The Texas natural gas market is rapidly evolving, in large part due to burgeoning Permian production but also due to gas production gains in East Texas driven by strong returns on new wells in the Haynesville and Cotton Valley plays. Most of this supply growth is looking to make its way to the Gulf Coast, where close to 5 Bcf/d of LNG export capacity is operational and plenty more is under construction. The combination of fast-rising supply and demand is straining the existing gas pipeline infrastructure across Texas, creating the need for more capacity. The Permian has been grabbing the headlines for its extreme takeaway constraints and depressed, even negative supply-area prices, and all eyes are trained on the announced pipeline projects that will eventually provide relief to the region. But pipeline constraints also are developing between the Haynesville and the Texas coast. Today, we discuss the latest solution for the intensifying Haynesville-area supply congestion.

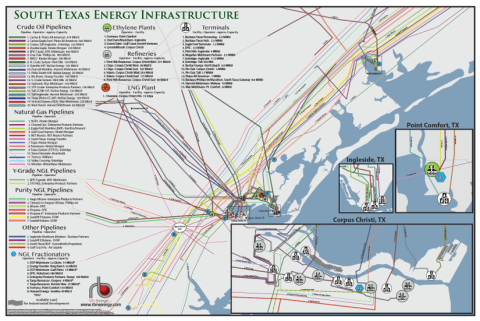

RBN Energy’s South Texas Energy Infrastructure Map brings together all the pieces of the critical and complex puzzle of the greater Corpus Christi region. Spanning from Point Comfort, TX to Corpus Christ, TX and south of the Agua Dulce natural gas hub, the map details the processing, transportation and export facilities in RBN Energy’s classic clear, concise and easy to comprehend style.

While most of our recent blogs related to the Texas gas market have focused on the Permian, an interesting dynamic is also emerging on the other side of the state, in the gas fields of East Texas. As we discussed in What Are The Chances last August, after facing steep declines earlier this decade, gas production from the Greater Haynesville Shale producing region — including the Haynesville, Bossier and Cotton Valley formations that straddle northwestern Louisiana and East Texas — have raced higher over the past couple of years. The play has attracted renewed interest and focus from a new slate of players who have steadily improved drilling efficiencies and economics there. Unlike the Permian, where most of the gas production growth is being driven by volumes associated with oil drilling, East Texas production is being driven almost entirely by dry gas economics, which historically haven’t been attractive enough in the Haynesville at the kind of gas prices we’ve seen in the last few years — in the vicinity of $3/MMBtu. However, enhanced drilling techniques and a focus on the region’s “sweet spots” have spurred on Greater Haynesville production growth, with volumes climbing from less than 6 Bcf/d in late 2016 to about 10.5 Bcf/d in the past couple of months — surpassing the monthly average peak seen in late 2011 (maroon and blue layers combined in Figure 1). That includes the Texas side of the Haynesville (maroon layer), where volumes now top 3 Bcf/d, about 400 MMcf/d above their 2011 peak.

About the song

"Easy Livin'" was written by Uriah Heep keyboardist Ken Hensley, and was the second single off of Uriah Heep's 4th studio album, Demons and Wizards. Released in September 1972, the song rose to #39 on the Billboard Hot 100 chart, making it the only song that cracked the top 40 in the U.S. for the band. Hensley, who wrote most of Uriah Heep's popular songs, said that he wrote the song in about 15 minutes, after a discussion with his bandmates about the misconceptions most people have that the life of a rock-and-roll band is always easy. The words "easy" and "life" stuck in his mind, and he wrote the song around that foundation.

Demons and Wizards was recorded at Lansdowne Studios in London in March-May 1972. The Gerry Bron-produced album was released in May 1972, and went to #23 on the Billboard Top 200 Album chart. It was certified Gold by the Recording Industry Association of America. Personnel on the record were: David Byron (lead vocals), Mick Box (lead guitar), Ken Hensley (keyboards, backing and co-lead vocals, guitar, percussion), Gary Thain (bass), Mark Clarke (bass), and Lee Kerslake (drums, backing vocals, percussion).

Uriah Heep is a British rock band formed in London in 1969, and were performing under the name "Spice" until keyboardist Ken Hensley joined the group in 1970, when they changed their name to Uriah Heep. Hensley, formerly of the group "Toe Fat," which had already released their debut album before his departure, was brought into the group to expand their sound with a Marshall-fueled overdriven Hammond B3 sound that was popular at the time with Jon Lord in Deep Purple, Mark Stein in Vanilla Fudge, and Vincent Crane in the Crazy World of Arthur Brown. Hensley would later recruit drummer Lee Kerslake into Uriah Heep, which completed the lineup for the most popular and successful period for the band. Kerslake had previously played with Hensley in Toe Fat, and before that in the mid-60's British band "The Gods," which also included future John Mayall and Rolling Stones guitarist Mick Taylor, and future Toe Fat and Jethro Tull bassist, John Glasscock.

Uriah Heep have released 25 studio albums, 20 live albums, and 32 singles during their career so far. They have had 25 band members pass through their ranks to date. Led by founding member, guitarist Mick Box, the band still records and tours to this day. "Easy Livin'" is still the most requested and popular song at Uriah Heep live shows.