Global natural gas prices are once again at record levels as escalating tensions between Russia and the Western world have re-ignited fears over gas shortages in Europe this winter. The global gas market is in the midst of an epic bull run that has been going on for more than a year, taking prices from all-time lows in the summer of 2020 to repeated all-time highs. And while strong demand for gas and LNG has underpinned prices and tied global gas markets together, Europe has been the driving force behind most of the headlines and panic-driven price run-ups. Prices in Europe have climbed to nearly $60/MMBtu as market fears around Russian gas supplies into Europe have been renewed by threats of new U.S. sanctions on Russia over aggression toward Ukraine, delays to the startup of the controversial Nord Stream 2 pipeline, continued low gas flows from Russia to Europe on existing infrastructure, and now Europe is facing its first real cold snap of the season. In today’s RBN blog, we take a look at the situation in Europe and its impact on the global gas and LNG markets.

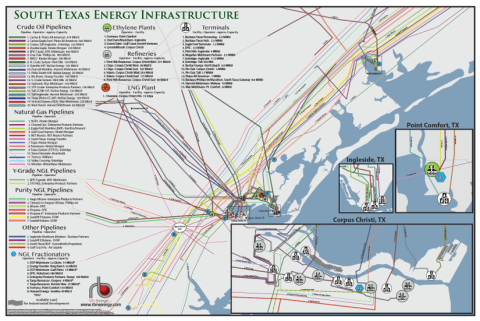

RBN Energy’s South Texas Energy Infrastructure Map brings together all the pieces of the critical and complex puzzle of the greater Corpus Christi region. Spanning from Point Comfort, TX to Corpus Christ, TX and south of the Agua Dulce natural gas hub, the map details the processing, transportation and export facilities in RBN Energy’s classic clear, concise and easy to comprehend style.

Europe features a robust gas market that has multiple supply sources that can be put into three basic categories: domestic production, piped imports from Russia, and LNG. European production has been in a steep decline for more than a decade, driven by falling reserves and economics as well as environmental regulations, and this has increased Europe’s reliance on gas imports, both from Russia and LNG. Russia is the largest supplier of European gas and accounts for 35%-40% of total supply. Reliance on Russian imports was expected to increase this year and in the long term with a controversial new pipeline, Nord Stream 2, which follows the path of the existing Nord Stream Pipeline that brings Russian gas directly to Germany via the Baltic Sea. This route bypasses Ukraine, through which the majority of Russian gas currently bound for Western Europe passes, and is the center of the controversy surrounding the pipeline, as it puts Ukraine’s energy and financial markets in a precarious position. Europe’s growing reliance on Russian gas, which is all owned and controlled by state-owned Gazprom, gives Russia an enormous amount of market power in Europe, and many feel that Russia is using that power to press its advantage.

We began sounding the alarm bells in the early spring that Europe was potentially facing a bumpy winter. After a long heating season last year, European storage inventories were depleted and heading toward multi-year lows. Cold weather lingered into the spring and essentially cost Europe over a month of injection season, putting further stress on storage levels. This was further compounded by record-high carbon prices (red line in Figure 1, below; see I Won’t Back Down) putting upward pressure on gas prices and a multi-front supply shortfall. Serious concern developed that if the shortfall persisted into the winter, Europe would have few avenues for relief in the event of cold weather or supply disruptions or both. Then, Russian imports fell below seasonal norms and LNG cargoes — because of high demand in Asia and Latin America — were hard to come by. For much of the spring and summer, almost no destination-flexible cargoes from the U.S. landed in Europe, all heading to Asian markets or Latin America. This sent prices soaring, with only minor step-backs throughout the spring and summer, pulling all LNG markets along with them, as Asian buyers continued to outbid Europeans for cargoes.

About the song

"Baby, It's Cold Outside" was written by Frank Loesser in 1944. It first appeared in the 1949 film, Neptune's Daughter, and won the Academy Award for Best Original Song in 1949. The call and response song was set up as a duet for Loesser and his wife, Lynn Garland, to sing at a housewarming party the pair was giving in New York City. The example we're giving here is Ray Charles and Betty Carter's definitive version that appeared as the seventh song on their 1961 duet album, Ray Charles and Betty Carter. Recorded at Radio Recorders in Hollywood in June 1961, with Sid Feller producing, the single of "Baby, It's Cold Outside," was released in November 1961. It went to #1 on the Billboard R&B Singles chart and #91 on the Billboard Hot 100 Singles chart. Personnel on the record were: Ray Charles (vocals, piano), Betty Carter (vocals), Hank Crawford (alto sax), David Fathead Newman (tenor sax), Leroy Cooper (baritone sax), Bill Pittman (guitar), Edgar Willis (bass), Mel Lewis (drums), and The Jack Halloran Singers (background vocals). The song has been covered by many artists, including Ella Fitzgerald and Louis Jordan, Dean Martin and Marilyn Maxwell, Brian Setzer and Ann Margret, Rod Stewart and Dolly Parton, and Willie Nelson and Norah Jones.

The album, Ray Charles and Betty Carter, was recorded at Radio Recorders in Hollywood between August 1960-June 1961 and released in August 1961.

Ray Charles was an American singer, songwriter, pianist, and composer. He helped pioneer the soul music genre by combining elements of blues, jazz, rhythm and blues, and gospel into the sides he recorded for Atlantic Records in the fifties. He released 62 studio albums, seven live albums, 39 compilation albums, and 127 singles. He has won 17 Grammy Awards and is a member of the Rock and Roll Hall of Fame, Rhythm and Blues Hall of Fame, and Country Music Hall of Fame. He has a National Medal of Arts, Kennedy Center Honor, a George and Ira Gershwin Award, and has a star on the Hollywood Walk of Fame. Charles died in Beverly Hills in June 2004.

Betty Carter was an American jazz singer known for her improvisational skills. She released 21 studio albums, and ten singles. She holds a National Medal of Arts that she won in 1997. Carter died in Brooklyn in September 1998.

Comments

You failed to mentioned the significant imports received via pipeline from Norway or from Algeria. Here's a link to a graphic that illustrates that (https://www.bruegel.org/publications/datasets/european-natural-gas-imports/). You might also note that EU storage levels are apporaching historical lows (https://www.bruegel.org/2021/12/how-serious-is-europes-natural-gas-storage-shortfall/)