The gasoline market has become highly regionalized with the country apparently divided into areas of feast and famine. Shortages, low margins and declining refinery capacity have plagued the Northeast and California. Increased gasoline exports have rewarded Gulf Coast refiners. Midwest and Rocky Mountain refiners have profited from strong refining margins. Meantime gasoline consumption is falling across the country just as new US crude produced from shale basins – which just happens to be rich in gasoline blending components -- starts to reach coastal refining centers. Today we look at how the new crude streams might impact regional gasoline markets.

Northeast Gloom

As we reported earlier this year, East Coast refineries have been feeling the pinch from lower refining margins (see Don’t Let The Sun Go Down on Me – East Coast Refining Part 1). Refiners have faced higher costs for imported crudes priced against Brent that has traded at a $20/Bbl or higher premium to cheaper US and Canadian crudes. Those crudes are plentiful in the Midwest but until recently only trickled to the East Coast because of limited transportation options. The related closure of a number of refineries in the region due to lower margins led to fears of product shortages in July 2012. That crisis was averted when the Carlyle private equity group reopened the former Sunoco Philadelphia refinery in September and Delta Airlines purchased the Trainer refinery to keep that one open. Gasoline imports are still necessary to maintain adequate supplies to the Northeast however, because of constraints on refined product pipelines running from the Gulf Coast to the Northeast and Jones Act shipping restrictions (see The Sea and Mr. Jones).

There have still been occasional gasoline shortages this summer in the Northeast. We reported at the end of September on a NYMEX gasoline futures delivery squeeze in New York caused by refinery outage fears and rumors of product shortages (see Do We Need a New Gasoline Alley?).

California Suffering

California gasoline refiners suffer from a unique product blend requirement that is more expensive to produce and not a fit for any other market. The California gasoline market has been insulated from the rest of the US since the California Air Resource Board (CARB) began setting vehicle emissions standards in the 1970’s. (California’s gasoline market is a blog topic all of its own – its on the list). Today’s CARB regulations require refiners to supply a customized gasoline blend to meet stricter air pollution controls than the federal Clean Air Act “RVP” and reformulated gasoline specifications (see Regulatory Gas Pressure Party). As a result of the stringent CARB regulations, refiners in the Golden State are threatening to leave the market (Valero is reportedly trying to sell its two refineries in the State, BP just sold its California refinery). Because of the unique CARB gasoline specifications, supplies can run short quickly if there are refinery problems. Earlier this month (October 2012) a power outage at an Exxon refinery in Torrance followed an earlier fire at the Chevron Richmond refinery that reduced capacity in August. The result was shortages that spiked gasoline prices over 50 cents a gallon in a week.

On top of the CARB restrictions, Californian refiners are paying higher crude prices and suffering lower margins just like their colleagues in the Northeast. With no existing pipeline capacity to deliver new lower priced crude production from Canada, the Rockies or North Dakota to California, refiners are still paying premium prices for their crude based on international crude benchmarks.

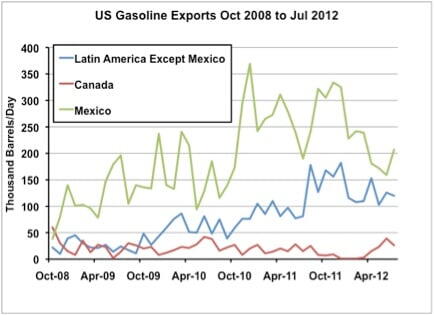

Gulf Coast Boom

We have previously covered the surge in US Gulf Coast diesel production in response to healthy diesel crack spreads over crude (see Gulf Coast Diesel Crack Habit Part I and Part II). Much of that production growth has been exported to Latin America and Europe. At the same time, there has been a similar increase in US gasoline exports. The chart below shows US gasoline exports over the past three years. The largest gasoline destination in that period has been Mexico (green line) that has at times imported more than 350 Mb/d and has consumed over 150 Mb/d since October 2010. Aside from Mexico, Canada is the largest importer of US gasoline – much of it being exported up the East Coast from the Gulf. Over the same period a lot of gasoline exports have gone to other Latin American countries (blue line on the chart) including Venezuela, Argentina, Chile and Brazil and a number of Central American destinations.

Source: EIA Export Data from Morningstar

High gasoline and diesel exports are helping Gulf Coast refiners maintain healthy margins even though they are currently paying higher prices for their crudes that are still priced against international grades linked to Brent.

Midwest and Rockies Margin Party

For gasoline refiners, the Midwest has been the sweet spot. While refiners on the East and West Coast have suffered low margins caused by high crude costs, their counterparts in the Midwest (PADD 2) and the Rockies (PADD 4) have been luxuriating in a flood of cheap crude. There are two reasons. First much of the new US domestic production is occurring close to these regions - in the Rockies and North Dakota. Second the production boom in North Dakota and Canada has flooded the market with more crude than Midwest refiners can consume. The lack of efficient infrastructure to get the excess barrels to coastal refining centers has caused Midwest crude prices to trade at a $20/Bbl or higher discount to the prices coastal refiners pay for their crude. Although Midwest gasoline demand like that across the country has been stagnant (we will get to that in a moment) refined product prices have held up close to national levels and since refiners are getting their crude at a discount, refining margins have been very attractive.

Gasoline Demand

Whatever the refinery economics, US domestic gasoline consumption is falling today and has been doing so for the past five years. The chart below shows how apparent demand for gasoline (see No Apparent Demand for the calculation) this summer (blue line in the chart) was lower than the previous five year average (pink line). A lot of that reduced demand is due to government regulation that replaced up to 10 percent of gasoline with ethanol (see A Market of Contradictions) and increased Federal CAFE auto fuel economy standards. In addition US drivers have reduced their gasoline consumption since the recession and usage does not appear to be picking up again.