By: Eric Penner

A lot of natural gas storage follows a time honored pattern – put gas in during the summer and take it out during the winter. But it is getting much more complicated than that. Developments in natural gas production – particularly in the Appalachian (Marcellus) region will be driving big changes through the gas storage business. Today we pick up on a blog series we started last month to examine the two fundamental value generating gas storage mechanisms, and how they match up with the physical characteristics of storage facilities.

In Catch a Hydrocarbon, Put it in Your Cavern, Save it for a Wintry day we started this blog series by examining how storage acts as the ‘flywheel’ for the natural gas market, how much storage there is out there, where it is located, and some basics about the geology of storage. We use the term geology because almost all natural gas is stored underground, either in depleted reservoirs (old oil and gas fields), aquifers (geological structures that use underground water to trap gas), and salt caverns (huge underground caves ‘washed out’ of a salt formation with water). These different types of storage facilities are used in quite different ways to provide value to customers. And that means that there are big differences in how the various kinds of storage facilities are priced in transactions between the seller of storage services and the buyer of those services.

One more introductory comment before we get into this discussion of storage value. Who is the seller and who is the buyer? Well, it depends. Sometimes it is a utility that uses storage the old fashioned way. They store gas in the summer to meet the requirements of their residential and commercial customers in the winter. In this situation, most likely the utility both owns and uses the storage asset, so there is really no price associated with the storage capacity itself. The value of the storage is imbedded in the utility’s overall service (regulated by a state Public Utilities Commission) provided to its customers. More interesting to our discussion here is the ‘merchant’ case where a storage operator owns the storage facility and leases capacity to a company that needs the service for some business reason – perhaps to manage the gas supply for an industrial facility or power plant, or perhaps to provide a tool to be used in natural gas trading strategies. In this latter case, the operator ‘sells’ or leases its capacity to a storage customer, based on a mutually agreed price – what the customer pays the operator for capacity and the associated services (rate of injection, rate of withdrawal, length of time that the gas can be held in storage, etc.)

How Much Should Natural Gas Storage Be Worth?

As with any transaction, the fundamental question is ‘What’s the right price?’, and to that end, what basis should be used by the buyer and seller to determine the acceptability of a given price? In our personal lives, for the most part, we internalize this acceptability criteria in the sense that we develop an intuitive notion as to whether a given product (say an iphone) is subjectively more or less valuable than the asking price. In the same way, when asking how storage is priced, we must first answer the question – how much is it worth?

At the most basic level, the answer is pretty simple. The value of storage depends upon the degree to which the price of natural gas will be higher or lower at some point in the future. Unfortunately we don’t know what the future price will be (if we did, we wouldn’t be writing blogs about it). That means that a storage decision depends instead on whether there is a credible expectation that natural gas can be purchased today, stored (for the price of that storage) and the sold for a profit at some point in the future. Unfortunately accurate expectations regarding future natural gas prices rely on so many factors that it is virtually impossible for any single person or firm in isolation to determine forward prices with any degree of certainty. Thankfully though, we have a lot of help from the futures market. It might not predict what the future price will be, but it does give us a good indication of what buyers and sellers think about future prices at any point in time. In a way, looking at CME/ NYMEX forward prices makes anyone an instant (but subject to quick expiration) expert on natural gas pricing. At one level the valuation of storage boils down to simply the difference in the current spot price and the expected future spot price, the forward price.

Let’s take a moment to think about an implication of the previous statements; the value of natural gas storage relies entirely on the variation in price of natural gas over time. That means that without price variation (i.e., if price is constant), there is no inherent economic benefit to storage in our ‘merchant’ case. Of course, that is far from reality. In fact, there are two kinds of price variation which contribute to the value of storage. For reasons that we hope will become obvious we will refer to these two sources as the Signal and the Noise.

The Signal and the Noise (intrinsic versus extrinsic)

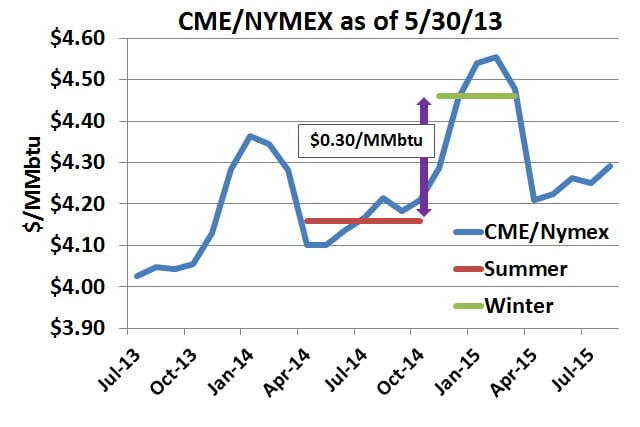

The Signal is the variation in prices caused by seasonal fluctuations in demand which rise in the winter and fall in the summer. We call it the Signal because it is a strong consistent indicator of annual price variation. This seasonal valuation, also known as the “intrinsic” value of a storage facility, is quantified by the average summer/winter forward price differential for some future period. (Note that in the gas world, the summer ‘injection’ is usually assumed to be the seven months between April-October while the winter ‘withdrawal’ season is the five months between November–March.) For example, as shown in Figure #1 below, on May 30th 2013 the average forward summer 2014 price was $4.16/MMbtu while the average forward price for the winter of 2014 - 2015 was $4.46/MMbtu. . The difference between these two prices $0.30/MMbtu indicates the intrinsic value of storage between these two time periods.

Figure #1 –

The other source of variation, the Noise, is the daily fluctuations in natural gas pricing which at times seems to have no rhyme or reason. This value, called the ‘extrinsic’ value of storage, is derived from the inherent volatility within the market. Essentially the extrinsic value comes from the same source as intrinsic value, the ability to sell gas at a higher price after some period that it is held in storage. The difference between the two is the length of time over which the price variation takes place, for intrinsic value it is long (i.e., bi-annually) and for extrinsic it is very short (i.e., one or more days). To capture the extrinsic value from these daily price fluctuations the storage facility must be able to switch from injection to withdrawal and back very quickly, often in a matter of hours to exploit the volatility. Facilities well positioned to capture this value inject (buy) gas when the price falls and withdraw (sell) when the price rises.

Quantifying the extrinsic value of storage relies on financial pricing models similar to those used to calculate the price of a financial option contract. (Business school grads might remember something called Black-Scholes, a mathematical model of option pricing.) A person can spend years attempting to understand the mathematical arguments used to justify an options pricing model (Myron Scholes won a Noble Prize for his work) but in essence it depends on a measure of the current volatility-how much the price bounces around.

Volatility in the context of natural gas prices is a measure of the dispersion of forward prices or, put simply, a measure of the distance between the maximum and minimum forward price for gas over a short time period. Obviously, as the max and min price get farther apart the value of the possibility of injecting (buying) and the min and withdrawing (selling) at the max increases.

As the level of volatility in price increases, the likelihood that large changes in natural gas price will frequently occur also increases. Capturing extrinsic value is dependent on these large price changes, so naturally as the probability of frequent large price changes increases so does the extrinsic value.

There are a number of techniques to measure historical price volatility. The most common technique starts by determining the percent change in price from one trading day to the next. The calculation then takes the standard deviation of that percent price change over some sample period of time. That value is then annualized by multiplying that standard deviation by the average number of days in a typical trading year. Don’t freak out. If you really want to understand this particular calculation see Investopedia Option Volatility: Historical Volatility. But if you just want to get the big picture, see the graphs below. Figure #2 shows a period of high natural gas price volatility back in 2009. See how much the price (the blue line) bounces around. Our measure of volatility (the orange line) ranges between 70% and 110%. That’s high. Figure #3 shows a period of low gas volatility in 2011. The price moves around very little, and our measure of volatility ranges between 30% and 40%. For natural gas that’s low. The value of extrinsic value is primarily a function of this volatility, and can be calculated using that Black- Scholes model described above. To insure our reader’s sanity, we won’t go into that math today.

Comments

Eric,

Thank you for the great article. I have a question regarding the extrinsic value of the storage. The article suggests that it should be valued in a similar fashion to financial option models. I can see how storage could be deemed as similar to a call option in that it offers the potential to store now and sell later at a (hopefully) higher price. My concern is that there seems to be downside risk with the storage option (prices could drop forcing a sale at a price lower than the price when the gas was injected) that isn't present in a financial option. My understanding was that the value of a financial option increases with volatility because of the asymmetrical payoffs. (Ie being long a call option offers unlimited upside with downside risk limited to the premium paid). Here the downside risk does not seem to be limited so would the valuation methodology not need to change?

Thanks again!

In reply to Quantifying Extrinsic Value by marmac marmac

Thank you for your question. Absolutely right the key word in the sentence from the blog “…pricing models similar to those used to calculate the price of a financial option contract” is “similar”. In fact, there are a number of differences in the models used. In regard to your specific question, there are ways to manage that downside price risk. For example, if the ‘option’ is expected to capture intra-month price volatility (an uptick in spot prices over the next few days), it is always possible to purchase and inject gas at the same time a forward futures position is placed. Assuming the market is in contango, that would lock in some upside when the transactions are placed. Then if short term volatility kicks up, the physical position can be sold and the financial position reversed. If spot prices decline, the physical can be rolled and offset against the forward futures position. There are many other mechanisms that are used to manage real life storage positions, with some analysts making a life’s work out of it. Our intent in the blog was only to make an introduction to the concepts. Thanks again.