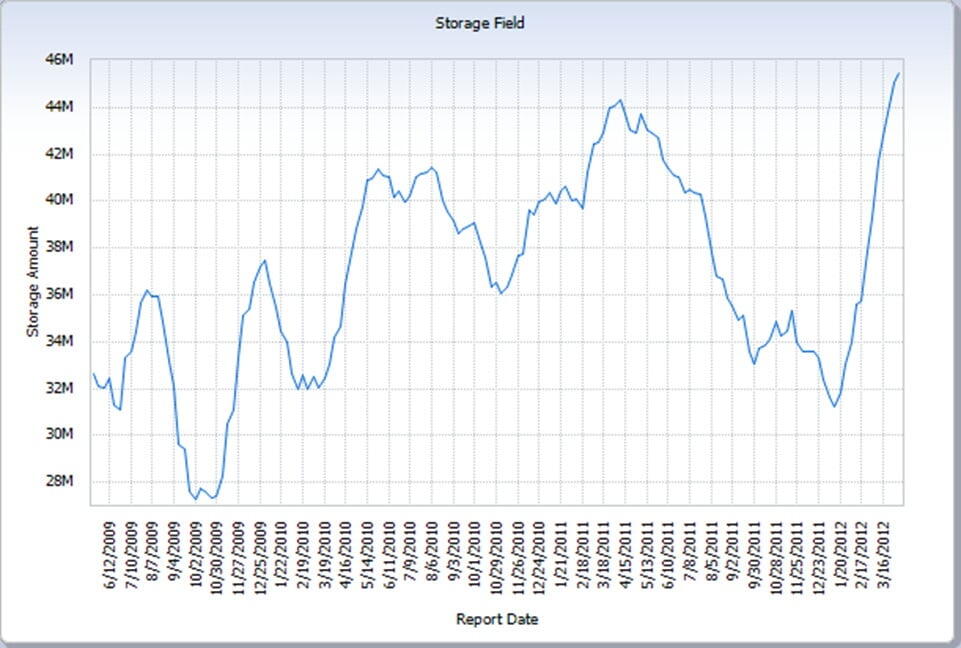

Last week EIA published a note titled Cushing Crude Oil Inventories Rising In 2012, which focuses on the 12 MMbl increase in storage levels from mid-January until end-March. It was a 43% surge, the largest over an 11 week period since 2009.

See graph below.

| Big news out of ONEOK yesterday – a new 200 Mb/d crude oil pipeline from the Bakken to Cushing. If you have not seen the route or press release, download links are at the bottom of this post. |

EIA attributes 20% of the build to the reversal of Seaway, which was emptied into Cushing so the pipe could be reversed. The rest, according to EIA is ‘largely due to flows into Cushing as a result of increasing production in the mid-continent region’. They also note that ‘While Cushing inventories are now approaching the record levels of 2011, the amount of available storage capacity at Cushing is much greater now than it was a year ago, relieving some of the pressure on demand for incremental storage capacity.

These look like pretty big numbers. How should we interpret this development? Is there a gas-like inventory situation looming for Cushing crude oil? Is it possible to tell which crude supplies are contributing to these inventory increases? And BTW, what kind of crude oil will be moving from Cushing to the Gulf on Seaway – heavy or light?

Markets have always been a little (or a lot) opaque around Cushing, but the folks at Genscape have helped in bringing transparency to that crude oil hub. Genscape has been kind enough to provide a few graphs to RBN members that will shed some light on the developments.

The first graph shows storage inventories. According to the Genscape numbers, Cushing inventories have jumped from about 31.5 MMBbls to more than 45 MMBbls from January 20th until today. That’s a lot of oil. Note that the volume is above the EIA numbers because Genscape shows ‘shell’ inventories – the total volume that will fit inside the tank. EIA shows operational inventories, usually about 10% less.

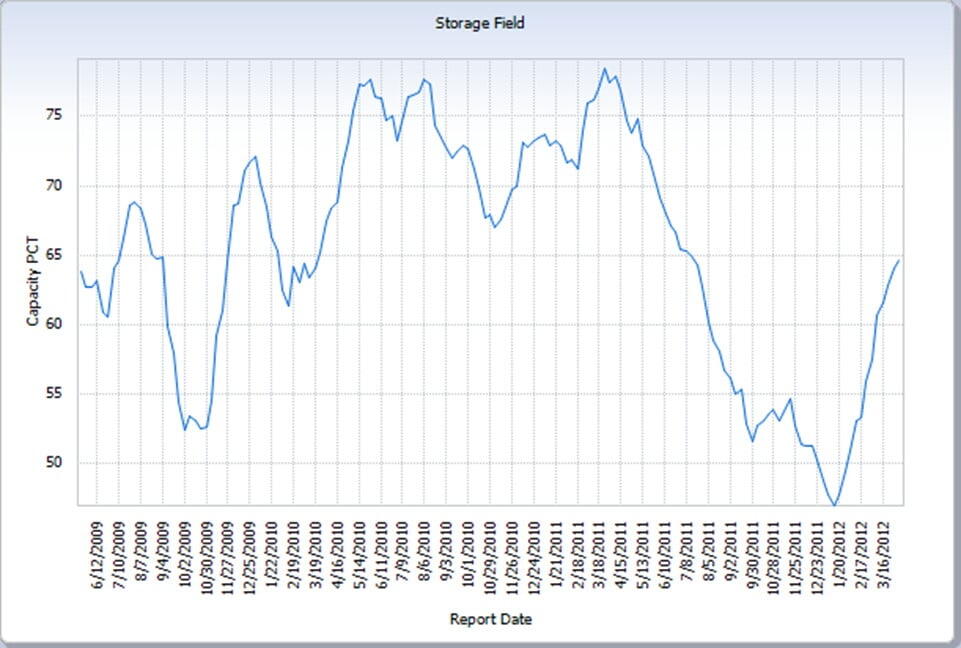

(These graphs are formatted large so you can read the units and dates).

But before you start getting nervous about storage capacity overruns like we are dealing with in the gas market we need to look at the capacity side of the equation. And there we have seen a big change over the past two years, with new construction bringing on an incremental 17 MMBbls of new capacity. That’s an increase from about 52 MMbbls to 70 MMbls. So when we look at storage utilization in the next graph -- it is a non-issue. The utilization percent was below 50% at the first of the year, and now is only up to about 65%. At this point we are a long way from filling up Cushing.

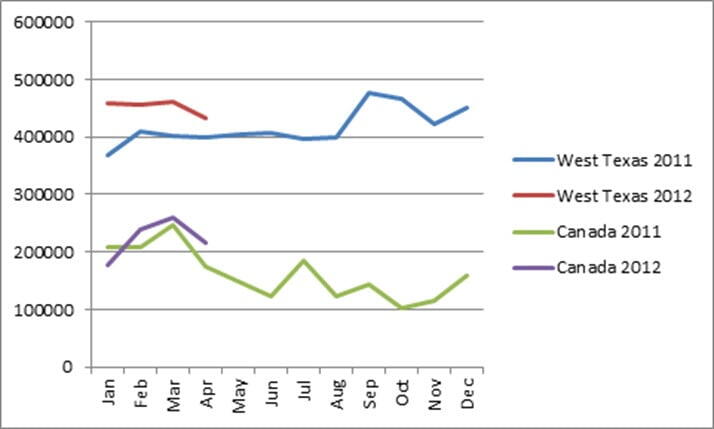

Where has the oil come from? According to Genscape’s numbers, in the last half of 2011 about 75% of the crude came from West Texas on the Basin and Centurion pipelines, while about 25% came from Canada on Spearhead and Keystone. But so far this year, almost 40% of the crude has been Canadian. That suggests that shippers may be loading up Cushing with more Canadian heavy crude in anticipation of Seaway’s southbound flow. And if it does turn out to be mostly heavy oil on Seaway, what will that mean for the differential of WTI versus LLS and/or Brent? That sounds like a topic for another blog.

| Big news out of ONEOK yesterday – a new 200 Mb/d crude oil pipeline from the Bakken to Cushing. If you have not seen the route or press release, download links are below. |