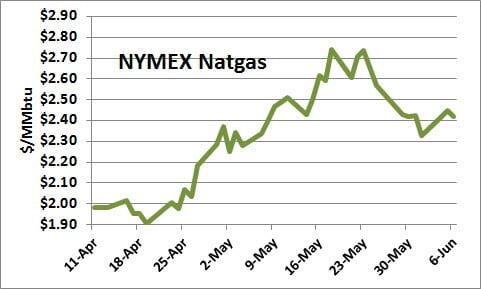

Yesterday natural gas NYMEX futures for July delivery closed at $2.421/MMbtu, down 2.5 cnts. Given where half of our RBN readers thought the market was going at the end of March (see Split Decision), this is a pretty good number. After bottoming out at $1.91/MMbtu, Natgas skyrocketed to $2.74 before drifting back into the mid-$2.40s for the past few days (See graph below). Is this price a signal that we’ve dodged the bullet one more year? That the odds of natural gas storage inventories hitting maximum capacity levels are increasingly unlikely? Clearly we need to look at the Bentek supply/demand numbers once more to get a better understanding of what is going on.

First we look at production. The graph below shows Bentek’s ‘Cell Model’ U.S. lower 48 production numbers January 2012 until today. Volume is down by about 1.5 Bcf/d. But note that just nine days ago production was about flat with the first of the year. Then production came off hard over the past few days. Here are the two most important take-ways. First, natural gas production has been basically flat since the first of the year. As we’ve mentioned here before, any production declines from dry gas plays like the Haynesville have been offset by increases from wet gas plays and the Marcellus dry zone (Marcellus Special - Defying Gravity). Second, gas production as measured by pipeline nominations in the Bentek system are down hard over the past few days primarily due to pipeline maintenance in the San Juan and similar mechanical constraints in the Southeast/Gulf. Once the hardware problems are resolved, expect to see production to recover and continue to increase.