Crude differentials in the Permian are getting squeezed. The spread between Midland and WTI at Cushing widened out to near $18/bbl at one point in 2018, when pipeline capacity was scarce. But that same spread averaged a discount of only $0.25/bbl in March 2019. Differentials between Midland and the more desired sales destination at the Gulf Coast are also in a vise. What gives? Production in the Permian continues to climb, but the rapid pace of growth we saw in 2018 has slowed down a bit lately, with fewer rigs in service and fewer new wells being brought on each month. More importantly, we’ve seen several new pipeline expansions and pipeline conversions come online in bits and bursts — in some cases, ahead of schedule — and this new chunk of pipeline space has compressed Midland pricing. In today’s blog, we begin a series on Permian crude takeaway capacity and differentials, with a look at the handful of new projects that have come online in the past few months and what has happened to Permian prices as a result.

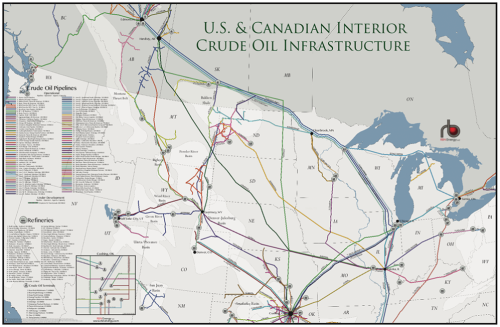

RBN's US & Canadian Interior Crude Oil Infrastructure Map features pipelines, refineries, and terminals that are new, existing, and under development from Canada to the Bakken Shale to Cushing.

It was only a matter of time before the crude oil market found a way to kill the price spread. It’s happened again and again. A few years back, pipeline takeaway capacity in both the Bakken and the Powder River Basin was limited, crude-by-rail was getting built out at an impressive clip, and traders were taking advantage of unique pipeline, rail, and trucking options to capture arbitrage opportunities on double-digit spreads. While producers were seeing low netbacks and weren’t happy, traders and end-market users were living the good life. Over time though, more than enough pipeline capacity got built out in those areas, spreads tightened, and most of the crude-by-rail and niche trucking opportunities were mothballed. Midstream companies saw wide price differentials, recognized the opportunity, built projects like the Dakota Access Pipeline, and the spread was dead.

That’s similar to what we’ve seen materializing in the Permian Basin over the past six months or so. In September 2018, with production quickly rising and pipeline capacity scarce, the Midland-Cushing spread widened out to minus-$18/bbl (blue line and dashed red oval in Figure 1) and the Midland-Magellan East Houston (Midland-MEH) spread widened out to minus-$24/bbl (orange line and dashed red oval). Spreads at those levels supported all kinds of movements, from Permian pipeline transportation to Cushing and the Gulf, long-haul trucking barrels to Eagle Ford pipelines — even a few crude-by-rail projects in West Texas had legs for a couple of months. Since then, however, those spreads have diminished substantially. At the end of January, we discussed how the Permian had become a tighter market; production disruptions in the area had slowed the growth and forced traders to scramble to find barrels. At that time, we saw West Texas barrels actually trade at a premium to WTI at Cushing, something that had seemed impossible only a few months earlier. Since the end of January, the Midland-Cushing differential has remained within a narrow band, with Midland trading at times just above or just below WTI at Cushing and averaging a discount of minus-$0.15/bbl over the course of February and March.

About the song

"Hard Hat and a Hammer" was written by Alan Jackson and was the second single from his 14th studio album, Freight Train. The LP was produced by Keith Stegall and released in March 2010. The song includes the sound of Jackson hitting an anvil that once belonged to his father, who passed away in 2000. It reached #17 on the Billboard Hot Country Songs chart. Freight Train reached #7 on the Billboard Top 200 Albums and #2 on the Top Country Albums charts.

Alan Jackson is an American country singer and songwriter. He has sold more than 60 million records worldwide, and has had 26 #1 country singles that he wrote or co-wrote. Alan has released 17 studio albums, two gospel albums, two Christmas LPs, one live album, and 13 compilation albums. He has won 15 American Country Music Awards, 15 Country Music Association Awards, two Grammy Awards, and one Billboard Music Award. Jackson still records and tours to this day, and is currently on his “Alan Jackson Tour 2019.”