Is the glass half-full or half-empty? The answer to that age-old question usually indicates whether a particular situation is a cause for optimism or pessimism. That question is particularly appropriate when trying to place in perspective the cyclical movement of the earnings and cash flows of U.S. exploration and production (E&P) companies, including returns that have steadily declined with commodity prices over the last year. In today’s RBN blog, we analyze Q2 2023 E&P earnings and cash flows and provide some perspective on the past and future profitability of U.S. oil and gas producers.

The NATGAS Appalachia weekly report provides the data and insights to monitor the northeast natural gas market’s twists and turns and identify the risks and opportunities along the way, including tracking supply-demand trends, outbound capacity and their impact on takeaway pipeline utilization, and regional prices.

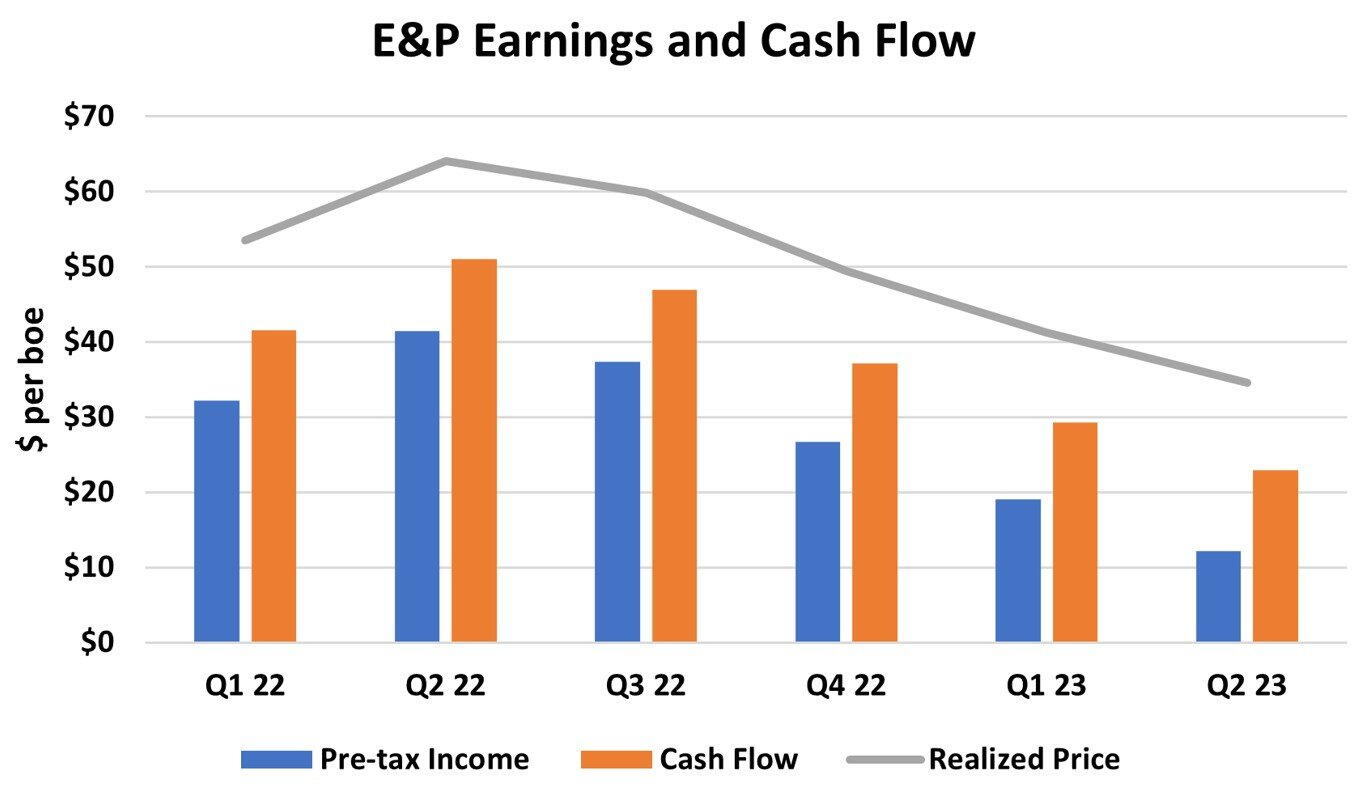

In Q2, earnings and cash flows for the 42 U.S. E&P companies we cover declined for the fifth consecutive quarter to $16.7 billion ($12.18/boe) and $31.4 billion ($22.95/boe), respectively. The results, a two-year low, essentially matched the $12.29/boe profit and $22.95/boe cash flow recorded in Q1 2021, when oil and gas producers were just beginning to recover from the market shocks of COVID. From a short-term perspective, the results of the recent quarter look like cause for concern. But remember that the song title we used in our review of Q1 2021 earnings was Walking on Sunshine — relative to the previous quarters, E&P results were great. That quarter marked a dramatic turn in fortune as the industry recovered from $84 billion in first-half 2020 losses after the onset of the pandemic. It also represented the highest pre-tax earnings in the last decade, surpassing the $10.58/boe recorded in 2014, when oil prices topped $100/bbl. Cash flow was also the second highest in the last decade, topped only by 2014.

The historic results in Q1 2021 were not only a cause for celebration, but they also kicked off a stretch of extraordinary growth in returns triggered by soaring oil prices and stringent financial discipline. As shown in Figure 1 below, pre-tax income (blue bars) and cash flow (orange bars) peaked in Q2 2022 at $41.48/boe and $51.02/boe, respectively. But this golden age for E&Ps that we described in Camelot didn’t last. Realized prices (gray line) began to retreat in the second half of 2022, with the decline steepening in the first half of 2023, mostly because of plunging natural gas prices. The average WTI oil price in Q2 2023 was $73.75/bbl, down 32% from $108.78/bbl in Q2 2022, while the average Henry Hub gas price plummeted to $2.33/MMBtu, down 69% from $7.47/MMBtu over the same period. (For a table showing additional comparisons to previous quarters, click here.)

Figure 1. E&P Earnings and Cash Flow, Q1 2022-Q1 2023. Source: Oil & Gas Financial Analytics, LLC

About the song

“Bottoms Up” was written by Brantley Gilbert, Justin Weaver and Brett James. It appears as the third song on Brantley Gilbert’s third studio album, Just as I Am. The song references kegs, Daisy Dukes, tailgates on pickup trucks, and partying. The video for the song presents Gilbert as a bootlegger/gangster, strapped with two 9mm pistols, surrounded by flapper girls while he travels in a resto-mod 1935 Ford followed by a 1928 Ford Model A with two Tommy gun-armed escorts riding shotgun on the running boards. They arrive at a party where Gilbert's band is dressed in all the accoutrements of a late-eighties metal band. The video ends with gunfire and the question ... who shot who? Released as the first single from the album, “Bottoms Up” went to #1 on the Billboard Hot Country Songs and #20 on the Billboard 200 Singles charts. It has been certified 7x Platinum by the Recording Industry Association of America (RIAA). Personnel on the record were: Brantley Gilbert (lead vocals, acoustic guitar), J. Bonilla, David Huff (programming), Eric Darken (percussion). Jess Franklin (dobro, electric guitar), Paul Franklin (steel guitar), Wes Hightower (backing vocals), Dann Huff (bouzouki, acoustic guitar, electric guitar), Elliot Huff, Chris McHugh, Ben Sims (drums), Charlie Judge (keyboards), Gordon Mote (piano), John Merlino (electric guitar), Jonathan Waggoner (bass), and Jonathan Yudkin (strings).

Just as I Am was recorded in 2013-14 in Nashville and produced by Dann Huff and Scott Borchetta. Gilbert wrote or co-wrote all of the songs on the album. Released in May 2014, it went to #1 on the Billboard Top Country and #2 on the Billboard 200 Albums charts. It has been certified Platinum by the RIAA. Four charting singles were released from the LP. A remix of “Bottoms Up,” featuring Atlanta rapper T.I., was included on reissues of Just as I Am.

Brantley Gilbert is an American country music singer, songwriter, and record producer from Jefferson, GA. He signed to Warner Chappell Publishing as a songwriter in 2007. He released his debut album, A Modern Day Prodigal Son, in 2009. He has released six studio albums, and 17 singles. Four of his singles went to #1 on the country charts. He has won two ACM Awards, two CMA Awards, and one American Music Award. Gilbert continues to record and tour and will be the opening act on Nickelback’s Get Rollin’ Tour beginning in September 2023.