Listen to Paul Simon’s “The Sound of Silence” and you hear the words of a teenager coming to terms with the disconnect between the world his parents promised and the real world yet to come. In the LNG market, there’s a similar generational divide. A business built on long-term contracts, rigid trade patterns, and the promise of substantial growth potential is being met with a more skeptical outlook, one in which a large amount of incremental LNG supply has been locked up but serious questions remain about LNG demand. As we discuss in today’s RBN blog, an entire generation of LNG supply is being built on the presumption of selling it for $10/MMBtu or more, but a shortfall in demand growth could leave it selling for considerably less. And if that happens … sunk-cost economics, here we come.

Join us at our historic 20th School of Energy!

School of Energy: Foundations is a two day, in person conference designed to help energy professionals better understand the forces shaping crude oil, natural gas, NGLs, refined products, and petrochemicals.

Attendees will learn from RBN experts, work with Excel based analytical models, participate in Q&As, and network with industry peers.

Build the foundation to better navigate volatile energy markets.

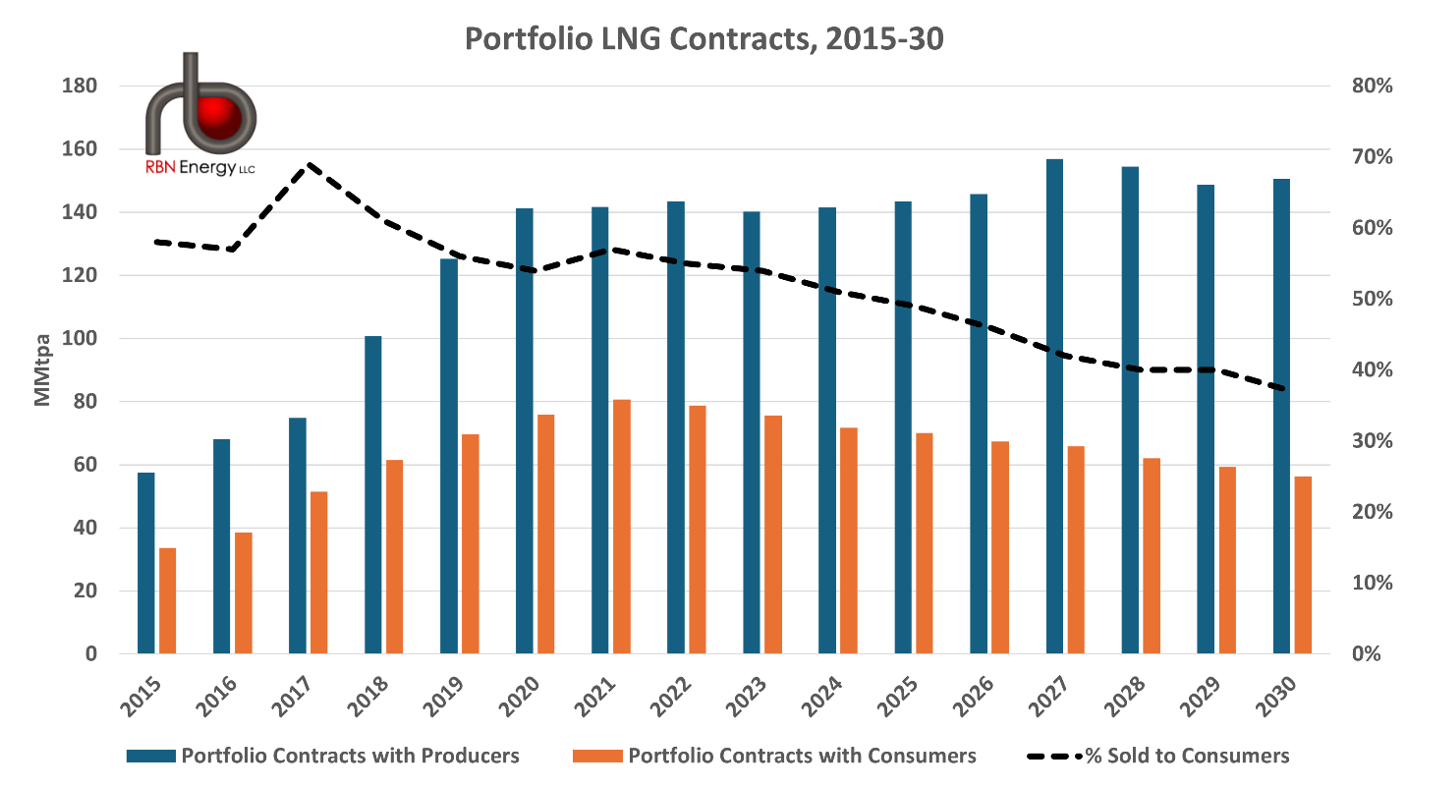

The enormous amount of LNG supply coming into the market in the mid-to-late 2020s is looking for long-term buyers … and looking and looking and looking. Not to get all existential, but the outlook for LNG demand is increasingly taking on the overtones of “Waiting for Godot,” the Samuel Beckett play: It’s out there, it’s coming, and it’s only a matter of time until it arrives. But like Godot, the consumers for all that LNG expected to come online in the next several years may prove elusive. The disconnect can be viewed through the lens of those who have contracted for LNG volumes. Although LNG portfolio contracts with producers (blue bars in Figure 1 below) are projected to climb from 141 million metric tons per annum (MMtpa) in 2024 to more than 150 MMtpa by 2030, the amount actually committed to consumers (orange bars) falls from 51% to 37% (dashed black line) over the same period. Part of this dichotomy may be attributable to the differing strategies of LNG portfolio players and gas consumers, with the former, up to this point, willing to accept the risk to lock in supply and global access while the latter, uncertain about their future needs, has been more inclined to cut shorter-term supply deals.

Figure 1. Portfolio LNG Contracts, 2015-30. Source: GIIGNL

About the song

“The Sound of Silence” was written by Paul Simon and appears as the sixth song on side one of Simon & Garfunkel’s debut studio album, Wednesday Morning 3 AM. A studio audition of the song led to the duo signing a record deal with Columbia Records in 1964. The song was originally released as a single in an acoustic version in October 1964 but failed to chart. In 1965 some radio stations started playing the song on the East Coast, leading to producer Tom Wilson to remix it, adding electric guitars, bass, and drums. The new version was released in September 1965 and went to #1 on the Billboard Hot 100 Singles chart. The success of the single led the duo to hastily record their second studio album titled, The Sounds of Silence, and include the new version on the LP. The song was also featured in the movie The Graduate and on the soundtrack album to the film. Personnel on the record were: Paul Simon (vocals, acoustic guitar), Art Garfunkel (vocals), Barry Kornfield (acoustic guitar), Bill Lee (acoustic bass), Al Gorgoni, Vinnie Bell (electric guitar), Joe Mack (electric bass), and Bobby Gregg (drums).

Wednesday Morning 3 AM was recorded at Columbia 30th Street Studio in New York City in March 1964 with Tom Wilson producing. The album was released in October 1964 and went to #30 on the Billboard 200 Albums chart. One single was released from the LP.

Simon & Garfunkel was an American folk-rock duo consisting of singer-songwriter-guitarist Paul Simon and vocalist Art Garfunkel. The duo met while attending elementary school together in New York City. As teenagers, under the name Tom & Jerry (named after a popular cartoon series in the 1950s), they had a minor success with the 1957 single “Hey Schoolgirl.” As Simon & Garfunkel, they released five studio albums, four live albums, 13 compilation albums, one soundtrack album, one EP, and 26 singles. They have won 14 Grammy Awards, a Grammy Hall of Fame Award, one Brit Award, and are members of the Vocal Group Hall of Fame and the Rock and Roll Hall of Fame. The pair have not performed together since 2010. Both have gone on to successful careers as solo artists. Paul Simon still records but retired from touring in 2018.

Comments

Today's blog was interesting and thought-provoking. Two comments:

1. The legend on Figure 2 doesn't appear to be correct, as one of the Big 3 producers (Australia) is not mentioned.

2. The blog focuses on the use of gas for power generation to the point that it ignores other potential LNG markets. If the author disagrees with the generally accepted view that LNG is going to be a very important competitor in the bunker fuel market, I would be interested in hearing the reasons for that view. But, the blog ignores the developing competition between oil products and LNG and that makes it difficult to accept the conclusions in the blog at face value.