries and now no longer needed here. The remainder of US foreign crude imports is made up of medium and heavy crudes that are refined primarily on the Gulf Coast and the West Coast. These continued imports mean that US crude prices will remain connected to the international market for the present time. That means that the relationship between Brent and WTI will continue to be significant for US refiners.

The chart below shows the Brent (red line) and WTI (blue line) relationship over the past three years. The WTI discount to Brent that began to deepen in August 2010 resulted from a build up of crude inventory at the Midwest Cushing, OK trading hub. The inventory increase resulted from growing crude production in North Dakota and Western Canada overwhelming Midwest refinery needs and getting caught in Cushing because of inadequate pipeline transport capacity to Gulf Coast refineries. There has been some relief to the Cushing stockpile – noticeably after the reversed Seaway pipeline began to flow crude from Cushing to Houston in June 2012 at an initial 150 Mb/d and was expanded in January 2013 to carry as much as 400 Mb/d. And then in April 2013 the Magellan Longhorn pipeline (also reversed) began to flow 75 Mb/d from the Permian Basin in West Texas to Houston that would otherwise have ended up in Cushing. This last increase in crude “relief” capacity for Cushing appears to have convinced the market that WTI prices should not be discounted so heavily to Brent because the $/Bbl spread between the two crudes narrowed to single figures at the end of April and has remained close to that level since.

Source: CME Futures Data from Morningstar

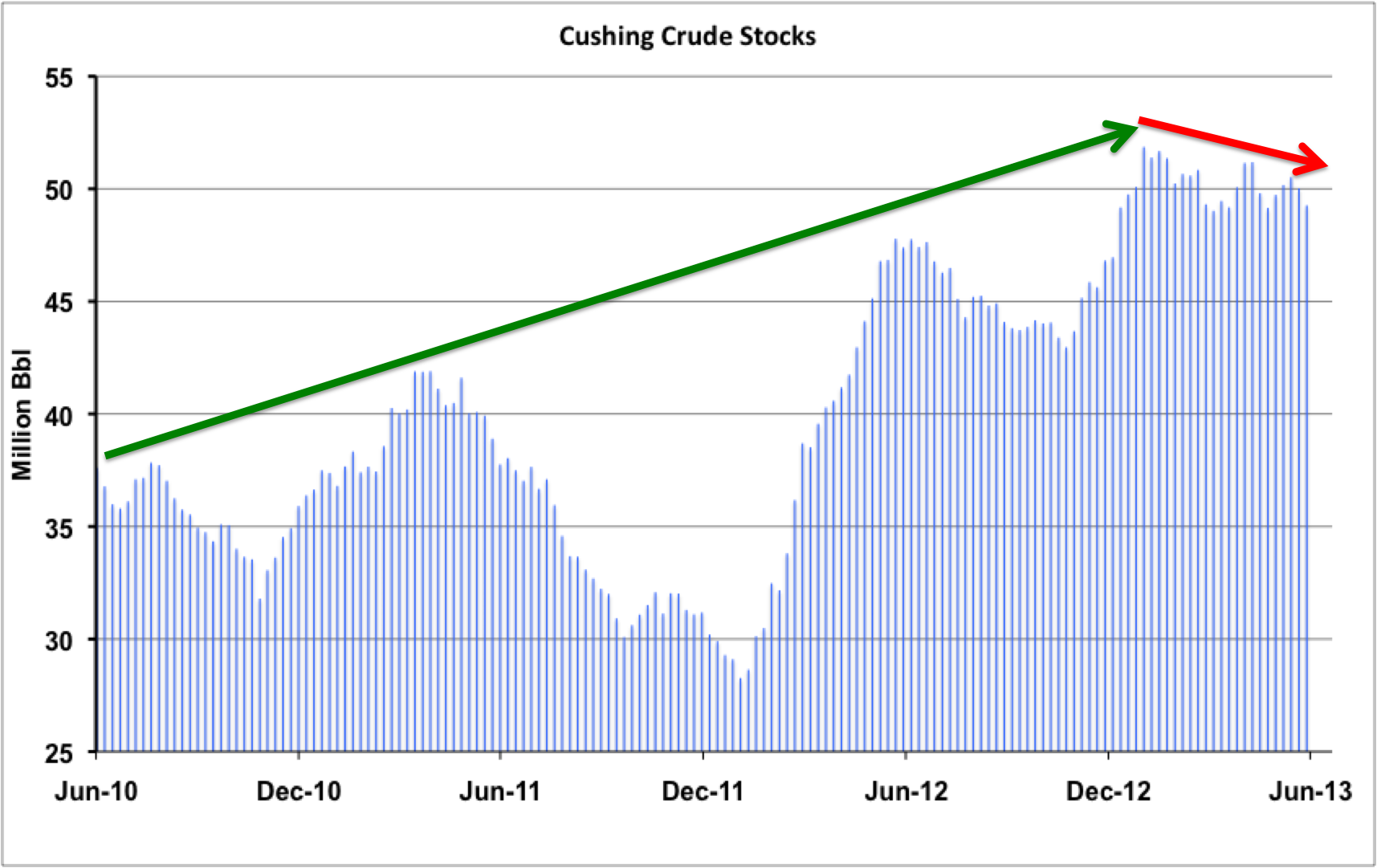

The implication of a narrowing WTI discount to Brent is that the supply logjam that caused the disconnect between the prices of these crudes is beginning to unwind. The first place to check that theory is to look at Cushing, OK crude stocks. The chart below shows Cushing stocks over the past three years. Generally speaking the Cushing stockpile has been on an upward trend such that every time stocks have been drawn down they filled back up again to new highs (green arrow on the chart). The signs are however that after reaching an all-time high of 51.6 MMBbl at the end of January 2013 they have leveled off and declined so far this year, with the past two weeks showing a drop off (red arrow on the chart). Given the volatile movements in stock positions over the period however it is still too early to call the end of the stockpile. It is true that pipeline capacity has opened up this year to move additional crude away from Cushing (e.g. the Longhorn pipeline as mentioned earlier) but the impact has not been conclusive. Next month (July 2013 Phase 1 of the Permian Express pipeline from Wichita, TX (in the Panhandle) will come online providing 90 Mb/d of additional capacity from the Permian Basin to Nederland on the Texas Gulf Coast. Magellan have stated that the Longhorn pipeline will ramp up from an initial 75 Mb/d to full 225 Mb/d capacity in 3Q, 2013 (i.e. in the next 3 months). These incremental increases in flows help to relieve Cushing but the stockpile is unlikely to be run down significantly until the Seaway twin pipeline comes online (+450 Mb/d) in 1Q 2014 along with the Keystone XL Gulf Extension (700 Mb/d).

Source: EIA Data from Morningstar

In the meantime some relief to Cushing should be afforded when the BP Whiting refinery comes out of its lengthy upgrade outage this month or next. That refinery in Indiana will then consume 250 Mb/d of heavy Canadian crude and relieve some of the weight of excess Canadian crude in Cushing tanks.

So we can’t credit a lower crude stockpile in Cushing with causing the WTI/Brent spread to narrow. But the fact is that despite the stockpile, increasing supplies of crude from the Eagle Ford, the Permian and from North Dakota are reaching the Gulf Coast. Eagle Ford crude is flowing to Houston via pipelines (Enterprise Eagle Ford Crude pipeline - 350 Mb/d and Kinder Morgan Crude and Condensate pipeline - 300 Mb/d). Additional Eagle Ford crude is reaching Houston or points further East on the Gulf Coast by barge from Corpus Christi (see We’re Jammin’). As we mentioned earlier, Permian Basin crude is bypassing Cushing now to reach Houston. And movements of crude-by-rail from North Dakota are reaching the Eastern Gulf Coast at St James (see The Bakken – St James Shuttle). All of this crude is light and sweet – much of it ultra light condensate from the Eagle Ford (see The Eagle Ford Condensate Challenge). The new crude flows are pushing out imports of light sweet crude regardless of the Cushing stockpile still being in place. In theory the fact that inland crude supplies are reaching the Gulf Coast to compete with Brent, should therefore mean that WTI prices rise towards Brent because domestic crudes are able to compete directly against imported barrels. But that is not what is happening.