Yesterday was still another day of lower natural gas cash prices and whipsawing futures prices. ICE cash Henry Hub was at $2.0748/MMbtu, down 6 cnts. At one point weekend Henry Hub printed $1.98. TGP-Z4 Marcellus came down 8 cnts to $1.9440. April futures ran up again to $2.33 about 10:30 before coming off the rest of the day, closing at $2.279. We’ve talked a lot about production gluts and potential storage overruns over the past two days. Perhaps it is good time to step back and look at the big picture of U.S. natural gas supply and demand. And what better way to do that than with BENTEK numbers.

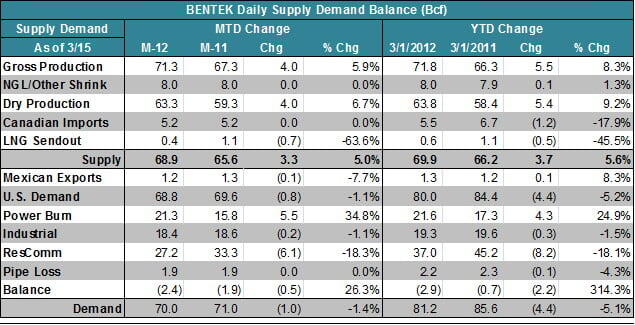

The table below is a summary of the key elements of BENTEK’s Supply/Demand Balance table published each day by the company. As I’m sure most of you know, it is based on pipeline scheduled volumes at thousands of meter locations around the country. BENTEK aggregates this data in such a way to assess the overall supply/demand picture (and thus storage balances) on a daily basis. The table shown here is a subset of the BENTEK report that they provide periodically to a few companies that cover natural gas markets. Thanks to BENTEK for including RBN on the distribution.

There are two sections of the table. On the left we have current month-to-date average volumes, comparing March 2012 with March 2011. On the right, Year-to-Date volumes comparing Q1 2012 with Q1 2011. Today we’ll concentrate on the Year-to-Date Q1, and tick down line-by-line to see what is happening.

No surprise with gross and net production. Gross production up by 5.5 Bcf/d, or 8.3%. Dry production +5.4 Bcf/d, or 9.2%. This is the source of a big piece of the storage overhang discussed in yesterday’s blog - Resistance is Futile. Canadian imports down by 1.2 Bcf/d or almost 18%. That is a huge number when you consider that 2011 was lower than 2010 by more than a Bcf/d. And the truly ugly story, LNG sendout, down 0.5 Bcf/d or 45% to only 0.6 Bcf/d so far this year. Remember 2007 when LNG sendout averaged 2.2 Bcf/d and terminals were being built right and left? That seems like a long time ago. But even with these declining imports, total supply is up 3.7 Bcf/d or 5.6% since Q1 of last year. That’s a big number.

What about the demand side? About the same volume is going to Mexico, up 8.3% on a percentage basis but only 0.1 Bcf/d higher. Power Burn up a whopping 25% or 4.3 Bcf/d. Thank goodness for the power guys burning more gas per degree day, primarily at the expense of coal. That’s the only happy news on the demand side. Industrial demand is about flat. Quite a disappointment when you think about the cost advantage dirt-cheap gas provides to the U.S. industrial sector. But that disappointment pales next to a 8.2 Bcf/d decline in residential/commercial demand. That’s what no winter looks like to the gas business –18% below last year. Put those numbers in your memory bank somewhere. You’ll need them next year.

So when you put the demand numbers together, the total is down 4.4 Bcf/d or 5.1%. With supply up 3.7 Bcf/d, that’s a net swing of 8.1 Bcf/d. No wonder storage inventories are 45% over last year. And no wonder that the imbalance better start correcting itself ASAP.

What’s the moral of this story? If you want to understand what is going to happen next, you’ve got to track these numbers. Storage levels may tell you that either supply or demand (or both) are starting to correct. But to understand the next phase of this market, it will be extremely important to understand which side of the equation is responding to price pressures.

It will be sad if supply carries the whole load. If the only thing that corrects the imbalance is supply, that means that some producers get crushed, and are on the auction block. Economic activity in many of the shale plays (especially the dry plays) dries up. OMG, what will happen to the Dowdens, those bayou billionaires on CMT? The glass is half empty. On the other hand, if it is a price response from the demand side, it means that industrials have figured out a way to exploit cheap energy and are hiring like crazy. Clean natural gas is making serious inroads in to coal’s market share. NGVs are tooling down the highway. T Boone smiles. Unemployment goes to 6%. There is an upturn in housing prices. The S&P 500 hits 2,000!!! The glass is half full.

From the standpoint of the natural gas market, here’s my theory. If the correction comes primarily from the supply side (the more likely scenario) then production can correct relatively quickly when prices start to come back. That is because E&P companies won’t be shutting down (like what happened in the ‘80s and ‘90s) and their geologists going to work at Quickie Mart. They will still be drilling for crude oil and wet gas, and can flip back to dry gas in a heartbeat when the price incentive returns. If oversupply happens again, it can turn off just as quickly, for the same reason.

On the other hand, a demand response will become a permanent fixture of the market. Once those new plants are built, the new NGVs are on the road and the coal plants are shut down, a price response won’t turn them off. And that will make the glass not just half full, but completely full for the U.S. natural gas industry.

Comments

If anyone would like more information about Bentek's most popular report, the Daily Supply/Demand Balance, please feel free to contact me via [email protected].