If you don’t have young teenagers (I don’t) and are not in the blogging business (I am), you might not be keeping up with the incredible number of internet/texting acronyms that have entered the ‘language’ over the past few years. One such acronym is NGL which of course stands for Not Gonna Lie. Any Google of a search term containing NGL brings up this definition and all sorts of other interesting hits. For your general edification I’ll be working some of these into the RBN blogs. That way you can use these terms to entertain your friends and look cool to your teenagers.

Which brings us to our topic today. What is happening in the NGL market? We’ve talked a lot about the huge profits that gas processors are banking in The Golden Age of Gas Processing series. But what about volumes and prices?

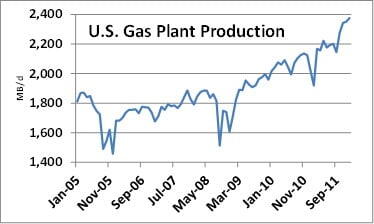

First volumes. This graph shows total EIA U.S. Gas Plant Production from Jan 2005 until Jan 2012. I’ve adjusted the scale so that the trend is unmistakable. Except for the hurricane blip in 2008, production has been growing at an average of 10 MB/d each month. Over the past year that number looks more like 30 Mb/d each month or +1.3% every 30 days. Sorry to go on about this, but after watching NGL production languish at 1,800 Mb/d for the prior decade, it is an amazing thing to see.

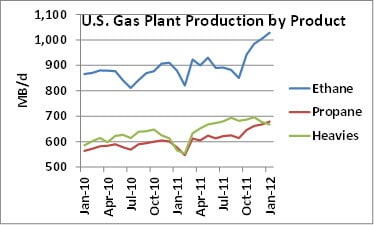

Wondering which of the NGLs is responsible for most of the growth? I think the graph below tells the story. It is ethane, ethane and ethane. And some propane. Heavies (normal butane, isobutane, and natural gasoline) have increased, and the growth rate for propane is respectable. But for the last five months, ethane is off the scale, up 178 MB/d. Of that change, 46 MB/d was from PADD II, 80 MB/d from PADD III, and 52 MB/d from PADD IV. That’s a pretty good distribution across most of the major plays.

But nada from PADD I. Marcellus ethane production remains constrained by lack of pipeline capacity. The Sunoco/Mark West Mariner West project is scheduled for July 2013 and the Enterprise ATEX Express line is targeted for Q1 2014. Until then, well see no ethane from the Marcellus.

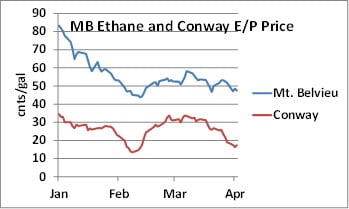

How about prices? As you might expect, ethane and ethane/propane mix (E/P) have had the biggest swings. OPIS Mt. Belvieu purity ethane is down from the mid-80s in January to 47.5 cnts/gal yesterday (graph below). And Conway E/P (80/20) mix has done another nose-dive this week, dropping to 16.375 cnts/gal on Tuesday before recovering a penny yesterday. It’s another one of those capacity situations similar to what was discussed here in the Feb 2012 posting – the Decline and Fall of Conway Ethane. Then as now, pipeline capacity constraints combined with petchem turnarounds in Mt. Belvieu to drive the price into the teens – capacity to move barrels south is limited and petchem capacity to consume the barrels is constrained. There are three petchem turnarounds going on now and four more coming up over the next few weeks, and that will work to keep downward pressure on ethane prices. Complicating matters are a couple of fractionator turnarounds during Q2 that will take purity barrels out of the market. But underlying all of this is relentless supply growth, which will keep the lid on ethane prices.

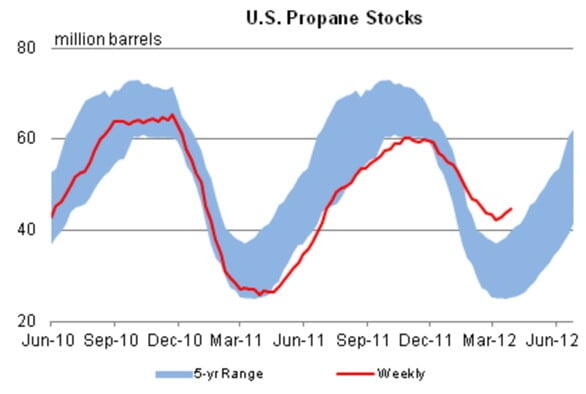

For the entertainment of our natural gas audience, I offer up the next and final graphic. If you were thinking that natural gas is the only energy commodity with an inventory problem, check out the EIA propane stocks graph released today. Look familiar? Certainly this is not as bad as the natural gas problem, but it is worrisome to the industry. The causes are the same as gas – no winter and lots of production. And prices are down, but not down hard. Prices have been cycling between $1.20 and $1.30 / Gal since mid-January. Yesterday OPIS NON-TET propane was about $1.19. Is it headed materially lower? Like the gas market there seem to be equal numbers of bulls and bears. Like the gas market, I tend to side with the bears.

Can’t forget the heavies. Without going into the details, the butanes are holding up pretty well as we move into the summer gasoline season, and natural gasoline continues to run strong due to its use as a diluent in the Canadian oil sands crude market.

So as promised, I’m not gonna lie. NGL production is up, prices are down (but not by that much, except for ethane), and capacity is constrained or limited in some parts of the market. Expect more of the same in the coming months.