This week BP announced plans to spend $1 Billion increasing production at the company’s Prudhoe Bay Alaska field. Years of declining Alaska North Slope (ANS) crude output have threatened state oil revenues and the safe operation of the Trans-Alaskan pipeline system (TAPS) that transports crude to the southern Port of Valdez. A new tax regime offers more upside potential to encourage producers like BP to invest. There is still a market for medium sour crudes like ANS on the US West Coast and in Asia. However Alaskan producers must overcome regulatory hurdles to compete successfully in these markets and competition for their drilling dollars from shale boom plays in the lower 48. Today we review the prospects for an ANS production renaissance.

RBN presented yesterday at the Alaska Oil and Gas Infrastructure and Development Summit in Anchorage, AK. Our topic was “New Markets for Alaskan Oil”. The sentiment in Anchorage these days is one of optimism that a recently passed oil and gas production tax reform will save the industry from declining production rates. Our message was that there is still demand for ANS and that a North Slope producer has advantages compared to green field alternatives in much of the rest of the world. But there are two forms of challenge that producers need to overcome to justify continued investment in Alaska. The first are regulatory constraints - on crude exports and transportation as well as environmental issues in the US market. The second are competition from booming shale oil production that competes for drilling dollars and is likely to place downward pressure on ANS prices in coming years – reducing producer returns.

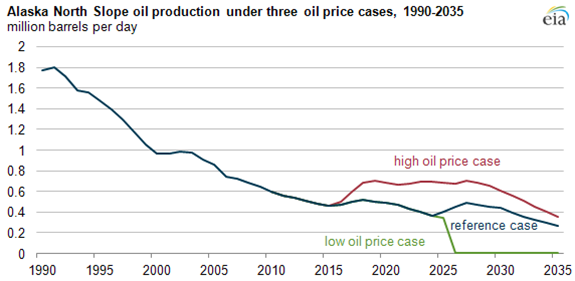

We last wrote about ANS production back in January of this year (see “After The Oil Rush – ANS Decline and the West Coast Crude Market”). We described in that blog the decline in ANS production from a peak of over 2 MMb/d in 1987 to just 590 Mb/d in 2012. The Alaskan Department of Revenue forecasts the decline in production to continue – down to 400 Mb/d by 2020 and 350 Mb/d by 2022 – unless there is new investment by producers. Aside from falling production there is additional risk to the 800 mile TAPS that transports crude from Prudhoe Bay on the northern coast of Alaska to the ice free Port of Valdez in the south from where it is shipped to market in tankers. The pipeline is large enough to carry 2 MMb/d of oil but is currently running only 25 percent full and that creates operational challenges in the arctic cold. A 2011 report by TAPS operator Alyeska Pipeline Service Company on the impact of low flows stated that considerable investment would be needed to keep the pipeline running if volumes fell below 350 Mb/d. The US Energy Information Administration (EIA) 2012 Energy Outlook provided three forecast models for ANS production (see chart below). The EIA forecast suggests that increased ANS output is dependent on higher oil prices and it’s low price scenario would lead production to decline below 350 Mb/d as early as 2026 – causing the pipeline to be decommissioned.

Source: EIA

Yet there is no lack of Alaskan oil in the ground. The latest EIA estimate of Alaska reserves (updated in 2011) indicate up to 3.5 Billion Bbl of proven conventional oil reserves in producing fields onshore and 36 Billion Bbl of unproven reserves in federal lands offshore and onshore. Although production is declining at Prudhoe Bay and other nearby fields there is high potential for new discoveries in the Arctic, both onshore and offshore. The Alaskan Outer Continental Shelf constitutes one of the world’s largest untapped resources potentially reaching as high as 27 Billion Bbl of oil and 132 Tcf of natural gas, with the majority being in the Chukchi Sea. Apart from supplies of ANS crude and equivalent grades there are also large untapped deposits of heavier crude and the possibility exists to exploit unconventional shale deposits in the future.

Part of the reason for declining Alaskan production is reduced investment by producers because of the State production tax regime. The 2007 Alaska’s Clear and Equitable Share (ACES) system was a progressive tax that increased the State’s take from oil production as prices rose. This tax – introduced under Governor Palin (when she wasn’t looking out for Russians) became very unpopular with producers as oil prices increased to record levels in 2008. The present Governor Parnell just signed new legislation into law in late May 2013 that imposes a flat tax rate of 35 percent on producers and provides relief for development costs. The new tax law was championed by the big three Alaskan producers – ExxonMobil, BP and ConocoPhillips. Two of the three have already indicated their approval of the change by their actions. Conoco announced it would add a new rig to its Kuparek field and on Monday of this week BP announced plans to invest $1B with plans to add two drilling rigs to its Prudhoe Bay field. BP will also begin planning additional Prudhoe Bay development that could lead to $3B more investment.

And there is demand for ANS crude both in the US and overseas. This medium sour crude with a 31.5 API gravity and 0.96 percent sulfur is desired by many West Coast refineries that were built to run on a diet of ANS. To that extent they would use more ANS if it were available and if the price was competitive. ANS is also quite marketable outside the US - most obviously in Asia – one of the few places in the world where demand for crude oil is still growing. Chinese crude demand is expected to increase by 10 MMb/d from 2012 to 2030 (source: BP Outlook). Many Chinese refineries are configured to run middle eastern medium sour grades that are similar to ANS. The transport distance from Alaska to Asia is shorter than for any other part of North America.

But ANS faces market challenges in both Asia and the US which cast doubt on the returns that producers can make from new drilling in Alaska. In the first place there are restrictions on the export of ANS (as well as all other US crudes – see Fifty Shades Lighter The Lease Condensate Export Problem). It is actually legal to export ANS with a license from the Bureau of Industry and Security (BIS) but there is a catch. Because US tax payers paid a significant part of the $8B cost of building TAPS, seaborne exports of Alaskan crude that use that pipeline (i.e. all ANS production) are subject to the Maritime Act – aka the Jones Act. We did a whole blog on the Jones Act last year (see The Sea and Mr. Jones) and the bottom line is that it increases shipping costs by at least $2-$3/Bbl for most tanker voyages by requiring strict adherence to US manning levels and ownership rules. That means Alaskan exports to Asia would be at a cost disadvantage against competitors from the Middle East, Russia and Canada. Consequenty producers realize lower returns and diminished incentives to invest in Alaskan production.

About the song

Michelle Shocked had a hit in 1988 with “Anchorage”