With natural gas prices hanging at numbers around $2.50/MMbtu and possibly headed lower, there is a lot of talk about shut-ins. Presumably going out to the wellhead and turning off the valve. A couple of weeks ago, Jim Hackett, Anadarko CEO told a Rice University audience that “at current gas prices, gas operators can't sustain profitable domestic operations. By shutting in some of their wells, prices quickly would rebound.” Is that true? Is it a good idea?

Here’s another couple of press quotes over the past few days:

* “Faced with decade-low natural gas prices that have made some drilling operations unprofitable, Chesapeake Energy Corp. says it will drastically cut drilling and production of the fuel in the U.S.”. (Oil Drum) [“Drastically?” I don’t remember Chesapeake saying that.]

* …Producers "likely" will have to shut in more than 1 Tcf of natural gas sometime this year.” (Raymond James) [Wow. That’s a lot of gas.]

The RBN Blog posting on January 24th attempted to dispel some of the myths around shut-ins. In Shut-in by Press Release – Part Deux we looked at just exactly what Chesapeake said, and how little it really meant. One assertion of that piece was that shut-in economics rarely make sense. But we didn’t get into the math. Since this subject doesn’t’ seem to be going away anytime soon, let’s delve into the details.

First the premise. I can sell my gas for $2.50 and get revenue of $2.50. Or I can shut in my well and get zero. Let’s say I shut in 10% of my gas. The price better increase at least $0.28/mmbtu on the other 90% or it’s been a losing proposition.

But wait, you say. The shut-in gas is not gone. It is still in the ground to be produced another day. Yes, but not tomorrow. With few exceptions (described below), a cubic foot produced today cannot be immediately recovered when the well is turned back on. That is because the well produces at the maximum rate in the first place. That rate is established by determining the flow which will yield the maximum recovery of the reserves over the life of the well. If a well is producing 5,000 Mcf/d today and we shut the well in tomorrow, it won’t produce 10,000 Mcf/d the next day. In fact, you don’t see those deferred molecules to the end of the producing life of the well.

Take a look at the typical shale well decline curve below. If we shut in for a few months in 2012 (the yellow carve out), that gas doesn’t show up until years later (the green area).

One obvious consequence is that the producer has less dollars to pay the bills. Revenues fall and the producer must curtail drilling programs or borrow more money. (Thus on 2/6/12 S&P affirmed Chesapeake’s BB+ but downgraded the rating from stable to negative for this very reason. “…because investment will now likely exceed cash generation to a greater extent than previously assumed.” More about that in a future blog.)

There are other issues. Different wells respond differently to shut-in. In some cases, shut in actually can damage or choke back future flows from the well. Other wells can see a surge of production when the well is restarted, recovering some of the lost production. But in most cases, it is simply a deferral of cash flow. That can impact the economics of the well investment. A dollar received in 2021 is not worth the same as a dollar in 2012. It’s that old present worth problem.

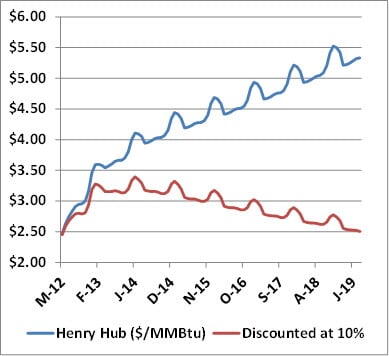

Consider the graph below. The blue line is the CME/NYMEX natural gas forward curve. The red line is that same curve, discounted at 10%. We can argue about cost of capital and other discount rate issues, but just go with me on the concept. Even though the forward curve gets north of $5.00 by 2019, when you discount the 2019 price back to today, it comes out about the same as today’s price. Not an economic disaster (due to the combination of a low prompt price and steep contango in the market today). But what happens if those future prices don’t materialize? It’s tough to hedge out more than a couple of years.

All of this is not to say that we won’t see a decline in natural gas production. The storage math would say that it has to happen. Drilling in dry gas plays will get cut way back. Signs of declining volumes are already being reported in dry areas like the Haynesville. Well completions will be delayed. Investment budgets will be cut. Producers with heavy exposure to natural gas prices will hunker down. These developments will kick in over time, not overnight.

The situations of actual shut -in - where the valves are turned off immediately at existing wells -- will be few and far between. For both operational and financial reasons.

Getting paid now is good, even if prices are not what you would like. If you don’t get enough money in the door now you might not be around later.