Recent third quarter earnings reports from US refiners have reflected lower refining margins squeezed by higher feedstock prices for inland crudes like West Texas Intermediate (WTI) rising to the same level as coastal crudes like Light Louisiana Sweet (LLS) while product prices stood still. In the past two weeks domestic crude prices have fallen below $100/Bbl in the face of a Gulf Coast supply glut. But despite lower crude costs, refinery margins have continued to weaken. The primary culprit has been sharply falling gasoline prices. Today we review what Gulf Coast refiners could do to improve margins.

RBN Energy analysis of refining margins uses a simplified approach known as “crack spreads” to identify overall trends in refinery performance rather than getting into more complex refinery economics. Recall that the term “crack” does not refer to something a wayward crude trader might ingest in the bathroom but rather to breaking down or “cracking” crude oil. The term “spread” means the difference between the sales price of the refined products and the raw material cost of crude i.e. the refining margin. A 3-2-1 Crack spread for example approximates a refinery that produces two barrels of gasoline and one barrel of diesel for every three barrels of crude input. In other words the refinery yield is two-thirds gasoline, one-third diesel (see Bakken Buck Starts Here Part IV). If you are a registered RBN member (free) you can follow the 3-2-1 crack spread on the daily updated RBN Spot Check section of our website.

Back at the start of August we looked at how the NYMEX 3-2-1 crack spread (based on NYMEX futures contracts) cratered 56 percent between March and August this year (2013) after the NYMEX benchmark West Texas Intermediate (WTI) crude discount to Brent narrowed close to parity in July 2013 (see Money For Nothing (I Need My 3-2-1)). WTI prices had previously been discounted to Brent for almost three years as a result of crude supply disruption in the Midwest (for chapter and verse on that saga see Strangers in the Night). The 3-2-1 crack spread was squeezed when rising WTI crude prices this year were not matched by refined product prices that stayed more or less static. As a result refiners paid more for their crude but didn’t get higher revenues from refined product sales - reducing their margins.

Two months ago in September we looked at the impact of the Syrian crisis on refining margins at the US Gulf Coast (see War Huh What is it Good For?). Back then the threat of war caused international crude prices to increase temporarily, pulling US crude prices along with them but leaving product prices behind. That put further downward pressure on refinery margins – showing how refiners are frequently impacted by events beyond their control.

Any time that crude and refined product prices get out of whack – and it happens quite often - refiners experience volatile margins. Sometimes it works out in refiners’ favor. Over the past three years the WTI discount to Brent crude meant that refiners with access to lower priced “advantaged” crude (for example refineries in the Midwest) were able to enjoy very favorable margins, because generally speaking, product prices continued to be set higher by international markets even as crude feedstock prices for these refiners were discounted.

Back to the present and - as we discussed a couple of weeks ago, crude prices have come under pressure at the Gulf Coast as more supplies reach refineries there from US and Canadian producers and seasonal refinery maintenance reduces demand for feedstocks (see Goodbye Stranger). But even as crude prices are falling, refinery margins are not responding positively. That is because refined product prices – particularly gasoline are falling faster than crude. And as we shall see, the resulting margin squeeze encourages those refiners that have the flexibility, to cut down their gasoline output and increase their diesel production.

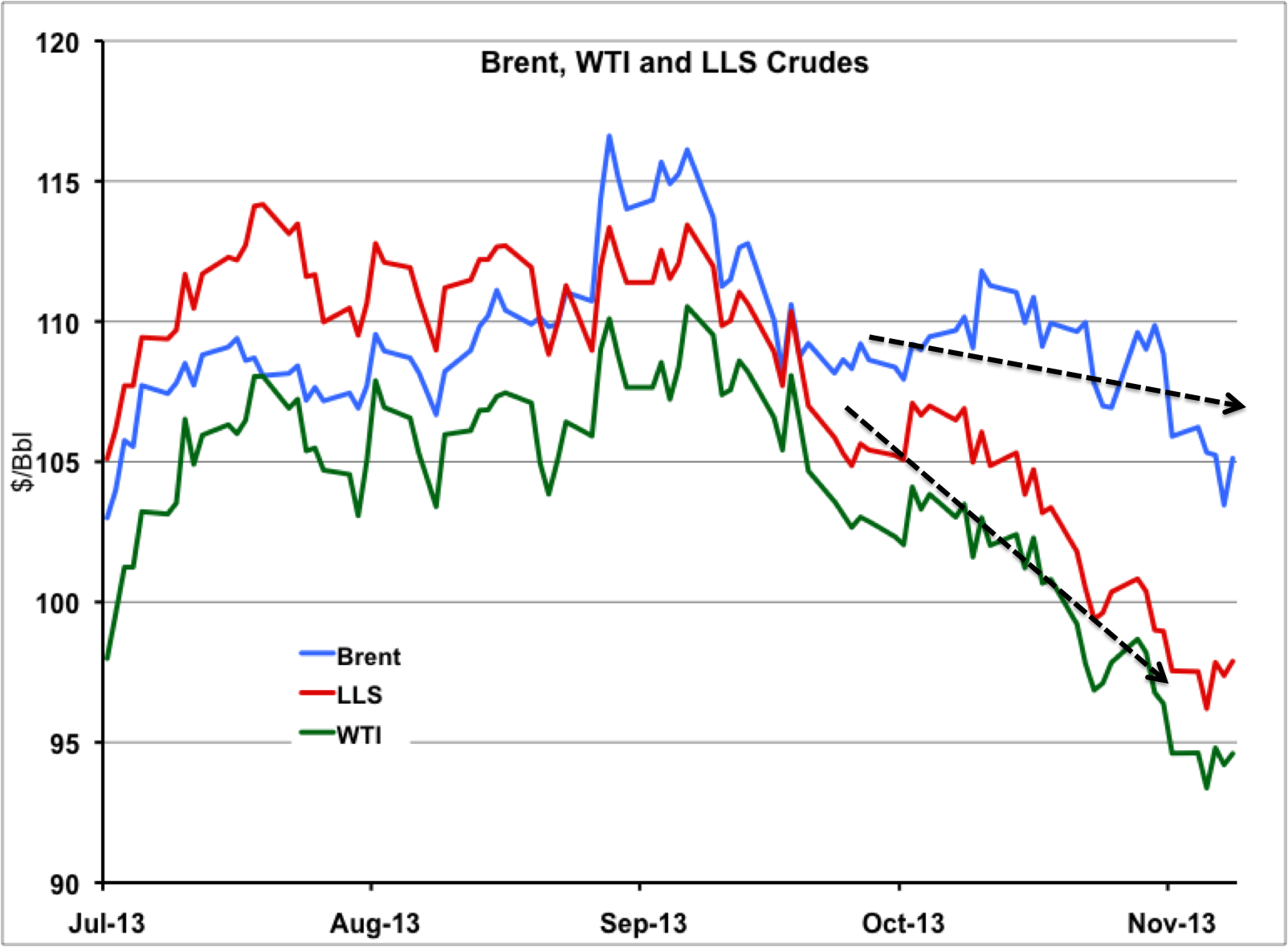

Taking a look first at crude prices, the chart below shows WTI (green line) Gulf Coast benchmark Light Louisiana Sweet (LLS – red line) and international benchmark Brent (blue line) since the start of July 2013. After increasing to over $110/Bbl in early September under the influence of international tensions in the Middle East, crude prices have fallen back below $100/Bbl. As we noted a moment ago an increasing surplus of light sweet crude supplies at the Gulf Coast has caused WTI and LLS prices to fall. Meanwhile Brent prices have become detached from the Gulf Coast market because supplies of imported light and medium sweet crude that use Brent based pricing are not currently needed to meet refinery needs. The two black dotted arrows on the chart show the divergence between Brent and WTI/LLS prices. The current supply surplus has caused crude inventories in the Gulf Coast region to increase by over 17 MMBbl from mid September to the beginning of November. LLS prices have fallen 13 percent from $110.63/Bbl on September 13, 2013 to $97.89/Bbl on November 8, 2013. WTI prices fell 13.6 percent over the same period from $108.21/Bbl on September 13 to $94.6/Bbl on November 8.

Source: CME data from Morningstar

Next take a look at refined product prices for gasoline and diesel at the Gulf Coast. The chart below shows ultra low sulfur diesel (ULSD - green line) and reformulated gasoline (orange line) priced at the Gulf Coast since the start of July 2013. You can see that the price of diesel has remained relatively stable since the start of September while gasoline has fallen sharply (blue dotted circle). The strength of diesel prices results from continued strong demand for exports from the Gulf Coast, to Latin American and European markets. Also demand for heating oil (used primarily in the Northeast during the winter) is high at this time of year in the run up to winter. Because New York State now requires the use of lower sulfur spec heating oil, the demand for low sulfur diesel from Gulf Coast refineries is higher –underpinning ULSD prices.

Comments