The natural gas trading market has been getting a lot of attention lately and not in a good way. A couple of weeks ago the Wall Street Journal published two articles describing the fact that traders have started to reduce their presence in natural gas storage. At about the same time, Oneok, once a big player in energy services shut down its operation that had used natural gas storage and pipeline transportation capacity to provide those services to the industry. With gas production still coming on strong, more gas being used for power generation and the possibility of serious LNG exports on the way, what’s the problem? Today we look deeper into turmoil in the natural gas markets.

A lot of the problem has to do with the value of storage. In our most recent posting in this blog series, Come on, Feel the Noise: Natural Gas Storage - The Signal and the Noise we learned that the value of storage relies almost entirely on price variation within the forward and spot markets. Seasonal or “intrinsic” value is derived from the price spread between summer and winter forward prices. The other driver of value – called extrinsic - is derived from daily price swings, or volatility, in the spot price.

While there are a lot of nuances in the business of extracting value from storage capacity, the basic notion is pretty simple – buy gas, store it for a while and sell it for a margin – hopefully more than the cost of storage. But for that to work, there must be some minimal level of volatility in the market price for natural gas. No volatility, no opportunity for margin. No margin, no value creation. No value, no business.

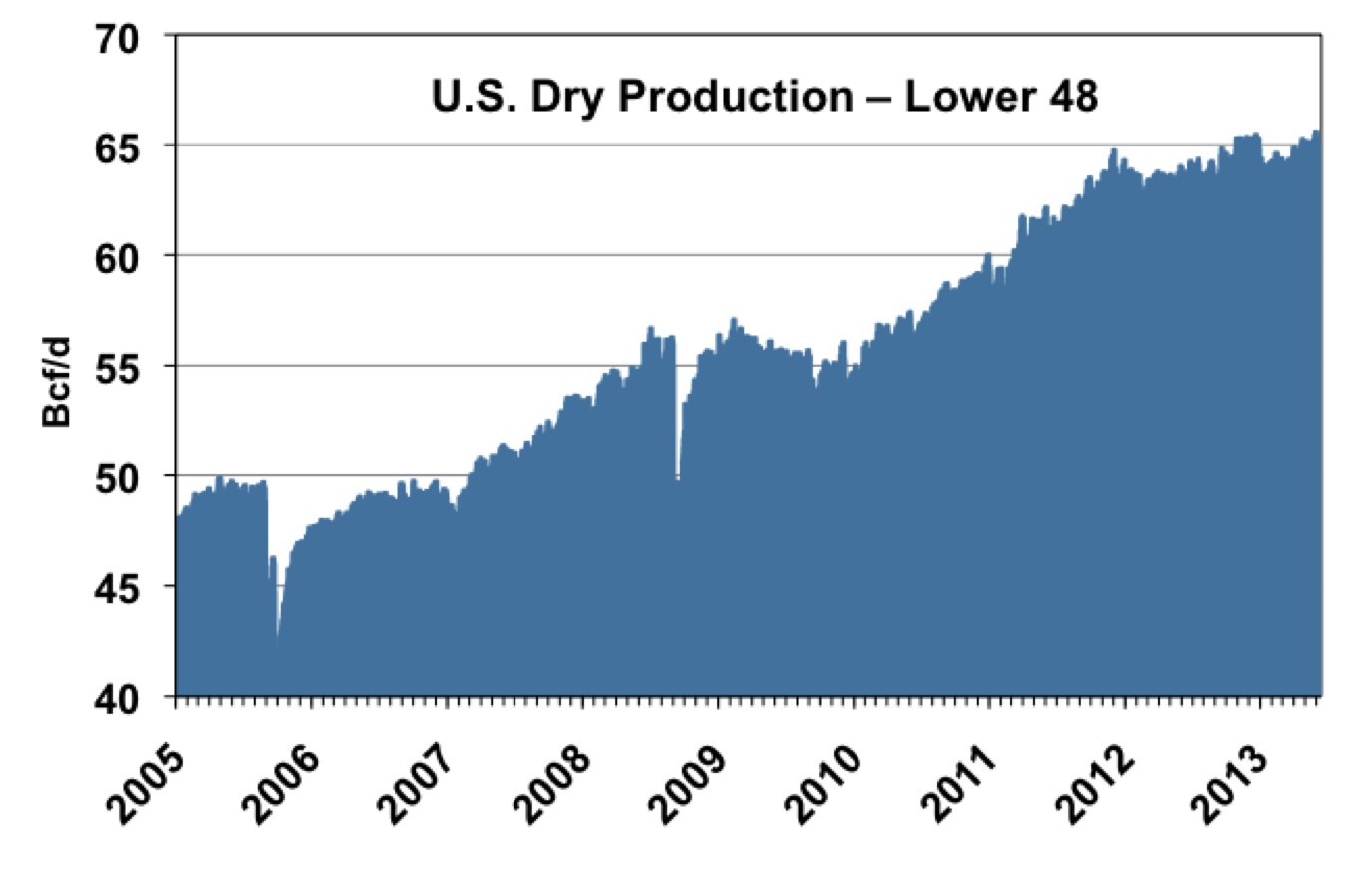

The culprit that has spoiled the storage party is that darned shale gas production. Lower 48 dry gas production (the U.S. Energy Information Administration (EIA) term – total marketed production minus extraction loss) has been on its well-publicized tear for the past eight years, increasing about 35% since 2006 and putting a huge damper on seasonal and daily price swings (see Figure #1 below).

Figure #1: U.S. Dry Production; Source – Bentek Energy

Stuck in the Doldrums

There is just so much production that supply hiccups that would have been a problem in the pre-shale era are not that much of a problem anymore. There seems little risk that there won’t be enough gas stored away in the summer injection season to meet winter demand. In fact, in recent years the concern has been that there might not be enough storage capacity to squirrel away all that summer supply.

And those short term price blips have also been smoothed out, since it seems that there is always more than enough supply to handle any short term spike in demand. Clearly the increase in production that the market has experienced over the past five years has reduced the amplitude of the summer winter price spread “Signal” and filtered out the “Noise” of daily price variation almost completely – the terms we coined in last week’s blog. Accordingly, as this price variation attenuates, the value of storage and therefore the margins it can generate shrink. This leaves commodities trading desks bored and looking for more volatile markets while storage operators are feeling the pinch as their margins shrink.

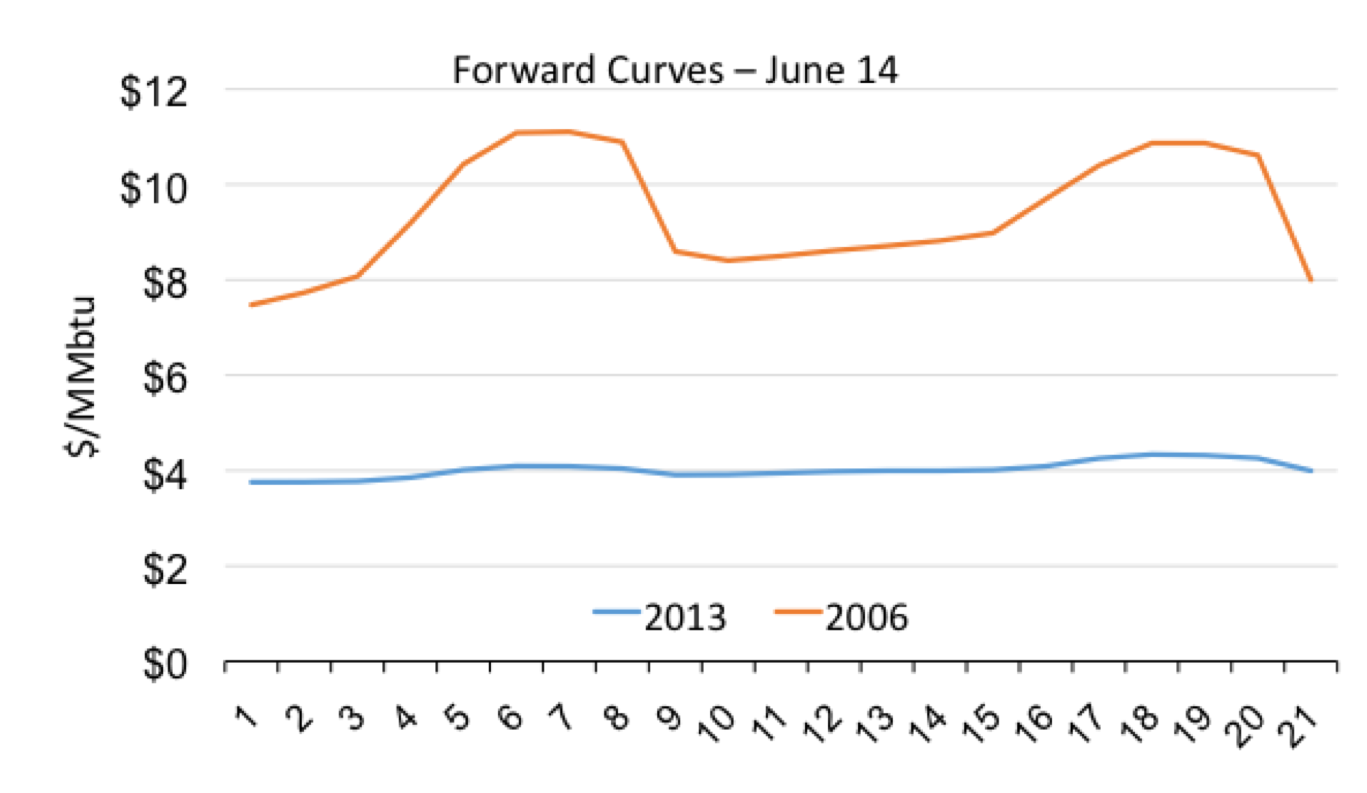

Let’s put that in the perspective of the forward curve. Figure #2 below tells that story. A few years ago back in the heyday of gas storage in 2006, the natural gas forward looked like a rollercoaster – with a differential of more than $2.50/MMbtu between July and January each year. Compare that to the forward curve last Friday, June 14, 2013. Flatter than a pancake. Only a $0.35/MMbtu differential between July and January each year. So it is certainly not hard to see why seasonal (intrinsic) storage no longer yields the profitability it did a few years back.

Forward Months

Figure #2: NYMEX/CME Natural Gas Forward Curves June 14 – 2006 and 2013 (click to enlarge)

About the song

"Bright Lights, Big City" was written and first recorded by American bluesman Jimmy Reed in 1961