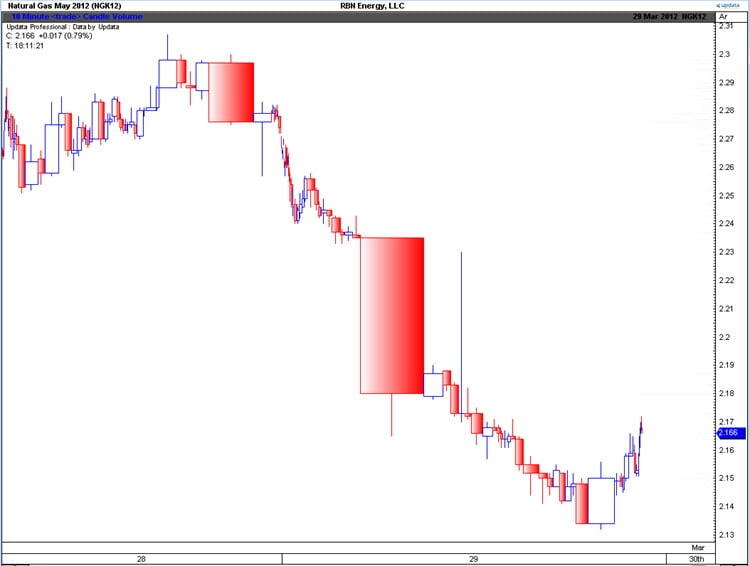

Thursday’s RBN post closed out with the prospect of bad news for gas price bulls if EIA storage came in with some number like +56 bcf when expectations were for +45. So the EIA build turned out to be one notch higher at +57 bcf. True to form, the CME/NYMEX May contract dropped like a rock. See the Updata Candlestick-Volume chart below that again tells the story.

May had closed at $2.282 on Tuesday, was moving lower to $2.24 just before EIA printed, then immediately fell to $2.18 on big volume. The price drifted around the rest of the day before settling at $2.149, down 13.3 cnts. Yes it was a big drop, but only 4 cnts off the close for the prompt April contract the previous day.

Clearly the market did not resolve the ongoing tug-of-war over the $2.00 threshold price. But fortunately RBN took action! We surveyed our members to find out what the market really thinks to settle this issue of price expectations once and for all. Or so we thought.

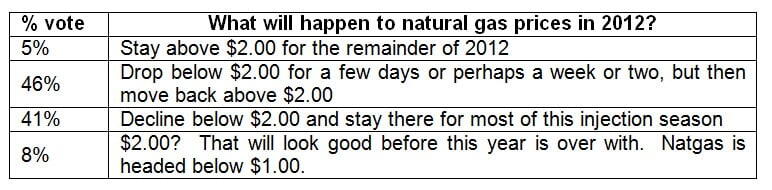

The question was simple. What will happen to natural gas prices in 2012? We gave our voters four choices in increasing levels of bearishness.

By midnight on Thursday 247 individual RBN members had come to the site during the day. 39 voted. Not as large a sample as I would have liked, but enough to get some sense of our collective view. Unfortunately our voters were as conflicted as the market. Here are the results from the poll.

I promise I did not make this up. 51% think the market stays above $2.00 for all or most of the remainder of 2012. 49% think it will be bad or really bad for gas prices. A dead heat. There were hanging chads spilling out of our web servers. No wonder the market is range bound. Market opinion is range bound, even in our tiny sample.

Fortunately for our industry, opinion only counts for so much. We are in a physical business. While opinions, news and transaction flows are the prime movers in financial markets, the prime mover with commodities is the physical supply/demand balance for stuff. In this case, natural gas. Ultimately opinions and financial prices must true up to physical realities. And those physical realities are looking more bearish each day. Aside from a +57 Bcf storage build, just look at ICE next day prices traded yesterday for flow today. Henry hub $2.017, down 3 cnts. CIG Mainline $1.70, down 4 cnts. SoCal Border (with OFO expectations riding high) $2.15 down 17 cnts. And today kicks off a three day weekend. It seems like only the possibility of a snowy weekend in parts of the northeast could avoid sub-$2.00 Henry Hub cash prices. Of course, that’s the forecast.

So the split decision could continue on – for who knows how long. But don’t forget – there is twice as much gas in storage at the end of March than there was last year. At some point that can’t continue. It seems like we need a healthy dose of price signal. And the sooner it happens the less severe that it will ultimately be. I guess you can tell how I voted.

BTW, we did not cut off the voting mechanism. So if you are hanging around this weekend and want to go back to Thursday’s blog and register your opinion, have at. Just click here – Livin on the Fault Line. We’ll leave it open until Sunday night. You can’t vote a second time (unless you get a new IP address), but once you’ve voted you can see the percentage splits.

We’ve got something new on RBN today. Check out Updata’s daily technical analysis for natural gas and crude markets here.