Yesterday we looked at Tuesday’s natural gas price 13cnt whipsaw and the apparent resistance to prices below $2.26 or so. I closed that blog with a commitment to look again at the fundamentals for oversupply, maxed out storage capacity and the impending collision of natural gas prices with reality (for background see Whip it, Whip it good). That’s what we’ll do today.

To update our perspective, let’s look at what happened on Wednesday. Things continued to deteriorate in the cash market. ICE Henry hub cash was down another 2 cnts to $2.13/MMbtu. Thirty-two cash hubs traded below $2.00 versus 26 on Tuesday. Gas for the balance of the month (Balmo) deals also softened. But April futures hung in there, closing out at $2.284, down a mere 1.5 cnts. So theoretically the enterprising marketer could buy cash at $2.13, cut a one-month parking deal and deliver the gas on the CME/NYMEX contract at $2.28. Better do it quick since there are only 10 shopping days left before the April contract closes out.

How can you be anything but bearish with today’s fundamentals looking at you? Let’s dredge up those numbers one more time, and play out the most likely scenarios for storage over the next eight months. This time we’ll use a spreadsheet instead of the back of an envelope. The answers are the same, but it is easier to see in a graph.

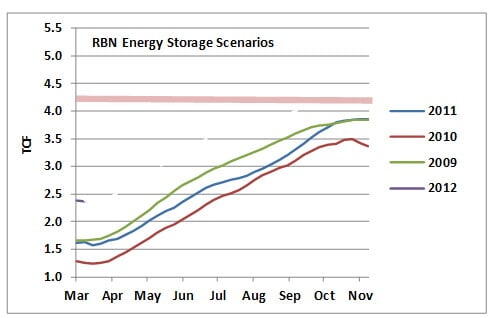

Graph #1 shows storage inventory history for the past three years – 2009, 10 and 11. We hit most of the highs in 2009. Last year inventories stayed below 2009 due to the hot summer. When autumn weather wiped out that powergen demand delta, inventories caught up in a hurry. Both 2009 and 2011 ended the season at about 3.8 TCF. Note where we are starting in 2012… now 45% over last year.

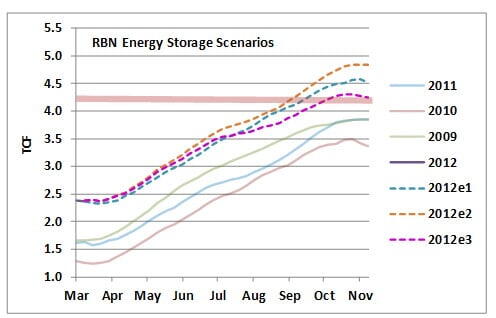

Three scenarios are built in into Graph #2, below. All three assume the same weekly flow behavior that we saw in 2011, but with a delta built into the total balance number. Each scenario starts from where inventories are today.

Scenario 2012e1 (the blue dashed line) simply applies the same build rate that we saw last year throughout this injection season. That ends the injection season at 4.5 TCF. I show this just for reference purposes, since this scenario could not happen. Dry lower-48 production is up 9.3% YTD 2012 versus last year, demand is up only slightly, so the daily oversupply is well above last year. But even this impossible scenario ends the season at a level above FERC’s 4.2 TCF estimated ceiling.

Scenario 2012e2 (the orange dashed line) shows what happens if production flattens out at today’s numbers. For today I’m using the current BENTEK numbers for production, which show a decline of about 1.5 Bcf/d since the first of this year. So it is flat from today, not flat from December (the most recent EIA numbers). That scenario gets us to 4.8 TCF, 0.6 TCF above the ceiling. This one is probably high, since additional production declines plus more coal-gas switching will definitely kick in at prices below $3.00.

What does it take to bring Scenario 2012e2 down low enough so that storage ends the injection season at 4.2 TCF? The answer is 2.5 Bcf/d. You say, well that doesn’t sound like that big of a deal. It is bigger than it sounds. There are two factors to consider. First, 1.5 Bcf/d is already gone. So it is really 4.0 Bcf/d compared to the end of 2011. But the bigger factor is that the number assumes that the 2.5 BCF/d disappears out of the balance tomorrow, and stays gone for the entire injection season. That’s not going to happen.

Which gets us to Scenario 2012e3 (the hot pink dashed line). In this one, the delta that comes out of the balance declines ratably from today until the end of the injection season. Of course, it would not happen like that, but the math is easy and the calculations yield a reasonable number. That is 5 Bcf/d. Plus the 1.5 Bcf/d that has already happened since Jan 1st gets to a net 6.5 Bcf/d.

Can a ratable decline 5.0 Bcf/d come out of the oversupply balance over the injection season? Yes, it is quite possible. My best guess would be about half from producers, and half from higher demand from the power sector (coal-gas switching, etc.). But it will not happen without very low prices to create enough pain for producers to cut back drilling programs, curtail well completions and shut in some existing dry production (yes I said shut-in). And low enough prices to encourage power generators to deal with all the coal displacement issues that come along with high levels coal-to-gas switching.

All of these numbers and graphs boil down to one thing. We are in a massive oversupply situation that, if left unchecked will result in the industry hitting the storage wall in October. Only low prices and a response from both the supply and demand side will save the natural gas market from itself.

We are the Shales. Lower your prices and surrender your drilling rigs. We will add your technological distinctiveness to our own. Your culture will adapt to service us. Resistance is futile [1].

One last comment. If things are so bad, why do we see a relatively healthy $1.07/MMbtu contango between April 2012 and January 2013. Rumor has it that producers are lifting hedges in the back end of the curve so if they do have cut back (or shut in) it does not result in accounting issues. I have absolutely no evidence that this is the case. But it makes a nice story, and could make for an interesting trade.

-----------------------------------

[1] Apologies to the Borg, that pseudo-race of cybernetic organisms from Star Trek. The Borg don’t talk much and spend most of their time hanging out at the hive or assimilating populations of planets. Similar to the way shale technologies have assimilated all gas and liquid hydrocarbon production in North America. Resistance is futile.